BONDS: NZGBS: Richer With US Tsys But NZ-US10Y Wider

In local morning trade, NZGBs are 1-2bps richer after US tsys finished 4-7bps richer, with a steeper curve, in response to weaker equities.

- No specific headline or block-related trade can be cited for the move, although some desks pointed to an overreaction to the story about two regional banks being hit (Zions and Western Alliance Bancorp). The Financials sector led the decline, primarily due to insurers.

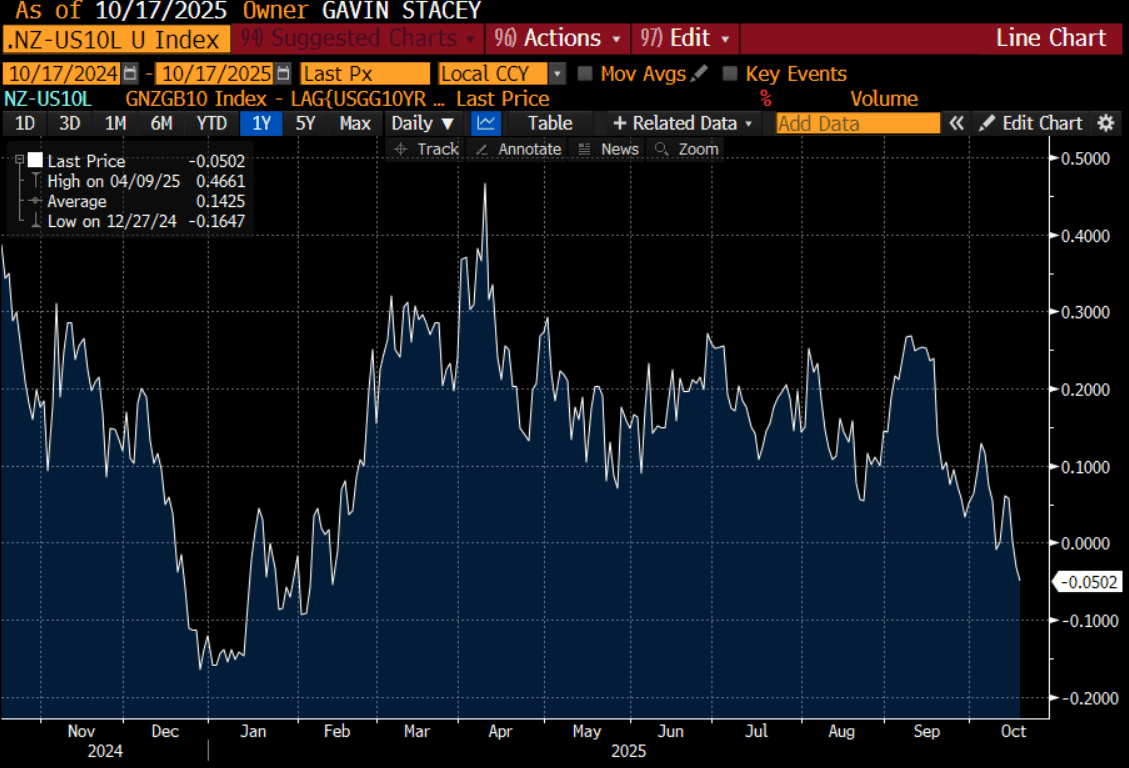

- The NZ-US 10-year yield differential is 2bps wider at flat. Nevertheless, the differential is holding around levels last seen in February. (see chart).

- Swap rates are 2-3bps lower, with the 2s10s curve slightly steeper.

- RBNZ-dated OIS pricing is little changed across meetings. 26bps of easing is priced for November, with a cumulative 37bps by February 2026.

- Today, the local calendar will be empty, ahead of Q3 CPI on Monday.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

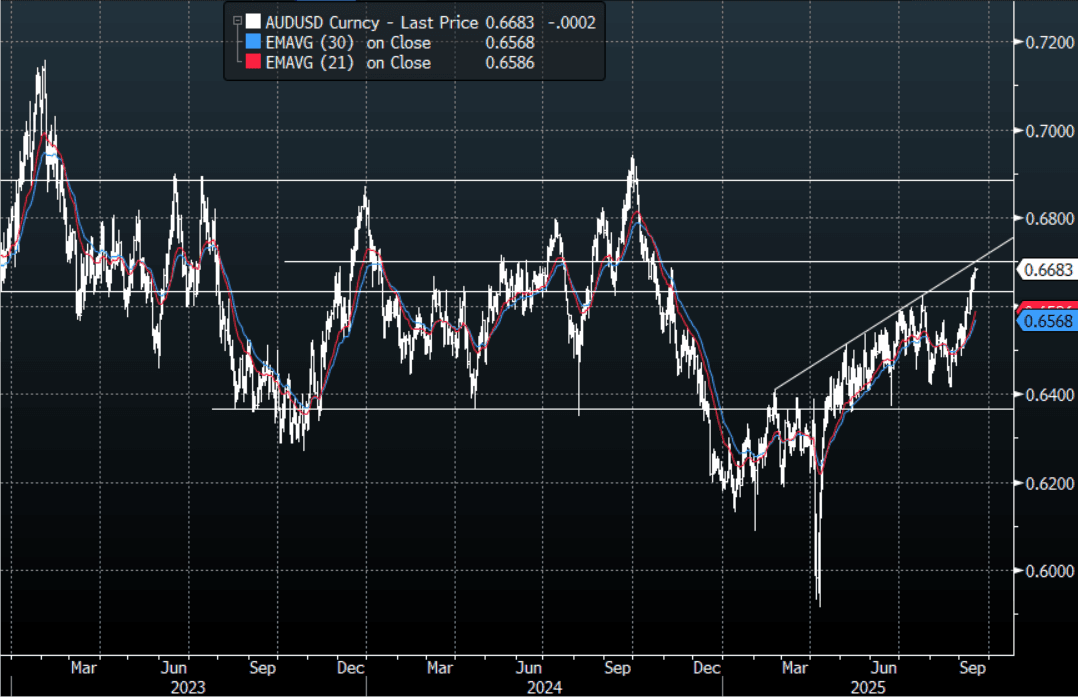

AUD: AUD/USD - Grinds Higher Into FOMC

The AUD/USD had a range overnight of 0.6660-0.6688, Asia is trading around 0.6680. US stocks finally paused for a breath ahead of the FOMC, but the USD can’t catch a break and looks to be breaking lower even before the market hears from Powell. The AUD continues to be supported and grind higher. How the USD reacts after the FOMC will be key as the market has already priced in some significant negativity. If the USD can follow through with this move then we could see the AUD gain momentum above 0.6650/0.6700 and potentially target levels back towards 0.6900/0.7000. The price action suggests dips will be supported for now as we await confirmation of this potential break higher, the first buy-zone is back towards the 0.6550 area.

- Bloomberg - “Australia Pension Fund Hedging to Double in Decade, RBA Says. Australia’s pension funds are set to double their foreign-exchange hedge books over the next decade as the A$4.3 trillion ($2.9 trillion) sector ramps up its exposure to overseas assets, said Reserve Bank Deputy Governor Andrew Hauser.”

- “RBA Is ‘Pretty Close’ to Inflation and Jobs Targets, Hunter Says. Australia’s central bank is “pretty close” to getting inflation back to the midpoint of its 2-3% target while the economy is near full employment, Assistant Governor Sarah Hunter said.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6650(AUD457m). Upcoming Close Strikes : 0.6600(AUD894m Sept 18), 0.6750(AUD1.16b Sept 19) - BBG

- CFTC Data last week shows Asset managers slightly increasing their shorts -68333(Last -66025), the Leveraged community pulled back the shorts they had just started to rebuild -5081(Last -11860).

- Data/Event: Westpac’s leading index for August prints today. The July 6-month rate was little changed at 0.06% signaling that the economic recovery is likely to remain gradual and lacklustre into year end. RBA Assistant Governor Brad Jones hosts a fireside chat at the Intersekt 2025 Conference in Melbourne

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

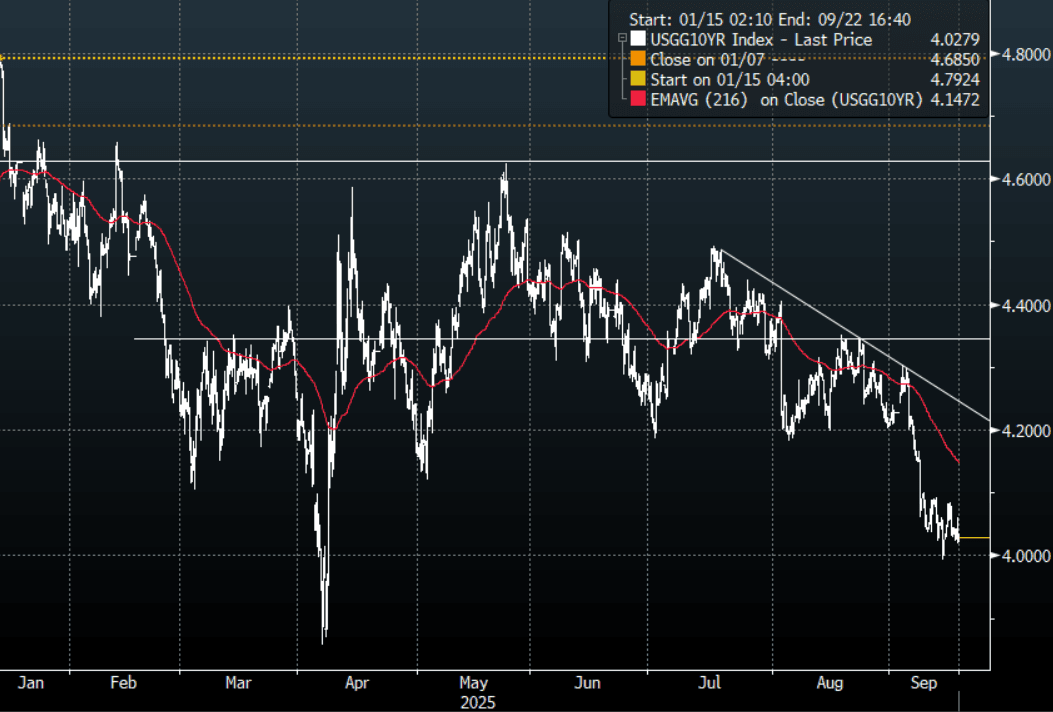

US TSYS: Yields Extend Lower, Led By The Front-End

TYZ5 reopens at 113-17, down 0-00+ from closing levels in today’s Asia-Pac session.

- Overnight the US 10-year yield had a range of 4.0184% - 4.0604%, closing around 4.028%.

- Treasury yields extended lower overnight; led by the front-end(2s10s +2.60 at 52.258, 5s30s +0.93 at 106.212).

- US DATA: Non-Store Retail, Autos Resilience Drives Strong Overall Sales Beat. August retail sales beat expectations in all departments, with higher revisions adding to the positive takeaways suggesting potential upgrades to Q3 personal consumption expenditures estimates.

- US DATA: NY State Service Firms Echo Manufacturing Weakness In Early September. Service firms in New York State got off to a similarly weak start to September as their manufacturing counterparts saw yesterday. These are the first September readings for the regional Fed surveys.

- 10-Year Yields continue to do work just above 4.00% as the market looks towards the FOMC this week. The first buy-zone is now back towards the 4.20% area where I suspect decent demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area. The market does seem confident and is pricing in a dovish outcome, the risk is Powell does not deliver.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

CNH: USD/CNH At Fresh Lows For 2025, But Lags Broader Dollar Weakness

USD/CNH tracks near 7.1050 in early Wednesday dealings. CNH rose 0.20% for Tuesday's session, as USD indices lost ground, the DXY down around 0.65%, while the BBDYX index fell by 0.50%. Dollar weakness continues in the lead up to the Fed meeting outcome, with better than expected US retail sales data on Tuesday not aiding dollar sentiment. EUR/USD got to fresh cycle highs of 1.1878, with CNH lagging broader dollar weakness. Spot USD/CNY finished up yesterday at 7.1144, while the CNY CFETS basket tracker fell by a further 0.20% to 96.335.

- For USD/CNH technicals, downside focus will rest on a test under 7.1000. Early Nov lows from last year came in at 7.0869. Key EMA resistance points continue to track lower, the 50-day now around 7.1560. EUR/CNH sits near 8.4300 in early Wednesday dealings, with early July highs at 8.4643 not too far away. CNH/JPY was last around 20.6130, lower, but still within Sep ranges.

- US-CH 2yr yield differentials are close to +207bps, around fresh cycle lows since early 2024. In the equity space, local onshore markets were mixed yesterday, but the Golden Dragon Index rose 1.8% in Tuesday US trade.

- Per our onshore China policy team: Beijing will pursue a 19-point action plan aimed at boosting service consumption across five key areas, the Ministry of Commerce said on Tuesday. According to the ministry, officials will cultivate platforms to stimulate service consumption and expand fiscal and financial support.

- US Tsy Secretary Bessent stated further talks will be held in Germany between US and China ahead of the Nov 10 reciprocal tariff deadline.