US TSYS: Off Session Lows

Tsys have firmed off session lows, local participants perhaps focusing on the headline CPI print which was the lowest since April 2021. However moves have been modest with little follow through thus far. This leaves cash tsys ~1bp richer across the major benchmarks. TYM3 deals at 115-27+, 0-01+, a touch off the top of the 0-03+ range.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

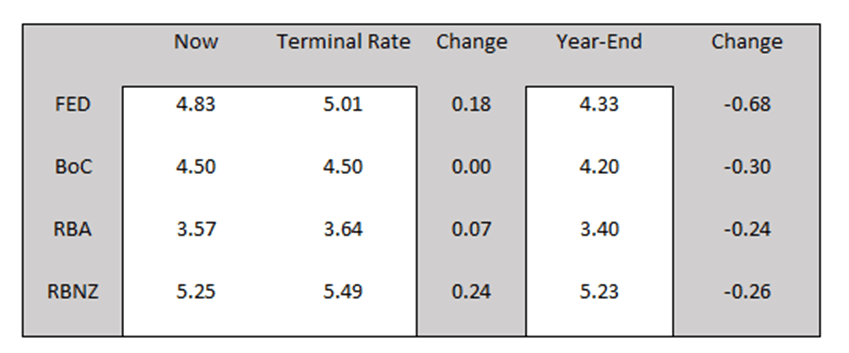

STIR: $-Bloc Firmer, US & CA STIR Leading

US STIR has firmed 5bp and 10bp respectively for the May and June FOMCs since the unexpected decline in the US unemployment rate to 3.5% (3.6% expected) last week. At the bell in NY trade, the Fed funds implied hike for May was 18.4bp and 18.8bp cumulative for June at 5.01% (expected terminal rate). There are 68bp of cuts priced for 2023.

- The BoC is expected to keep interest rates unchanged at its meeting on Wednesday, resulting in little change to the pricing for the April meeting, which currently indicates a 10% chance of a 25bp cut. However, pricing for meetings after June has firmed by 13-22bp since Wednesday's close, with December being the most affected, following the unexpected decline in unemployment rates in both Canada and the US.

- RBA dated OIS is 5-6bp firmer for meetings beyond August with December leading. A 25% chance of a 25bp hike in May is priced with year-end easing expectations at 24bp versus 29bp ahead of the Easter holiday.

- RBNZ dated OIS pricing is 2-4bp firmer across meetings today with 21bp of tightening priced for May. 26bp of easing is priced for Nov-23 off a terminal OCR expectation of 5.49% (July).

Figure 1: $-Bloc STIR: Terminal Rate Expectations & Year-End Pricing

Source: MNI – Market News / Bloomberg

US TSYS: Curve Marginally Steeper

Cash tsys have opened dealing flat to 2bps richer across the major benchmarks, the curve has bull steepened. Asia-Pac participants have faded Monday's cheapening, perhaps using the opportunity to close out short positions/enter fresh longs. TYM3 deals at 115-17+, +0-01, at the top of the narrow 0-02 range observed thus far.

- CPI and PPI data from China headlines the Asia-Pac session today, the print is due in just under 90 minutes.

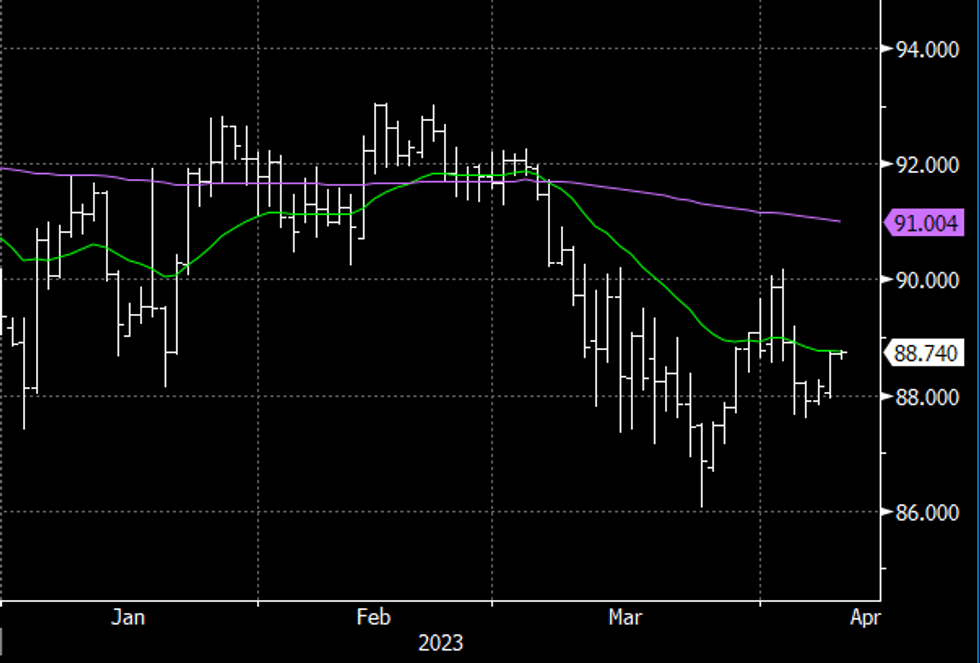

AUD: AUD/JPY: Supported Below ¥88

AUD/JPY has risen ~1.3% from April lows seen in the wake of last weeks RBA meeting. The pair sits a touch below its 20-Day EMA after bears failed to sustain a break of ¥88 handle.

- Previously highlighted comments from BOJ Governor Ueda pressured the Yen yesterday which aided the recovery in AUD/JPY.

- The cross however does remain well with recent ranges, a ¥86/90 range has been respected for the most part.

- Bears first look to sustain a break of ¥88 from here they can target 2023 lows at ¥86.06.

- Bulls look to sustain a break of the 20-Day EMA (¥88.76), from here they can target the 200-Day EMA at ¥91.00.

Fig1: AUD/JPY Daily Spot, EMAs

Source: MNI/Bloomberg