FRANCE T-BILL AUCTION PREVIEW: On offer next week

Mar-08 10:04

Agence France Tresor will look to sell up to a combined E7.2bln of the following 12/13/27/50-week BTFs at its auction next Monday (Mar 11):

- E3.0-3.4bln of the 12-week Jun 5, 2024 BTF

- E0.2-0.6bln of the 13-week Jun 12, 2024 BTF

- E1.3-1.7bln of the new 27-week Sep 18, 2024 BTF

- E1.1-1.5bln of the 50-week Feb 26, 2025 BTF

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT AUCTION RESULTS: 3.75% Mar-27 Gilt

Feb-07 10:03

| 3.75% Mar-27 Gilt | Previous | |

| Amount | GBP4.00bln | GBP4.00bln |

| Avg yield | 4.131% | 3.887% |

| Bid-to-cover | 3.04x | 3.44x |

| Tail | 0.5bp | 0.2bp |

| Avg price | 98.900 | 99.591 |

| Low price | 98.887 | 99.584 |

| Pre-auction mid | 98.894 | |

| Previous date | 10-Jan-24 |

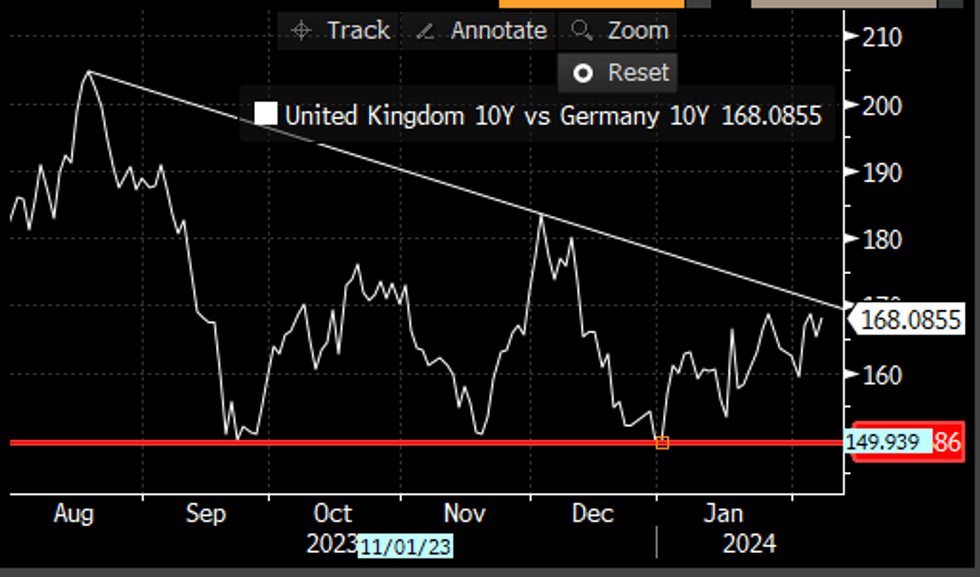

BONDS: Gilt/Bund spread tests resistance

Feb-07 09:59

- Gilt/Bund spread sits wider today, by 2.8bps, with Gilt future underperforming Bund, but both contracts stay in very tight ranges.

- Nonetheless, the January high, and the widest print since 12th December at ~168.8bps has so far held this Month, although better resistance will be seen around the 170.8bps area.

Chart source: MNI/Bloomberg.

GERMAN DATA: Services Sector Turnover Turning Lower, Mirroring Weak Survey Data

Feb-07 09:56

Turnover in German services sectors (excl. finance and insurance) weakened in November, coming in at -0.2% M/M (vs -0.6% prior) and +1.2% Y/Y.

- Those figures, published on Tuesday, which are reported by Destatis in real (inflation adjusted) and seasonally adjusted terms, represented the third monthly decline in a row. The 3M/3M measure came in at -0.6% (vs -0.2% prior), the second decline after 6 consecutive positive prints.

- The strongest gains on a monthly basis could be seen in information and communication at +1.3% M/M (vs -0.1% prior) and in freelance, scientific and technical services at +0.4% (vs +1.0% prior).

- Declines could be observed in the "other services" sector (i.e. rental of movable property and placement of labour) at -1.3% M/M (vs -2.4% prior), transport at -0.7% M/M (vs -0.5% prior) and real estate services at -0.2% M/M (vs +1.4% prior).

- Services have been relatively resilient compared to the manufacturing sector in Germany, but the weakness which started to emerge at the beginning of autumn last year seems to continue.

- Activity implied by the German Services PMI has remained in contractionary territory since November, coming in at 47.7 in January (49.3 Dec, 48.7 Nov). The latest release noted "an insufficient supply of new business to replace completed projects" and the "rate at which outstanding business fell was [...] the quickest seen for just over three-and-a-half years". The IFO services subindex also is on a declining trend but stayed in expansionary territory for now.

- Further dents in the relatively strong performance of German services might thus be possible going forward.

MNI, Destatis

MNI, Destatis