STIR: Modest Dovish Move In Fed Pricing On PPI, Hawkish CPI Move Briefly Unwound

Jul-16 12:54

Fed pricing little changed to a touch more dovish in the wake of the softer-than-expected PPI data, which comes on the heels of yesterday’s CPI reading.

- Our macro team notes that the PPI reading screens neutral to a little dovish for PCE.

- A reminder that the CPI data pointed to tariff pressures across several core goods categories.

- FOMC-dated OIS shows 0.5bp of easing for this month, 14.5bp through September, 28bp through October and 45bp through year-end. Levels little changed to 1.5bp more dovish vs. pre-data levels.

- The hawkish repricing that followed yesterday’s CPI was retraced at one stage, before the initial post-PPI dovish move faded a little.

- SOFR-implied terminal rate pricing moves to ~3.25% vs. 3.28% pre-data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: Citi Recommend Adding To SFRZ5 97.00 vs. 0QZ5 97.375 Calls

Jun-16 12:54

Citi have recommended adding to an existing long SFRZ5 97.00 call vs. 0QZ5 97.375 call position at 5.0.

- They initially deployed this trade recommendation in April and write “while the mark-to-market has been slightly negative, we add. The vol. differential is in your favour on this structure, so the strike spread is below forwards”.

- This comes ahead of Wednesday’s FOMC, with Citi noting that they “expect a neutral to hawkish FOMC given the still-large uncertainty around the path of inflation. Our economists expect two cuts in the SEP for 2025, and that sounds reasonable to us with a risk for just one cut. Geopolitical moves make two cuts the likely outcome. To be clear, there are downside risks to the economy. Last week’s claims data could be the start of a seasonal uptrend, as seen the past few years. The front-end Fed funds market is pricing in a gradual easing cycle towards mid-3% in 2026. This is a reasonable modal outcome, but we think the downside tail risk, especially for 2025, is underpriced”.

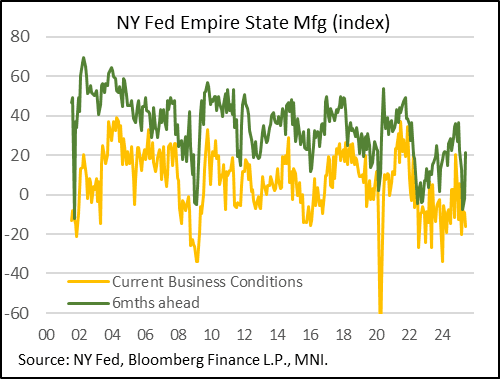

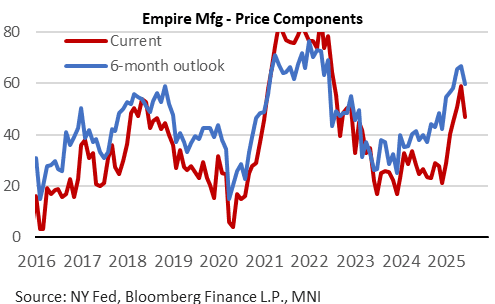

US DATA: Poor Activity, But Much-Improved Outlook In Empire Manufacturing Survey

Jun-16 12:52

The NY Fed's Empire Manufacturing survey unexpectedly saw the headline General Business Conditions index worsen in June, to a 3-month low -16.0 (-6.0 expected) vs -9.2 in April.

- This was a surprise as the Empire survey is conducted early in the month, and May's deterioration (-8.1 to -9.2) had been seen as not reflective of the May 12 US-China tentative tariff deal which saw sentiment improve in other surveys conducted later in the month.

- New orders pulled back sharply, from a positive 7.0 reading in May, to -14.2, a 3-month low, with shipments also declining. We also note higher delivery times and lower inventory levels, with the Supply Availability index ticking up to -8.3 from -11.4 but still suggestive of worsening supply availability.

- That said, this was a very mixed report as there was some notable improvement in other subindices. Most notably, the 6-month-ahead reading jumped to 21.2 (-2.0 prior), a 4-month high. And employment rose to the first positive reading (4.7, from -5.1 prior) since January, and the best level outright since December 2022, suggesting some hiring in the month.

- Even within the 6-month outlook, results were extremely mixed: "New orders and shipments are expected to increase, and firms expect supply availability to be only slightly worse in the months ahead. Capital spending plans remained soft." Indeed capex plans were the weakest since 2020.

- There is probably more noise in this report than signal, given how mixed these readings are (and how volatile the survey is even in normal times).

- One largely clear finding though was that inflation components in the survey eased from multi-year highs in May: prices paid fell to 46.8 from 59.0, with 6-month expectations falling to 59.6 from 66.7, suggesting that the worst of the perceived price pressures may be over.

US TSY FUTURES: BLOCK: Sep'25 10Y Ultra-Bond Sale

Jun-16 12:41

- -3,500 UXYM5 112-12, sell through 112-13 post time bid at 0832:13ET, DV01 $309,000.

- The 10Y ultra bond contract trades 112-13 last (-3)