US INFLATION: MNI US Inflation Insight: Tariff Evidence Seeping In

We've just published our US Inflation Insight - Download Full Report Here

- June’s softer-than-expected core CPI reading (0.23% M/M vs 0.29% MNI median, 0.13% prior) came with a notable composition in light of mounting tariff pressures.

- Namely, core goods inflation was stronger than expected (0.20% M/M vs 0.19% MNI median, -0.04% prior), but that was outweighed by core services slightly on the light side (0.25% M/M vs 0.27% MNI median).

- Ex-vehicle goods inflation jumped in what is arguably the clearest sign yet that tariffs are beginning to seep through into CPI. Indeed there was a broader increase in core goods inflation for a second month, with multiple core goods areas that are seen sensitive to tariffs seeing acceleration including apparel, recreation commodities and household furnishings and supplies.

- Against this backdrop, Regional Fed banks’ estimates of sticky/median Y/Y CPI rates appear to have bottomed in the spring, at least for now, at levels above pre-pandemic averages.

- That said, the June Producer Price Index report was roundly softer than expected - and certainly than feared given the context of rising tariffs - despite some upward revisions to prior. While core goods prices did indeed advance, and there continued to be problematic readings in categories such as durable goods, the rise was consistent with the increases seen over the last 6 months rather than a sudden surge.

- In short, this round of data didn’t settle the question of whether tariff-related price increase would be sufficiently acute to warrant holding rates for an extended period. As noted in the July Beige Book, Fed business contacts’ comments suggested “consumer prices will start to rise more rapidly by late summer."

- Post-PPI estimates of the Fed’s preferred core PCE gauge centered on 0.29% M/M for June vs 0.31% after the CPI report, still an increase from the 0.25% very tentatively eyed ahead of both CPI and PPI releases.

- Through this week’s inflation round, market pricing for Fed easing ended largely steady (with almost 50bp of cuts through end-2025 and a first cut by October), though not before CPI saw cuts pared on the stronger details and then PPI restored some confidence in future easing.

- Overall though, the Fed is set to stay on the sidelines for the summer.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

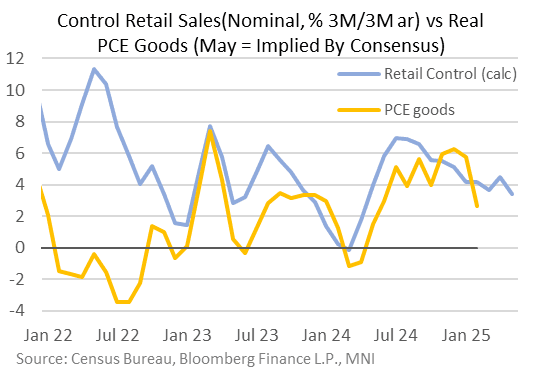

US OUTLOOK/OPINION: Analysts See Control Group Picking Up M/M In May (2/2)

As usual we expect the GDP-input Control Group sales to be the most closely watched part of the retail sales release - many analysts are centered around a 0.3% M/M (SA) advance in May's report. That would be an improvement from -0.18% but would still see the quarterly rate (3M/3M SAAR) pull back to a 13-month low 3.4%, after 4.5% in April, albeit those are both in nominal terms.

- A few comments by analysts, in alphabetical order:

- BofA (Control Group 0.0%): "Still in limbo...we forecast flat readings on both retail sales ex-autos and the control group"

- Citi: "We expect total retail sales to decline by 0.6%MoM mainly due to auto sales normalizing after some front loading in March and April. Control group sales should hold up better with strength driven narrowly by nonstore sales...A combination of trade-related uncertainty and pay-back from front-loaded activity should lead to softer economic conditions in coming months."

- Deutsche (Control Group +0.3%): Headline sales (-1.0%) should be pulled down by the drop in unit motor vehicle sales last month, while ex-autos (Unch) will likely see a drag from gasoline prices. However, we expect retail control (+0.3%) to rebound. As always, it will be important to pay attention to revisions."

- NatWest (Control Group +0.3%): "We expect (nominal) retail sales likely fell by -1.0% in May..we expect weakness in auto sales and gasoline station receipts weighed... In contrast, core retail sales which exclude autos and gas, likely rose by 0.3%m/m in May... we suspect retail sales in line with our forecasts are likely to translate into a small positive increase in real spending for May. This would put quarter-to-date (through May) average up at a strong 3.0%q/q, ar pace versus Q1 average (though slightly lower than the 3.7%q/q, ar pace at end of April)."

- TD (Control Group +0.3%): "Contracting auto sales will weigh on total US retail sales in May despite our expectation for a 0.3% m/m rebound in the control group segment. Auto sales are in the process of normalization following the front-loading of spending that lifted the series in March and April. Food services spending (bars & restaurants) likely also fell as well following firm increases in the last two reports."

- UBS (Control Group +0.3%): "We expect retail and food services sales fell 0.2% in May, with the headline held back by weaker auto sales...Ex-autos should look better, up 0.2% in May, with a similar 0.2% increase for ex-autos and ex-sales at gasoline stations...looking at the seasonal patterns in recent years, we have tended to see relative strength in control group sales in the month of May. However, this year the risks are more two sided."

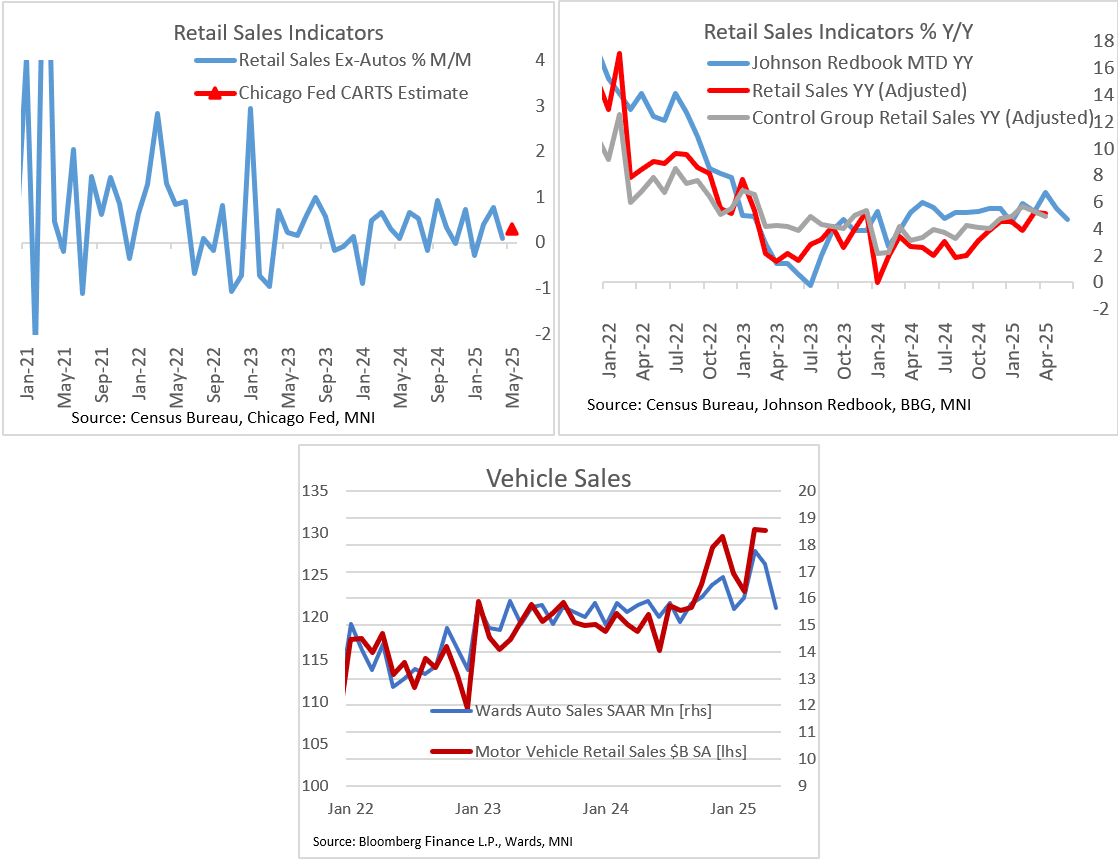

US OUTLOOK/OPINION: May Retail Sales Preview: Auto Drop To Weigh Heavily (1/2)

Tuesday's Census Bureau retail sales report for May is expected by consensus to show a 0.6% M/M (SA) fall, after +0.1% in April.

- That's due almost entirely to weaker auto and gasoline sales, with core metrics expected to pick up slightly per BBG median: ex-auto/gas 0.3% (0.2% prior), ex-auto 0.2% (0.1% prior), and Control Group 0.3% (-0.2% prior).

- Aside from gasoline prices dropping in the month (-2.6% M/M in CPI), Auto retailers are very likely to have seen a sharp pullback in May: US light vehicle sales (cars and light trucks) fell more sharply than expected in May, to 15.65M (16.00M expected, 17.27M prior), per Wards Automotive Group data. Note, autos are the single largest category of Census Bureau retail sales, and a May pullback would come after two record nominal highs in March and April in the category.

- Outside of that, sales data looked solid - and note that autos are not part of the Control Group measure.

- The latest Redbook Retail Sales Index showed 4.9% Y/Y growth in the last week of May (to May 31), a slowdown from 6.1% the prior week but still keeping total monthly sales at 5.5% Y/Y (vs retailers' 5.4% targeted gain).

- The Chicago Fed's Advance Retail Trade Summary (CARTS)'s final release for May projects that retail & food services sales excluding motor vehicles & parts (ex. auto) rose 0.3% M/M (SA) in the month.

USDCAD TECHS: Southbound

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4111 High Apr 4

- RES 2: 1.3861/1.4016 50-day EMA / High May 12 and 13

- RES 1: 1.3732 20-day EMA

- PRICE: 1.3555 @ 17:25 BST Jun 16

- SUP 1: 1.3535 1.0% 10-dma envelope

- SUP 2: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 3: 1.3473 Low Oct 2 2024

- SUP 4: 1.3410 1.764 proj of the Feb 3 - 14 - Mar 4 price swing

The trend needle in USDCAD continues to point south and fresh cycle lows last week and again today, reinforce a bearish theme. Support at 1.3686, the May 26 low and a bear trigger, has been cleared, confirming a resumption of the downtrend. This maintains the price sequence of lower lows and lower highs. Sights are on 1.3535 next, envelope-based support, and 1.3503, a Fibonacci projection.Resistance at the 20-day EMA is at 1.3732.