MNI US CPI Preview: Passthrough Pressure Mounting

Jul-14 18:24By: Tim Cooper and 1 more...

Inflation

Download Full Report Here

Executive Summary

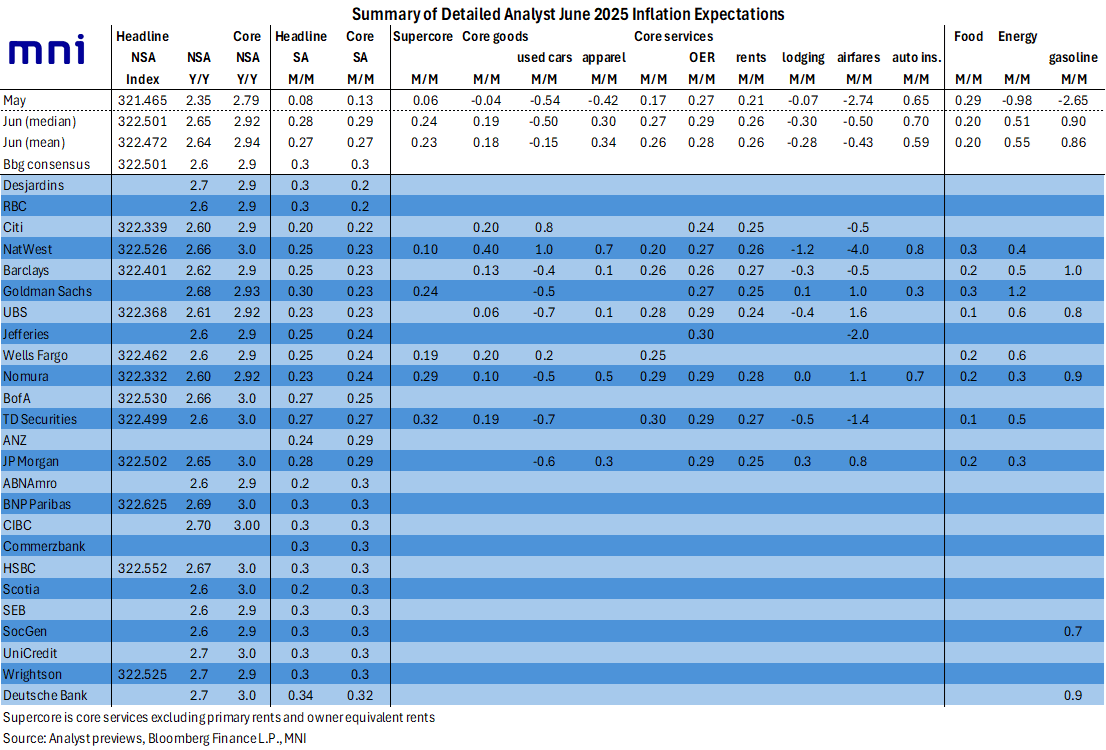

- Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June on a rounded basis, but with sizeable risk of undershooting at 0.2% (MNI median unrounded estimate at 0.24% M/M /average 0.25%).

- This would mark an acceleration from 0.13% M/M in May, with core services ticking up and core goods more than reversing May’s unexpected M/M deflation. Headline CPI meanwhile is seen at 0.3% M/M or 0.25% M/M unrounded after 0.08% in May, amid a bounce in gasoline-driven energy prices.

- It’s possible that June’s report will only be starting to show the delayed impact from the April reciprocal tariffs with the largest impact perhaps only to be seen in July. There appears a rough consensus of three months from tariff implementation to more notable consumer price increases.

- Goods will be in particular focus as tariffs are seen having an increasing influence on inflation as the summer unfolds. Categories to watch include apparel, communications/recreational goods, and furniture.

- In services, OER is seen steady with rent CPI picking up, while travel-related categories are seen remaining a drag. Supercore inflation was particularly subdued in May at 0.06% M/M and the estimates we’ve seen on average look for an acceleration to 0.23-0.24% M/M.

- It's unlikely that a downside inflation surprise would persuade the Federal Reserve to seriously consider cutting rates at its next decision on July 30, given the expected ongoing pickup in tariff-related prices.

- But a continued lack of evidence that tariffs are having an outsized effect on consumer prices would certainly help lay the groundwork for a resumption of easing in September.

- Headed into CPI (Tue) and PPI (Wed), the Fed’s preferred Core PCE gauge is seen at 0.25-0.26%.