EM CEEMEA CREDIT: OCPMR: primary dual tranche USD benchmark 5Y and L10Y with FVs

OCP (OCPMR; Baa3/BB+pos/BB+)

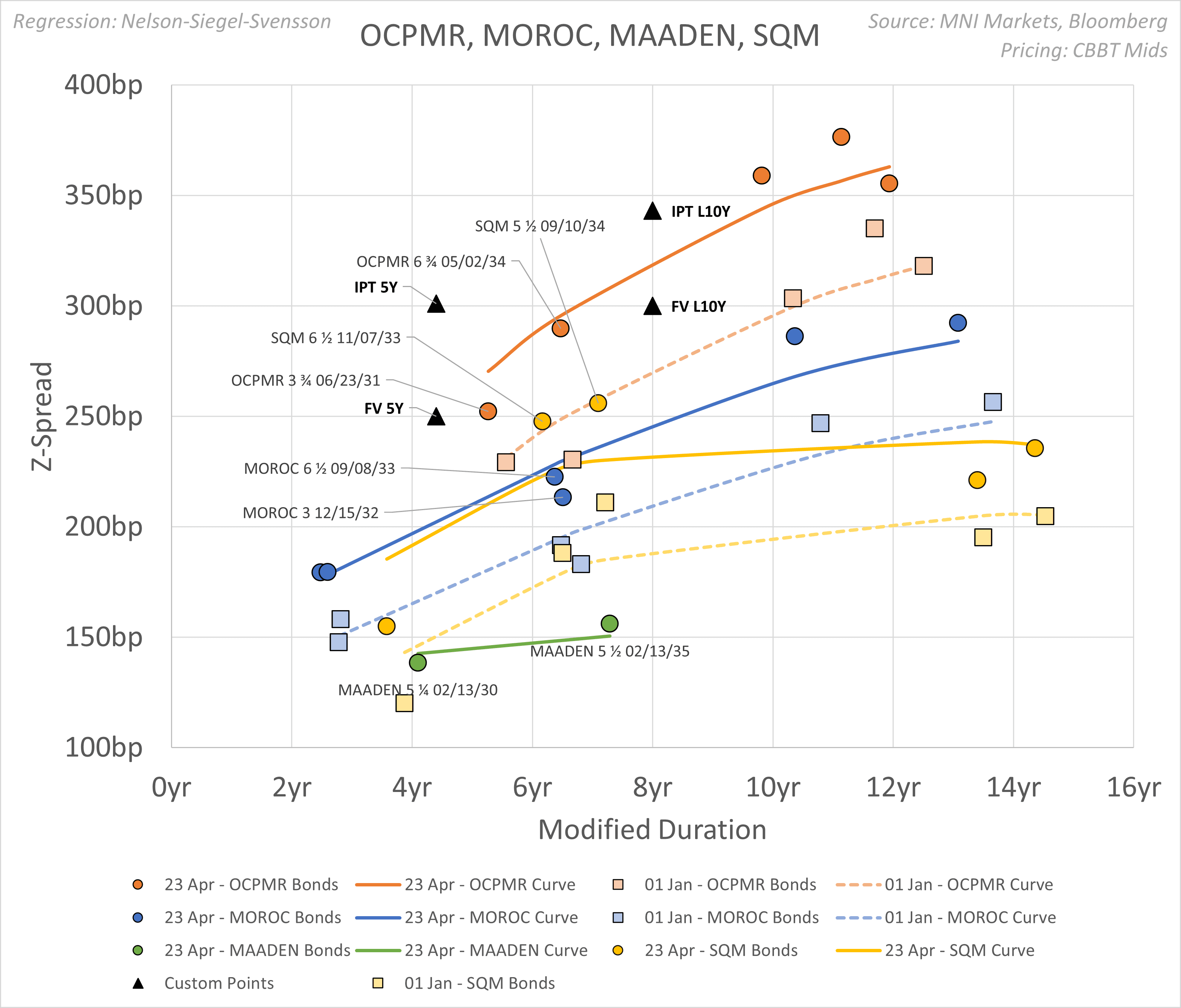

New issue deal: dual tranche USD benchmark 5Y and L10Y

IPT 5Y @ T+265bp area FV @ approx. T+214bp area (z+250bp)

IPT L10Y @ T+290bp area FV @ approx. T+246bp area (z+300bp)

- We see FV for 5Y bond at z+250bp (approx. T+214bp area) and FV for L10Y at z+300bp (approx. T+246bp area) as per chart below.

- Morocco’s government-related issuer, phosphate-based fertiliser producer OCP is in the primary market with a dual tranche new issue deal in USD. For perspective, we look at how secondary curves have moved YtD. We note that OCPMR curve has widened out more than the sovereign curve and similarly to SQM. OCPMR 31s spread move has been more modest compared to the longer end part of the term structure.

- We sketch our FV considerations looking at OCP’s seasoned bond curve (‘31s at z+252bp, ‘34s at z+290bp), the reference sovereign curve for Morocco (Ba1/BB+pos/BB+), as well as some of its higher rated, international peers, including Chile’s SQM (Baa1/BBB+/-) and Sukuk format, Saudi Arabia’s Maaden (Baa1/-/BBB+). We find less compelling comparables among bonds issued by US-based Mosaic, Norway’s Yara Intl and Israel-HQ ICL Group.

- For reference, Moody’s affirmed OCP’s ratings at Baa3 on stable outlook in mid-April, citing in line credit metrics and liquidity.

For context, OCP posted strong FY24 results back in March, showing strong growth in sales across geographies. Rev’s were up 8% YoY showing sequential quarterly growth to USD9.75bn equivalent (69% fertilizers). EBITDA up 35% YoY at USD3.9bn equivalent, EBITDA margin increased to 40%. Leverage was at 2.48x (vs 2.38x in FY23). Capex was higher vs previous year at USD4.38bn equivalent.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUNDS: /SWAPS: Off Lows On PMIs, DFA Confirms Issuance Plan

The long end leads Bund ASWs away from session lows, with spreads vs. 3-month Euribor last -0.3bp to +0.3bp.

- Softer-than-expected German services PMI data outweighed the firmer-than-expected manufacturing equivalent when it came to market reaction, with the latter aided by the well-documented fiscal developments.

- Elsewhere, the DFA has confirmed that it will sell EUR92.5bln of debt in Q225 (EUR62.5bln in bonds and EUR30bln in bills). We had previously suggested that the release would come too early to account for additional defence/infrastructure spending and expect related increases in issuance to start to filter in from Q3, at the earliest.

- That was in line with the wider sell-side train of thought as well.

MNI: EZ MARCH FLASH MANUF PMI 48.7 (FCAST 48.2, FEB 47.6)

- MNI: EZ MARCH FLASH MANUF PMI 48.7 (FCAST 48.2, FEB 47.6)

- MNI: EZ MARCH FLASH SVCS PMI 50.4 (FCAST 51.1, FEB 50.6)

STIR: Light Dovish Repricing In EUR Rates On Soft German Services PMI Details

The soft details of the German flash March services PMI has prompted a light dovish repricing in EUR rates, though ECB-dated OIS continue to assign a ~60% implied probability of a 25bp cut in April.

- OIS price 52bps of easing through year-end, up from 50bps before the PMI data.

- Euribor futures are now back to little changed through the blues.

- Although services activity remains subdued in Germany and France, there was a notable uptick in the manufacturing components in both PMIs. In Germany, this is likely to partly be a function of recent fiscal developments.

- MNI’s rough calculations suggest the Eurozone-wide flash manufacturing PMI, due at 0900GMT, could print close to neutral (i.e. 50) territory in March (vs 48.2 cons, 47.6 prior). That assumes countries excluding France and Germany also see an average ~2.5 point uptick relative to February. If the ex-France and Germany average manufacturing PMI was instead flat at 49.2, the Eurozone-wide PMI tracks at 48.8.

- Assuming the ex-France and German average PMI is unchanged at 53.9, we track the Eurozone-wide services flash unchanged at 50.6 (vs 51.1 cons).