INDIA: Modi, Trump Reviewed "Good Progress" in Trade Negoiations

Oct-09 15:36

- In a post on X, India Prime Minister Narendra Modi says he spoke with US President Trump and congratulated him on the success of the Gaza peace plan. Modi also said the pair "reviewed the good progress achieved in trade negotiations" and "agreed to stay in close touch over the coming weeks."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Narrowly Mixed, Lithium Miners Underperforming

Sep-09 15:26

- Stocks trade mixed, fluctuating in narrow ranges early Tuesday after sharply lower (more negative) than expected BLS payrolls annual revision. Near-term data risk is also keeping traders sidelined ahead of CPI and PPI scheduled Wednesday and Thursday.

- Currently, the DJIA trades up 97.2 points (0.21%) at 45611.61, S&P E-Minis down 4.5 points (-0.07%) at 6501.5, Nasdaq down 19.4 points (-0.1%) at 21779.68.

- Materials and Industrials sector shares underperformed in the first half: reports over Chinese lithium miner extending output weighing on Albemarle Corp -11.26%, Freeport-McMoRan -5.10%, Sherwin-Williams -3.12% and Steel Dynamics -2.40%.

- THe Industrials sector weighed by: Builders FirstSource -4.63%, Lennox International -4.21%, Carrier Global -3.95% and A O Smith -3.18%.

- On the positive side, Energy and Communication Services shares led gainers in the first half, a rebound in crude prices (WTI +1.14 at 63.40) helping oil and gas shares: Valero Energy +3.21%, Phillips 66 +2.66%, Marathon Petroleum +2.58% and ConocoPhillips +2.33%.

- Meanwhile, AT&T +1.87%, Paramount Skydance +1.32%, Alphabet +1.30% and Meta Platforms +1.12% buoyed the Communication Services sector in the first half.

US TSYS: Extending Lows

Sep-09 15:07

- Treasuries are extending lows at the moment, no particular headline or Block driver as many ply the sidelines ahead of CPI/PPI data next two sessions.

- Currently, the Dec'25 10Y trades -10 at 113-07.5 (yld 4.0856 +.0458) -- Initial firm support to watch is 112-11+, the 20-day EMA.

- Curves bear flattening: 2s10s -0.971 at 54.171, 5s30s -0.249 at 112.703.

- US$ gaining, BBG index BBDXY currently +1.51 at 1200.06 vs. 1196.69 post data low.

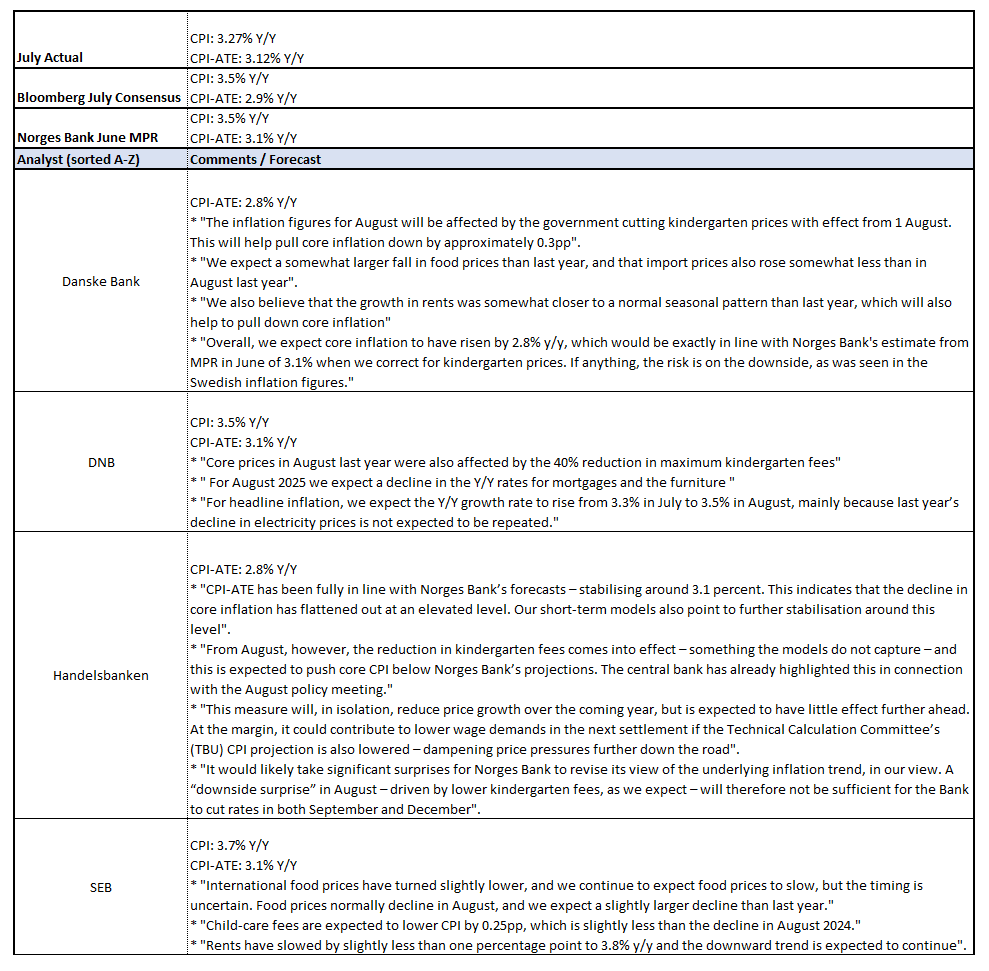

NORWAY: Preview: August Inflation Due At 0700BST/0800CET Tomorrow

Sep-09 15:01

Norwegian August inflation is due tomorrow at 0700BST/0800CET. Together with Thursday’s Q3 Regional Network Report, the data will be key in determining whether Norges Bank can deliver another 25bp cut on September 18.

- At its June and August decisions, Norges Bank Governor Wolden Bache said that the June MPR rate path was consistent with “one or two” more rate cuts this year (with implied probabilities skewed towards the quarterly MPR meetings in September and December). These comments keep the door open to a rate hold in September if this week’s data surprise in a hawkish direction – a risk markets may be underappreciating at present.

- Norges Bank’s June MPR projections for CPI-ATE are on track after two consecutive 3.1% Y/Y prints in June and July. In August, there are downside risks to the 3.1% Y/Y Norges forecast due to a reduction in child daycare prices in the 2025 Revised National Budget. From Norges Bank’s August monetary policy assessment: “Child daycare prices were reduced from 1 August 2025 and will thus be lower than assumed in the June Report. The reduction in child daycare prices will lead to lower 12-month inflation in the coming year and a modest improvement in household purchasing power but will probably have little impact on inflation further out”. That suggests Norges Bank are happy to look through the temporary policy change.

- The median analyst expects CPI-ATE inflation at 2.9% Y/Y in August, with forecasts ranging from 2.8-3.1%. A 3.1% Y/Y reading probably isn’t enough to derail a September cut just yet, but any higher and we think doubts should be increased - particularly if the Regional Network Survey is also hawkish.

- Alongside the daycare price impact, analyst previews we have seen generally expect a softening in food and rent inflation in August.

- Headline inflation is seen accelerating on an electricity base effect to 3.5% Y/Y (vs 3.3% prior), in line with Norges Bank projections.