MNI US Payrolls Preview: A Test Of Two Cuts Eyed For 2025

Jun-05 10:07By: Chris Harrison

Federal Reserve+ 4

Download Full Report Here

Executive Summary

- Nonfarm payrolls are seen increasing a seasonally adjusted 126k in May in the Bloomberg survey after a stronger than expected 177k in April (albeit one that was more than offset by negative revisions).

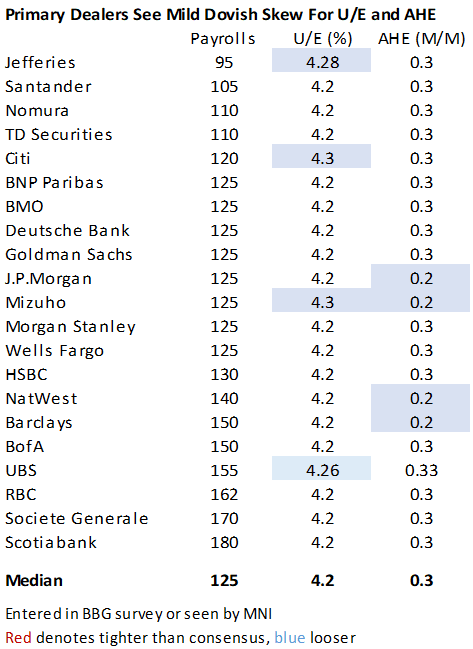

- Primary dealer analysts also see 125k whilst the Bloomberg whisper is weaker again, currently at 119k after Wednesday’s weak ADP release continued a clearly moderating trend.

- More analysts than not expect limited impact from the weather but that’s not a unanimous view.

- The industry breakdown will be watched for any weakness in trade & transportation after a strong April - likely on rapid inventory builds on tariff front-running - plus broader implications for discretionary demand.

- The unemployment rate is widely expected to round to 4.2% again after continuing to inch up to 4.19% in April. It would continue a broad plateau seen since last summer although there is mild dovish skew.

- Average hourly earnings are seen rising 0.3% M/M after a softer than expected 0.17% M/M in April, with the workweek watched after a recent recovery from January’s adverse weather lows.

- We expect greater sensitivity to a soft print in the event of a large surprise, although longer-term reaction would likely be capped by the FOMC not wanting a repeat of September’s (with hindsight) overreaction to a sharp but short-lived uplift in the u/e rate.

- A next Fed rate cut is almost fully priced for September before a second in December, both SEP meetings.