MACRO ANALYSIS: MNI US Macro Weekly: Not A Bad Economy

We've just published our US Macro Weekly - Download Full Report Here [This is a two-week edition of the US Macro Weekly, capturing the FOMC decision as well CPI, PPI and retail sales reports ahead of next week’s August PCE release]]

- The Fed restarted its easing cycle with a “risk management cut” at its September meeting, cutting 25bp to a range of 4.00-4.25%. That was expected, but the lack of conviction on the FOMC about the rate path forward was a key theme of the meeting’s release materials, as well as Chair Powell’s press conference.

- Despite a lower rate path signalled in the new Dot Plot including a further 2 cuts this year, a seeming lack of clarity on delivering those future rate cuts saw an early dovish market reaction subsequently reverse.

- From a macro perspective, while the latest Fed statement pointing to increased downside risks to employment and Powell’s comment that he no longer saw the labor market as “solid” conveyed concerns about economic weakness, the FOMC’s latest projections didn’t quite square with that perspective.

- Inflation is seen as a little more stubborn than had been expected in the prior set of projections, with upgrades to growth across the forecast horizon, and the unemployment actually seen steady/lower than had been previously expected. As Powell put it, “it's not a bad economy or anything like that.”

- Post-meeting FOMC speakers Miran, Kashkari and Daly all supported a September cut (Miran of course voting for 50bp), each citing potential labor market weakness. Kashkari’s reasoning sounded a lot like Powell’s: “it's not a bad labor market, but it's one that I think we need to pay a lot of attention to”.

- In data: the downward benchmark revision to payrolls was on the high end of expectations. Jobless claims data fired a warning shot a week ago, although much of the spike in initial was linked to ID fraud in Texas. Latest data then surprised lower, while continuing claims saw a fourth consecutive weekly decline.

- August retail sales beat expectations in all departments, with higher revisions adding to the positive takeaways triggering upgrades to Q3 personal consumption expenditures estimates. Indeed, the Atlanta Fed’s GDPNow is tracking quarterly annualized growth of well over 3%, driven by domestic demand.

- PPI started last week’s inflation releases with a report that relieved concerns about tariff-related price pressures whilst highlighting the volatile and revision-prone nature of the trade services category.

- CPI then followed and was marginally stronger than expected on a M/M basis for both headline and core, with the latter at a robust 0.35% M/M but with a more benign readthrough to core PCE. The MNI median of unrounded analyst estimates for core PCE is 0.21% M/M with potential skew to the upside.

- Data aside, analysts have made dovish changes to their rate views in the wake of the Fed meeting, with the most common change being a more front-loaded easing cycle. Analysts' views for further cuts this year range from zero to 50bp, with the median seeing Oct and Dec cuts aligning with the latest Dot Plot.

- The analyst median has also tipped toward seeing slightly more 2026 cuts: now 75bp (albeit almost an even split between the number seeing 50 and those seeing 75bp), vs 50bp median pre-meeting.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Late SOFR/Treasury Option Roundup: Year End Rate Cut Call Buying

Various upside call structures targeting more rate cuts than currently priced traded Wednesday, SOFR outpacing Treasury options for the most part - though paper bought over 100k TYV5 113 calls earlier, adding to some 78k Tuesday. Underlying futures trade modestly higher after the bell - paring gains slightly after mixed messaging in the July FOMC minutes. Projected rate cuts consolidate from midday high to near steady vs. early morning (*) levels: Sep'25 at -20.6bp (-21.1bp), Oct'25 at -34.1bp (-34.9bp), Dec'25 at -54.0bp (-54.1bp), Jan'26 at -65.4bp (-65.1bp).

- SOFR Options:

- Block, 5,000 SFRH6 96.25/97.25 call spds, 26.5

- +50,000 SFRH6 97.25 calls, 6.0-6.5 covered

- +50,000 SFRZ5 96.18/96.31/96.50/96.62 call condors, 3.0-3.125 ref 96.205

- +15,000 SFRU6 96.00/96.25/96.50 put flys, 3.25

- +5,000 SFRU5 95.81 puts, 3.25 vs. 95.90/0.30%

- 3,500 SFRU5 96.00/96.12/96.25 call flys ref 95.8975

- -20,000 SFRU5 95.81/SFRZ5 95.87 put spds, 0.75 net/Sep over

- +4,000 SFRU5 95.62/96.31 call over risk reversals, 0.25 ref 95.9025

- 8,000 SFRU6 96.75/97.25 2x1 put spds ref 96.805

- 1,400 SFRZ5 96.25/96.37/96.50/96.62 call condors ref 96.21

- Block, 4,500 SFRZ5 96.25/96.50/96.75/97.00 call condors, 6.0 ref 96.21

- 6,000 SFRU5 96.00/96.12/96.25 call flys ref 95.90

- 6,000 SFRU5 95.87/95.93 put spds ref 95.90

- Treasury Options: (reminder Sep options expire Friday)

- +10,000 USV5 119 calls, 16

- Block: -5,000 WNU5 117.5 puts 20 over the WNV5 116/119 put over risk reversal

- -8,000 TYV5 111.5 puts, 34 vs. 111-30.5/0.40%

- 1,700 FVU5 108.5 puts, 3.5 total volume over 6k

- 5,000 wk5 TU 103.75/103.87/104 put trees vs. TUU5 103.75 puts

- Block/screen, over 10,800 TYU5 111 puts, 2 vs. 111-22.5/0.08%

- over 5,600 TYU5 112 calls, 8 last

- over 5,300 TYU5 112.5 calls, 2 last

- over 103,600 TYV5 113 calls, 20-23 ref 111-24.5 to -25.5 (78k trade Tuesday)

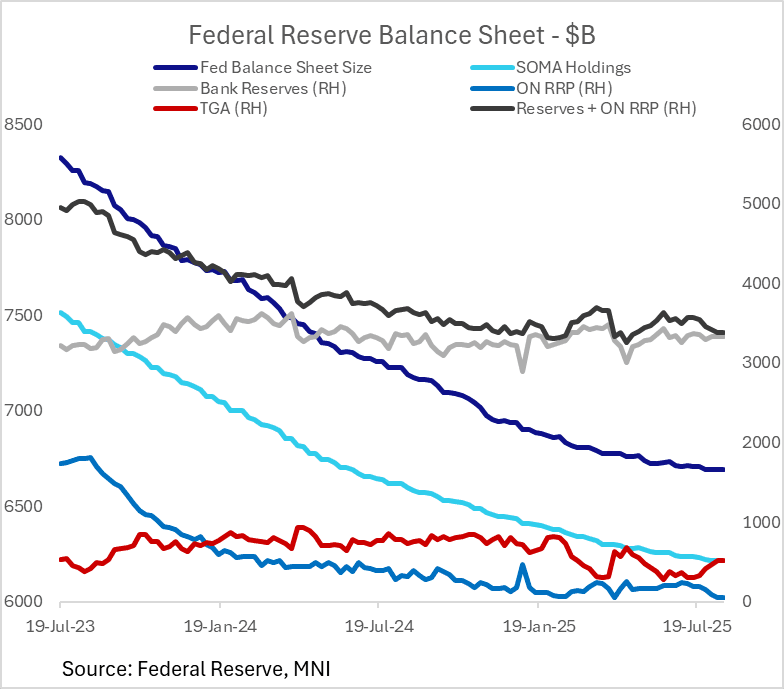

FED: July FOMC Minutes: Reserves "Abundant", Quarter-End SRF Takeup Eyed (3/3)

The July meeting devoted some discussion to the ongoing drawdown in reserves amid the Treasury cash rebuild. Overall, the Committee seem to be comfortable with the trajectory of reserves, despite some caution that reserves could be headed into "ample" from the current "abundant" territory.

- With regard to near-term funding pressures, namely potential for the mid-September tax date and Q3 quarter-end posing risks, the minutes suggest that while there may be some temporary acute liquidity issues, they can be resolved by takeup of the standing repo facility.

- As such, there was no real discussion of a shift in balance sheet management policy, particularly with QT proceeding "smoothly" and rerserves remaining "abundant", though vigilance of money market conditions would continue to be important.

- SOMA Manager Perli: "Market indicators continued to suggest that reserves remained abundant; however, ongoing System Open Market Account (SOMA) portfolio runoff, a substantial expected increase in the TGA balance, and the depletion of the ON RRP facility were together likely to bring about a sustained decline in reserves for the first time since portfolio runoff started in June 2022. Against this backdrop, the staff would continue to monitor indicators of reserve conditions closely. The manager also noted that there would be times—such as quarter-ends, tax dates, and days associated with large settlements of Treasury securities—when reserves were likely to dip temporarily to even lower levels. At those times, utilization of the SRF would likely support the smooth functioning of money markets and the implementation of monetary policy."

- And the broader FOMC: "Several participants remarked on issues related to the Federal Reserve's balance sheet. Of those who commented, participants observed that balance sheet reduction had been proceeding smoothly thus far and that various indicators pointed to reserves being abundant. They agreed that, with reserves projected to decline amid the rebuilding of the TGA balance following the resolution of the debt limit situation, it was important to monitor money market conditions closely and to continue to evaluate how close reserves were to their ample level. A few participants also assessed that, in this environment, abrupt further declines in reserves could occur on key reporting and payment flow days. They noted that, if such events created pressures in money markets, the Federal Reserve's existing tools would help supply additional reserves and keep the effective federal funds rate within the target range. A couple of participants highlighted the role of the SRF in monetary policy implementation—as reflected in increased usage at the June quarter-end—and expressed support for further study of the possibility of central clearing of the SRF to enhance its effectiveness."

SOFR OPTIONS: BLOCK: Mar'26 SOFR Call Spread

- 5,000 SFRH6 96.25/97.25 call spds, 26.5 at 1504:25ET

- This after scale buyer over 50,000 SFRH6 97.25 calls, from 6.0-6.5 covered