US: More Americans Disapprove Than Approve Of Big Beautiful Bill

Jul-24 18:08

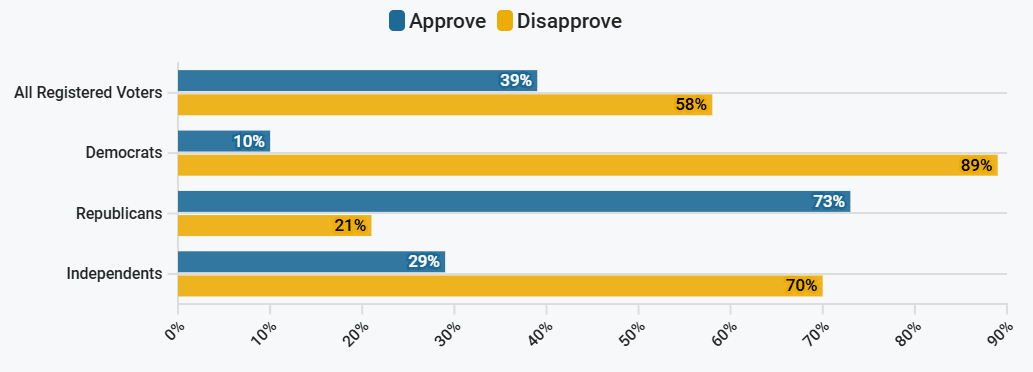

A new Fox News survey has found that more Americans, “disapprove (58%) than approve (39%) of the GOP’s ‘One Big Beautiful Bill’ by 19 percentage points, and more than twice as many think the law will hurt rather than help their family.”

- Fox notes: “Significant shares of Trump’s base also oppose the bill, including 52% of rural voters, 46% of White men without a college degree, and 37% of White evangelical Christians.”

- Fox adds: “Topping the list of things in the law that voters dislike is increasing the debt ceiling (74%), as three-quarters disapprove. More than half also disapprove of reducing food stamp funding (65%), making tax cuts permanent for those with higher incomes (64%), increasing spending for immigrant detention centers (59%) and the border wall (55%), ending wind and solar tax credits (58%), and increasing work requirements for Medicaid (53%).”

- There is some concern amongst Republicans that Trump's administration's failure to contain the fallout of the Jeffrey Epstein scandal could impact Republican lawmakers' ability to build support for the GOP's flagship legislation during next month's Congressional recess.

Figure 1: “Do you approve or disapprove of the federal budget legislation President Trump recently signed into law that he calls the “One Big Beautiful Bill”?”

Source: Fox News

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Sep'25 5Y Sale

Jun-24 18:03

- -6,500 FVU5 108-22, sell through 108-22.25 post time bid at 1355:01ET, DV01 $281,000.

- The 5Y contract trades 108-21.5 last (+2.25)

PIPELINE: Corporate Bond Update: Waiting for IFC, American National Group

Jun-24 17:57

At least $16.45B to price Tuesday

- Date $MM Issuer (Priced *, Launch #)

- 06/24 $2.5B #Kazakhstan $1.35B 7Y 5%, $1.15B 12Y 5.5%

- 06/24 $2.25B #Nomura $1B PerpNC5.5 7%, $750M 5Y +105, $500M 10Y +120

- 06/24 $2.2B #Imperial Brands $850M 3Y +85, $850M 10Y +140, $500M 30Y +158

- 06/24 $2B International Finance Corp (IFC) 5Y SOFR+41

- 06/24 $1.5B #Toyota $500M 2Y +38, $500M 5Y +60, $500M 10Y +77

- 06/24 $1.5B #Westpac $750M 5Y +50, $750M 5Y SOFR+82

- 06/24 $1.5B *Denmark 2Y +4

- 06/24 $1B *JBIC 3Y SOFR+44

- 06/24 $1B *CAF 3Y SOFR+69

- 06/24 $500M #China Development Bank 5Y SOFR+30

- 06/24 $500M #Ladder Capital 5Y +167

- 06/24 $Benchmark American National Group 10Y +175

- Expected Wednesday:

- 06/25 $Benchmark Swedish Export Cr 2Y SOFR+36a

BONDS: EGBs-GILTS CASH CLOSE: German Long End Underperforms On Issuance Concerns

Jun-24 17:56

European FI traded mixed Tuesday, with Gilts gaining and easily outperforming Bunds, and periphery EGB spreads tightening.

- Germany's Q3 issuance plan was in line with expectations though the curve steepened on indications of possible 50Y issuance, helping pressure the broader FI space. But lower oil prices on the overnight US/Iran/Israel de-escalation helped subdue any short-end yield rise.

- Global core FI regained ground by middle of the European afternoon however, led by Treasuries as Fed Chair Powell was seen to be open to earlier rate cuts if data warranted, while US consumer confidence and labor market indications were weaker than expected.

- In European data, German IFO Business Climate/Expectations beat expectations. There were several central bank speakers, with BOE's Ramsden perceived dovishly, while ECB's Lane drawing headlines for seeing some caution on services disinflation (though nothing really new).

- The German curve bear steepened on the day, with the UK's leaning bull flatter (out to the 10-year segment).

- Periphery/semi-core EGB spreads tightened in a risk-on session, with BTPs outperforming.

- Wednesday sees a quieter central bank communications schedule, with BOE's Lombardelli the lone scheduled speaker, while in data we get French consumer confidence and Spanish GDP/PPI readings.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.3bps at 1.851%, 5-Yr is up 2.1bps at 2.131%, 10-Yr is up 3.6bps at 2.543%, and 30-Yr is up 6.5bps at 3.026%.

- UK: The 2-Yr yield is down 1.7bps at 3.872%, 5-Yr is down 1.7bps at 3.991%, 10-Yr is down 1.9bps at 4.473%, and 30-Yr is down 0.4bps at 5.208%.

- Italian BTP spread down 5.5bps at 91.9bps / Greek bond spread down 3.5bps at 73.9bps