MACRO ANALYSIS: MNI US Macro Weekly: One Week, Two Labor Days

Aug-29 20:10

We've just published our latest US Macro Weekly - Download Full Report Here

- A busy pre-holiday week for data brought mixed economic signals and little net change in Fed easing expectations, putting next week’s labor day – Friday with its nonfarm payrolls report, of course, with apologies to Monday’s federal holiday – in focus for the FOMC and market participants alike.

- Second-quarter GDP was revised up by more than expected in the second reading, to 3.3% Q/Q SAAR, driven by better-than-previously estimated domestic demand but still leaving 1st half growth in slightly weaker territory vs last year. That said, the Atlanta Fed's Q3 GDPNow estimate jumped to 3.47% (though the implied contribution from net exports in the quarter looks somewhat dubious, as we explain).

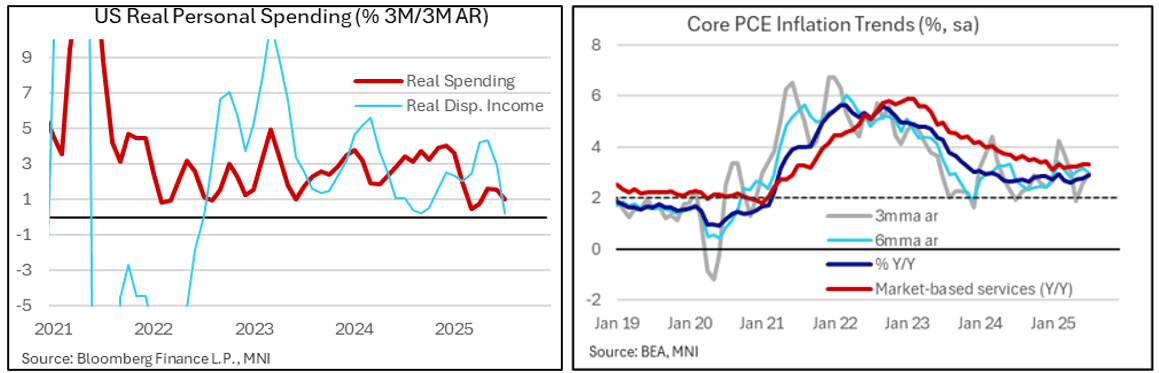

- The other major release of the week was July's Personal Income and Outlays report, which showed a modest uptick in income and spending on the month. However, the broader trends remain mixed at best, as real disposable income growth remains soft and services consumption is failing to regain traction.

- Core PCE inflation was close to expectations in July as the Y/Y accelerated to 2.9% for its fastest since February as it moves further away from recent lows of 2.6% having stalled above the 2% target. Recent trend rates are a little hotter but the median FOMC member will still need to see a further acceleration to meet their 4Q25 forecasts from June.

- Labor data were mixed. Latest jobless claims were in line to slightly better than expected, with initial claims trending a little higher but still impressively low whilst continuing claims are broadly plateauing after sharper increases in 1H25. But within the Conference Board consumer survey, the labor differential edged lower again, suggesting a continued upward trend in the unemployment rate.

- Elsewhere: regional Fed activity surveys were individually mixed, but combined generally showed an improvement in both manufacturing and services activity albeit with continued upside price pressures.

- Consumer sentiment (UMichigan and Conference Board surveys) and housing activity remained soft.

- Apart from Gov Waller again making the case from rate cuts, other FOMC colleagues who commented this week were a little more guarded when it came to the need for easing, to our ear.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Trump Remarks On Health Technology Underway Shortly

Jul-30 20:01

President Donald Trump is shortly due to deliver remarks at the White House on 'Making Health Technology Great Again'. LIVESTREAM

- According to ABC News, Trump is expected to unveil a plan that would create a system to ease the exchange of patient information.

AUDUSD TECHS: Clears The 20- And 50-day EMAs

Jul-30 20:00

- RES 4: 0.6700 76.4% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6688 High Nov 7 ‘24

- RES 2: 0.6677 0.764 proj of the Jun 23 - Jul 11 - 17 price swing

- RES 1: 0.6538/6625 High Jul 29 / 24 and the bull trigger

- PRICE: 0.6432 @ 20:01 BST Jul 30

- SUP 1: 0.6430 Low Jul 30

- SUP 2: 0.6373 Low Jun 23 and a bear trigger

- SUP 3: 0.6354 38.2% retracement of the Apr 9 - Jul 24 upleg

- SUP 4: 0.6323 Low Apr 16

AUDUSD has this week traded through both the 20- and 50-day EMAs. This undermines a recent bullish theme and signals the likely start of a corrective cycle. The next support was cleared Wednesday at 0.6455 the Jul 17 low. The clear break of this level strengthens a bearish threat and signals scope for an extension towards 0.6373, the Jun 23 low. Key resistance has been defined at 0.6625 the Jul 24 high. It also represents the bull trigger.

US TSYS: Fed Holds Steady, No Decision on Next Meeting

Jul-30 19:53

- Treasury futures are near late session lows, curves bear flattening as projected rate cuts into year end continue to cool after Chairman Powell said the FOMC has not yet made a decision on what it will do at its next policy meeting in September, adding that current policy is appropriate and there is lots of data between now and then.

- Projected rate cut pricing retreated vs. this morning/pre-data (*) levels: Sep'25 at -11.8bp (-16.9bp), Oct'25 at -21.4bp (-29.1bp), Dec'25 at -37.1bp (-46.6bp), Jan'26 at -45.6bp (--55.6bp). Year end projection well off early July level of appr -65.0bp.

- Treasury futures had pared losses after the FOMC kept rate steady as Fed Govs Waller & Bowman dissented in favor of a 25bp cut. "The majority of the Committee was of the view that inflation is a bit above target, maximum employment is at target" Powell said. "That calls for modestly restrictive, in my way of thinking, modestly restrictive stance right now."

- Futures extended well past this morning's ADP/GDP/Core-PCE lows: Sep'25 10Y futures currently trades -10 at 111-01.5 vs. 110-30.5 low (111-14.5 high). Key support is 110-08+, the Jul 14 and 16 low. Clearance of this level would reinstate a bearish theme. First support is at 110-19+, the Jul 24 low. Curves shift to flatter: 2s10s -1.814 at 43.131, 5s30s -1.397 at 94.131.

- Cross asset: Stocks retreating (SPX eminis -20.0 at 6386.0), Gold weaker at 3271.82, Bbg US$ index remains well bid: 1218.99 (+9.01).