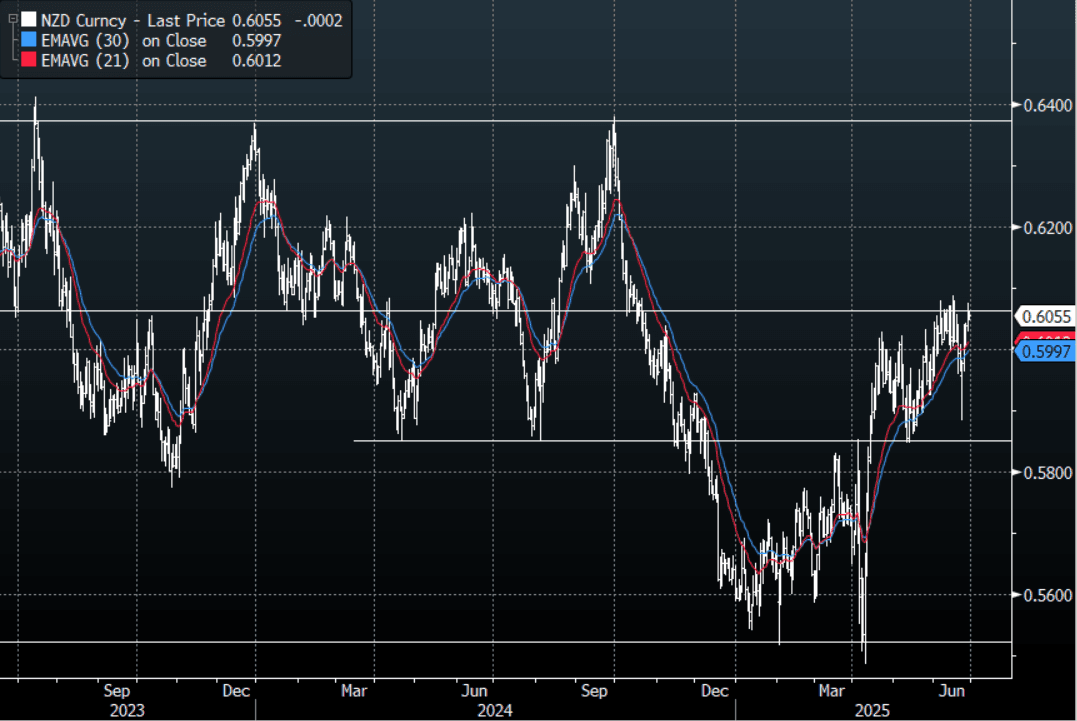

NZD: NZD/USD - Consolidates Above 0.6000

The NZD had a range overnight of 0.6043 - 0.6074, Asia is trading around 0.6055. A subdued overnight session, as NZD/USD consolidates above 0.6000. The USD has broken some key levels and is still looking vulnerable, this could see the NZD/USD continue to probe the 0.6100 area looking to gain some momentum to ultimately break higher.

- Bloomberg - "The labor market is not returning to sustained job growth, with high-frequency employment indicators showing a continued retreat in jobs over the second quarter."

- “Business surveys suggest additional weakness in hiring lies ahead, and policymakers will need to incorporate greater labor market slack into their August forecast update, which may lead to a need to take the Official Cash Rate below neutral later this year.”

- "NZ JUNE CONSUMER CONFIDENCE INDEX RISES TO 98.8, ANZ JUNE CONSUMER CONFIDENCE RISES 6.4% M/M: ANZ" - BBG

- A huge bounce from sub 0.5900 and the NZD has now established a foothold above 0.6000, with the USD breaking lower the NZD/USD looks to be building for a potential break higher of its own. A clear break of 0.6100 could provide the momentum to begin a larger move higher, initially targeting the 0.6400 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5850(NZD404m July 1)

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Upcoming OPEC Decision Concerning Oil Market

Oil sold off on worries that OPEC will decide to increase output substantially again at its meeting on the weekend. The USD index rose 0.5% which also pressured dollar-denominated crude.

- WTI fell 0.75% to $61.07/bbl after a low of $60.26 but is still up 6% in May. It has started today around $61.12. Initial resistance is at $62.71, 50-day EMA, with the bear trigger at $54.33.

- Brent is down 0.7% to $64.29 after falling to $63.50. It is now up 5.3% this month. It continues to trade well above the bear trigger at $58. Initial resistance is at $66.13, 50-day EMA.

- OPEC meets on May 31, a day earlier than originally scheduled, and there have been reports that it is considering another large production increase for July after two already in Q2. A market surplus in 2025 and 2026 has been forecast for some time and this would result in a widening of projections.

- With it becoming increasingly clear that Russia is not looking for a peace deal in Ukraine, the prospect of an easing of sanctions is fading. In fact, the situation appears to be moving in the other direction with Europe imposing new measures against Russian financial intermediaries and its shadow fleet and the US is now considering whether to impose new sanctions. There have also been discussions on reducing the G7 price cap.

- Chevron has been granted a US licence to retain its infrastructure in Venezuela, according to Reuters, but production will need to be wound down.

NZD: NZD/USD - Fails Above 0.6000 Again, RBNZ today

The NZD had a range overnight of 0.5940 - 0.5996, Asia is trading around 0.5950. The short bonds and short USD trade finally got a reprieve thanks to a Reuters report that the Japanese finance ministry was considering shifting its issuance profile away from long-dated paper. This has seen the NZD fail once again above 0.6000, the RBNZ will dictate price action our session.

- MNI RBNZ Preview-May 2025: May 25bp Cut, Then?

- The RBNZ decision is announced today and rates are widely expected to be cut 25bp to 3.25% bringing total easing this cycle to 225bp. 23 out of 24 analysts surveyed by Bloomberg are forecasting this outcome.

- Given heightened uncertainty, the MPC is likely to retain its easing bias again stating it has “scope” to cut rates further if required and its updated OCR path will be scrutinised to this end. A downward revision bringing the terminal to below 3%, estimated 'neutral', would signal a need for accommodation.

- The attention will be on the medium-term which is likely to show a softer outlook driven by weaker trading-partner growth due to recent global uncertainty. The RBNZ said in April that “on balance, these developments create downward risks to the outlook for economic activity and inflation in New Zealand”.

- The NZD continues to trade in a 0.5850/0.6050 range, another failure above 0.6000 and with corporate month-end in play expect more demand for USD’s over the next day or 2.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. A break above 0.6050 is needed to provide the spark for the next leg higher.

- CFTC Data showed Asset managers maintaining their shorts, while the leveraged community added a decent clip back to their own short.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5725(NZD1.09b). Upcoming Close Strikes : 0.5975(NZD400m May 29)

Data/Event : RBNZ

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

CNH: USD/CNH Rises On Broad USD Gains, CNH/JPY Rebounds

USD/CNH tracks near 7.1900 in early Wednesday dealings, with CNH losing close to 0.20% for Tuesday's session, as the USD rebounded across the board. Broader USD index gains were up around 0.50% for the BBDXY and near 0.60% for the DXY. Spot USD/CNY finished up at 7.1950 on Tuesday. The CNY CFETS basket tracker still edged down to 95.80 for Tuesday (per BBG), despite modest yuan outperformance versus USD gains elsewhere.

- For USD/CNH, the 20-day EMA resistance point is around 7.2140, while May 20 highs were at 7.2263. May 9 highs rested near 7.2530, which is also close to the 200-day EMA. Recent YTD lows were at 7.1616.

- Dollar gains were strong against the yen, which lost a little over 1% versus the USD on Tuesday, as Rtrs reported the Japan MoF may shift composition of its current issuance programme away from super-long-end instruments. This drove a sharp fall in long end JGB yields, which also spilled over to US Tsys.

- This helped a global equity rebound, with US markets outperforming (SPX +2.05%) (were aided by higher US consumer confidence data as well). In Tuesday US trade the Golden Dragon index lost 0.28%. The China to global equity ratio is back to April lows, a CNH headwind all else equal. To recap, the CSI 300 lost 0.54% for Tuesday's session.

- CNH/JPY rebounded, from lows just under 19.80, we sit back above 20.05 in early Wednesday dealings.

- The local data calendar is empty until Saturday's official May PMI prints.