OIL: Oil End of Day Summary: Daily Losses and Weekly Gains

Aug-01 2025 18:21

WTI is down sharply today following a series of weak US data releases, adding to global economic concerns amid President Trump’s tariffs. However, WTI is set for a near 3% net weekly rise due to Trump’s threats of secondary tariffs on Russia.

- WTI SEP 25 down 2.8% at 67.3$/bbl

- Baker Hughes rig count: Oil: 410 (-5) - down 75 rigs, or 15.5% on the year to the lowest since September 2021.

- Nonfarm payrolls growth was weaker than expected at 73k (cons 104k) after huge downward revisions in both June (-133k to just 14k) and May (-125k to 19k).

- Manufacturing data also underperformed estimates, with the US ISM Manufacturing Index at a nine-month low of 48, compared to an estimated 49.5, in a recent release.

- US President Trump slapped steep tariffs on exports from dozens of trading partners ahead of a Friday trade deal deadline, Reuters reports.

- Any perceived disruption to Russian volumes could propel Brent prices into the $80s/b or higher: JP Morgan.

- Chevron said that it expects some Venezuelan oil to start flowing this month.

- OPEC+ holders of spare production capacity will be reluctant to boost their own output to help facilitate US sanctions aimed at co-chair Russia: RBC

- At least four oil tankers laden with Russian crude are waiting off India’s western coast: Bloomberg.

- OPEC+ will likely approve another oil output hike on Sunday, sources familiar with the discussions told Reuters, adding that the group is still debating the final size of the increase for September.

- Saudi Arabia’s oil drilling units declined for a sixth consecutive month, reaching an over two-decade low, Bloomberg said.

- Brazil’s oil production rose to 3.757m b/d in June, up 10.1% year-on-year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: Specific Private Industries Worth Watching In NFP Report

Jul-02 2025 18:17

- Within industries of nonfarm payrolls, expect a continued focus on those more cyclically sensitive sectors, such as food & drinking places, for discretionary spending indicators.

- This category saw notable strength in May at +30k after +23k in April (average +11k in 2024) but maybe scope for a downward revision.

- Friday saw real consumer spending disappoint in May at -0.3% M/M (cons 0.0) with particular weakness admittedly in goods (-0.8%) but services also languished with -0.03% M/M for technically a third monthly contraction in the five months of the year to date.

- There could also be a calendar effect at play, with BofA warning that the earlier Memorial Day could weigh on leisure & hospitality more broadly.

- Transportation & warehousing should also be watched for a look at more direct impacts from US tariff policy. Recall that this category saw large downward revisions last month, leaving payrolls growth of +6k in May after -8k in April (initially +29k) and -21k in March (+3k) and changing a narrative around implications of inventory accumulation on warehousing roles in particular.

- The latest vintage points to a recent net negative impact from tariffs now having peaked with 28k and 34k monthly increases back in Nov and Dec.

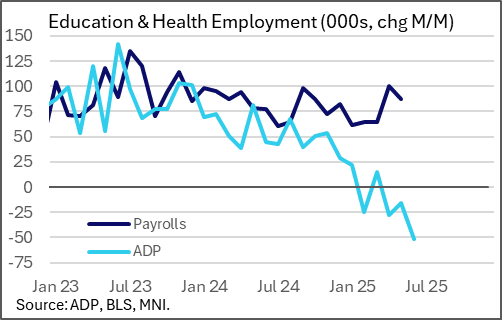

- Education & health services will also be watched closely after today's ADP employment report showed a yet further widening in what has been a puzzling disconnect with BLS payrolls.

US OUTLOOK/OPINION: Specific Factors Likely At Play In June Payrolls Report

Jul-02 2025 18:15

Nonfarm payrolls growth is expected at 110k in June per the broad Bloomberg consensus after a slightly stronger than expected 139k in May but one that was offset by a large two-month downward revision of -95k.

Specific factors at play this month:

- Returning strikers to add 5.6k to payrolls, with 1.4k on strike in the June reference period vs 7k in May (SAG-AFTRA and IAM strikes concluded).

- Supreme Court allows White House to revoke Temporary Protected Status (TPS) of ~350k Venezuelans. GS see this dragging 25k whilst UBS estimate 5k with a range of 0-10k. JPM on the matter note continued uncertainty: “However, a lawsuit related to this is still ongoing, and the TPS page for Venezuela says that TPS documentation granted before February 5, 2025 will remain valid until October 2, 2026 pending resolution of the case.”

- JPM also on the Supreme Court on May 30 allowing “the government to move forward with terminating parole granted to ~530k people under the CHNV program. That does not mean every parolee, though, will be deported, as some may have other status or a pending asylum case.”

PIPELINE: Corporate Bond Update: $2.2B SoftBank Group 4Pt Priced

Jul-02 2025 18:13

- Date $MM Issuer (Priced *, Launch #)

- 07/02 $2.2B *SoftBank Group $500M 3.75Y 6.5%, $600M 5.5Y 6.875%, $600M 7 Y 7.25%, $500M 10Y 7.5% (in addition to 3 Eur tranches: 4.25Y, 6Y & 8Y) Note, SoftBank Corp issued $1B over 2 tranches on Monday.

- 07/02 $800M *Korea Gas $300M 3Y SOFR+65, $500M 5Y +47

- 07/02 $800M #National Bank of Kuwait PerpNC6 6.375%

- 07/02 $500M *HIKMA Pharmaceuticals 5Y +135a

- 07/02 $500M #Qatar Insurance NC6 6.15%