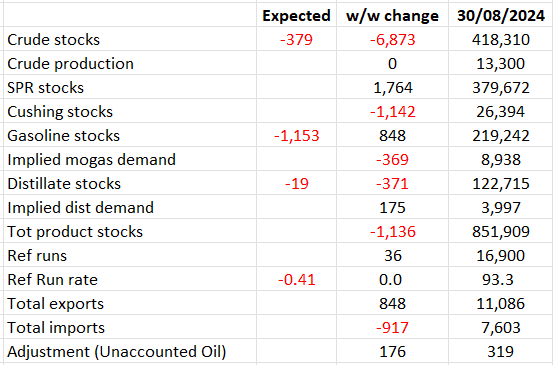

OIL: EIA Weekly US Petroleum Summary - week to Aug 30

Sep-05 15:02

- w/w change week ending Aug 30

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Equities Roundup: Stocks off 3M Lows, REITs, Transportation Led

Aug-06 14:58

- Stocks have rebounded after falling to the lowest levels since early May on the week opener. No particular headline driver, but a cautious continuation of buy interest following Monday's ISM services data that lessened concerns over an imminent economic recession.

- Currently, the DJIA trades up 520.51 points (1.34%) at 39235.9, S&P E-Minis up 84.75 points (1.62%) at 5302.75, Nasdaq up 272.6 points (1.7%) at 16475.76.

- Real Estate and Industrial sector shares led gainers in the first half, office and health care investment trust shares supporting the former: BXP Inc +4.33%, Alexandria Real Estate +3.13%, Welltower Inc +2.49%. Transportation stocks buoyed the Industrials sector: Uber +7.06% after announcing strong earnings this morning, CSX Corp +3.61%, Old Dominion +3.60%.

- Utility and Consumer Discretionary sectors underperformed in the first half, multi-energy shares weighed on the former: Sempra -1.09%, CenterPoint Energy +0.31%, Dominion Energy +0.7%. Meanwhile, autos and parts suppliers weighed on the Consumer Discretionary sector: Tesla -1.64%, Borg Warner +0.22%, Fors +0.46%.

- Expected earnings announcements after the close include the following: Illumina Inc, Devon Energy Corp, Fortinet Inc, Rivian Automotive, Astera Labs, Lumen Technologies, International Flavors, Reddit, Permian Resources, Wynn Resorts, Amgen Inc, Airbnb Inc and Super Micro Computer.

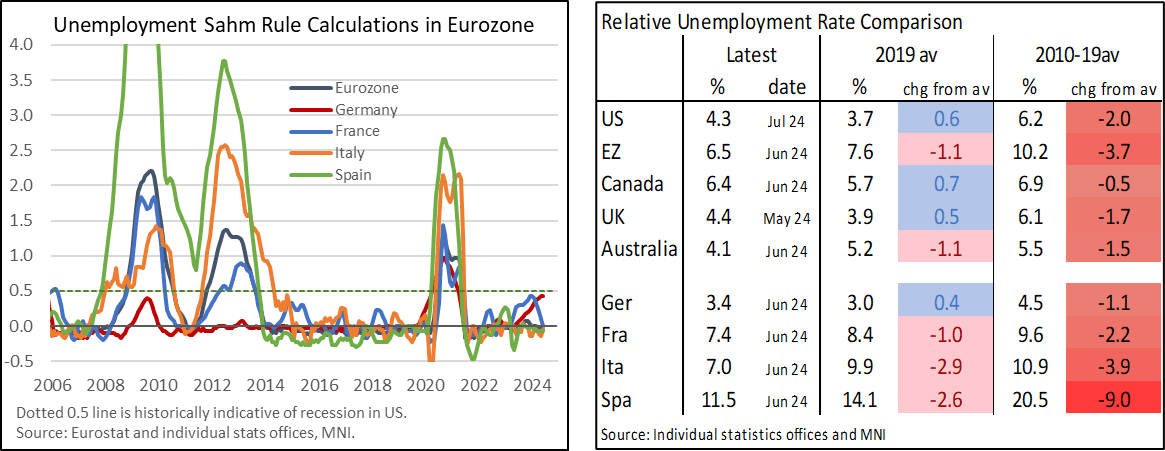

MACRO ANALYSIS: Germany Sees Greatest Relative Easing In European Labor Market [2/2]

Aug-06 14:53

- The country breakdown within the Eurozone is notable, with Germany a clear standout as its unemployment rate has been steadily trending higher whereas other major countries are broadly at zero on a Sahm Rule basis [using seasonally adjusted Eurostat data for June for comparability].

- The above points show recent trends and don’t necessarily account for how tight labor markets were, both at the start of the pandemic or how tight they became last year.

- Nevertheless, compare latest values with both 2019 averages and long-term historical averages (covering the sovereign debt crisis for the Eurozone) and this German relative underperformance within Europe continues to be seen [see table].

- Compared with 2019 averages, Canada, US, Australia and Germany have all seen broadly similar increases of 0.4-0.7pps and with other countries still notably tighter.

- All of the above countries continue to see tighter labor markets than their long-term averages, although Canada and Germany have closed the gap the most.

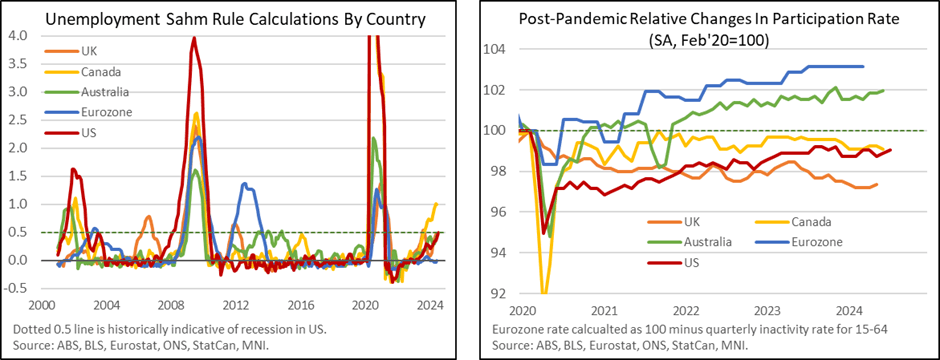

MACRO ANALYSIS: Eurozone Has Seen Far Less Labor Rebalancing Than DM Counterparts [1/2]

Aug-06 14:51

- Much has clearly been made of the rise in the US unemployment rate in Friday’s payrolls report for July, with the surprisingly high 4.25% near enough triggering the Sahm Rule (differences when calculating unrounded or rounded u/e rates aside).

- The measure lifting above 0.5 has historically been indicative of recession, although Powell in Wednesday’s FOMC press conference was keen to describe it as a “statistical regularity” rather than a rule. See more on this in the MNI Employment Insight here.

- Running this analysis across other DMs shows a similar labor market rebalancing in the UK and Australia, far greater moderation in Canada (helping the BoC to have already cut twice in June and July) but also essentially zero moderation in the Eurozone.

- The lack of a rise in Eurozone unemployment rate stands out especially if you also take into account it has seen the highest relative increases in participation rates since the pandemic.

- Eurozone participation (calculated as the inverse of the inactivity rate) stood 3pps higher in 1Q24 than it did pre-pandemic vs -1pp for the US, where the latter continues to see a reluctance of early retirees to return to the labor force.