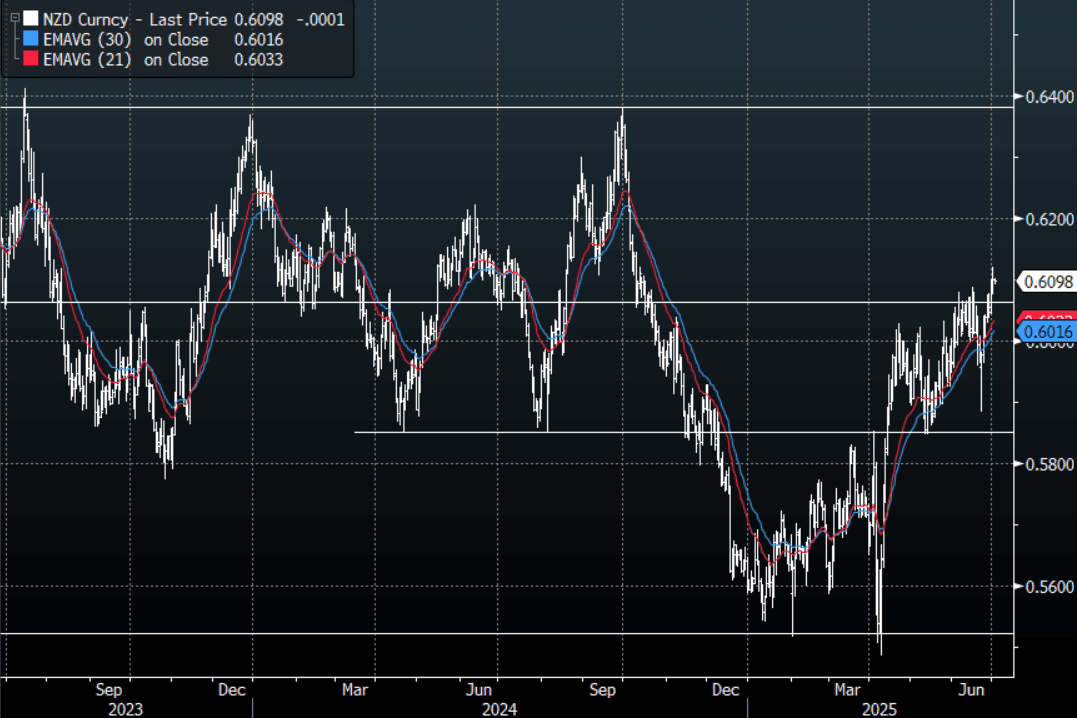

NZD: NZD/USD - Consolidates Around 0.6100, Eye's NFP On Thursday

The NZD/USD had a range overnight of 0.6081 - 0.6120, Asia is trading around 0.6100. The pair is breaking through its recent highs and attempting to build momentum for a potential look back towards the 0.6400/0.6500 area. The relentless pressure on the USD is providing a tailwind and dips towards 0.6000 should continue to see demand. The market will be eyeing NFP on Thursday so there is a good chance we will consolidate until we see if that gives the USD a further nudge lower.

- Whole Milk Prices Nearly 12% Off May Highs : Overnight the whole milk price auction saw a sharp fall. We fell to $3859 from $4084 prior, which was a 5.1% drop between the two auctions. The whole milk price is off close to 12% from its highs at the start of May.

- A huge bounce from sub 0.5900 and the NZD has now established a foothold above 0.6000, with the USD breaking lower the NZD/USD looks to be building for a potential break higher of its own. A clear break of 0.6100 could provide the momentum to begin a larger move higher, initially targeting the 0.6400/0.6500 area.

- CFTC Data shows Asset Managers have cut their shorts and are now beginning to build a long in NZD +12195, the Leveraged community maintained their short that had just been added to -11981.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5800(649m). Upcoming Close Strikes : none.

- Data/Event : Cotality Home Value

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: AUD/USD - Trades Sideways On A 0.6400 Handle

The AUD had a range Friday night of 0.6408 - 0.6448, Asia is opening around 0.6440. Friday moves were dictated by what looked to be a potential breakdown in US-China relations along with month-end covering which saw US stocks move lower and also supported the Bond market.

- Bloomberg - “ Donald Trump’s decision to double steel tariffs on imports was “inappropriate” but it won’t impact Australia any more than it would other countries. Prime Minister Anthony Albanese said the US President’s move to increase tariffs on steel and aluminum to 50% from 25% was “an act of economic self harm by the United states that will increase the cost for consumers in the US.”

- “Australian home prices rose for the fourth consecutive month, driven by interest rate cuts and expectations of further cuts later this year.”(BBG)

- The AUD continues to hold up pretty well against the USD so If you want to express a short it looks best to do that in the crosses for now.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend. A break above 0.6550 and the move higher could begin to accelerate.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6400(AUD586m), 0.6425(AUD454m), 0.6575(AUD445m). Upcoming Close Strikes : 0.6490(AUD 787m June 5)

- CFTC Data shows Asset managers pared back their shorts ever so slightly, the Leveraged community though added to their shorts quite aggressively over the week.

Data/Event: S&P Global Australia PMI, Melbourne Institute Inflation, ANZ - Job Ads

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg

US TSYS: 10-Year Yield Testing Support Below 4.40%

TYU5 reopens at 110-27, up 0-03 from closing levels in today’s Asia-Pac session.

- Friday night US 10-year yields had a range of 4.3846% - 4.4378%, closing around 4.40%.

- Treasury yields ended generally lower overnight, the front-end led the move causing the yield curve to steepen (2s10s +1.93 at 49.669, 5s30s +4.91 at 96.536).

- Chicago Business Barometer™ - Slowed To 40.5 In May: The Chicago Business Barometer™, produced with MNI, slowed 4.1 points to 40.5 in May. This was the second consecutive fall, bringing the index to its lowest level since January. The index has now been below 50 for eighteen consecutive months.

- US DATA: Rare Supercore PCE Deflation But Robust Market-Based Metrics: Core PCE inflation was completely in line with expectations for April on a M/M basis, at 0.116% M/M (unrounded analyst average 0.12).

- This marginal sequential firming in core PCE (from 0.09% to 0.12%) came despite a particularly weak core services ex-housing (supercore) at -0.02% M/M in Apr after 0.15% M/M. Supercore last saw M/M deflation in Mar and Apr 2020.

- The 10-year has come back down to test its support around 4.35/40%, likely aided by month-end rebalancing. Yields need to hold above this area to continue to build for a move higher.

ASIA: Coming Up In Asia-Pacific Markets On Monday

2300GMT 0700HKT 0900AEDT Australia S&P Global PMI Mfg May F

2350GMT 0750HKT 0950AEDT Japan Capital Spending Q1

2350GMT 0750HKT 0950AEDT Japan Company Sales/Profits Q1

0030GMT 0830HKT 1030AEDT Japan Jibun Bank PMI Mfg May F

0100GMT 0900HKT 1100AEDT Australia MI Inflation Gauge May

0130GMT 0930HKT 1130AEDT Australia ANZ-Indeed Job Ads May

0200GMT 1000HKT 1200AEDT South Korea Sell KRW2.3tln 2-Yr Bonds