SNB: MNI SNB Review - September 2025: All Neutral

FULL REPORT HERE (incl. a rough transcript of the post-announcement press conference Q&A)

Executive Summary:

- SNB held its policy rate at 0.0%, meeting market and analyst consensus

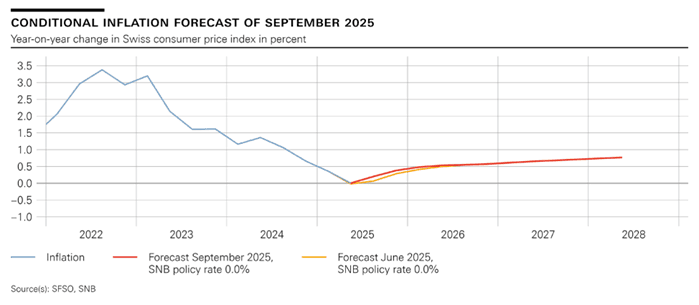

- The conditional inflation forecast and press statement remained materially unchanged. However, it remains unclear if Schlegel’s non-mention of side effects of potential negative rates in his opening remarks was an interesting development and could conceivably be argued to be a an implicit dovish or hawkish policy signal. We watch for any commentary on this in the new meeting summaries

- In the press Q&A, Schlegel refrained from giving forward guidance, drawing attention to the bank’s meeting-by-meeting approach, but did continue to mention the high bar for a further cut

- Market pricing marginally moved in a hawkish direction over the decision announcement and press Q&A, with now a mere 6bps of easing being priced through June 2026

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UK DMO UPDATE: Syndication Coupon Announcement

"The United Kingdom Debt Management Office (DMO) announces that the new conventional gilt, which will mature on 22 October 2035, will pay a coupon of 4 3/4% per annum, payable semi-annually. The new gilt will have the ISIN code GB00BTXS1K06 and the SEDOL code B-TXS-1K0; it will pay a long first coupon on 22 April 2026."

"The new gilt is planned for launch by syndication in the week commencing 1 September 2025, subject to demand and market conditions. Further details of this transaction will be announced in due course."

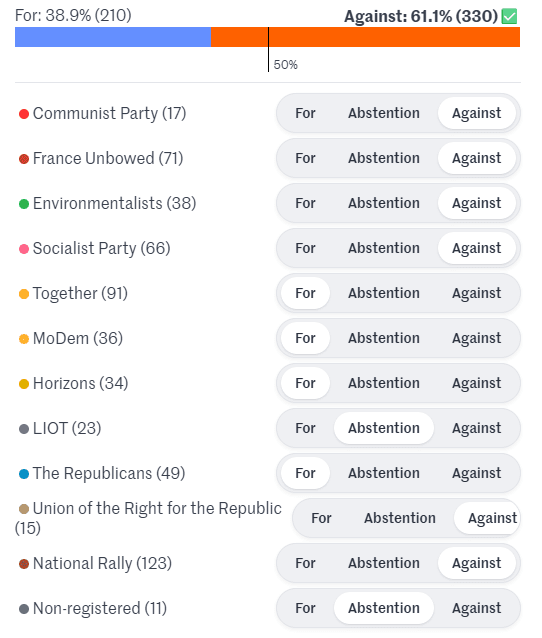

FRANCE: PM-"MPs Have 13 Days To Choose Between Chaos Or Responsibility"

Speaking at the French Democratic Confederation of Labour's summer university in Essonne, PM Francois Bayrou says that members of the National Assembly have "13 days to choose between chaos or responsibility", referring to the upcoming vote on spending cuts that the PM has said is effectively a confidence vote in his administration.

- That Bayrou has called the confidence vote, rather than the opposition calling a no-confidence vote, makes the gov'ts task that much harder. Art. 49 of the Constitution establishes that for a resolution of no confidence, an absolute majority of the National Assembly is needed to remove the gov't. This means abstentions are effectively votes to keep the gov't. However, in a confidence vote called by the gov't, there is not an 'absolute majority' requirement, meaning that abstentions work against the gov't if the votes against expressing confidence are going to exceed those in favour (as looks to be the case on 8 Sep).

- As such, the most likely outcome is the removal of the gov't. The parties of the far-left (Communists and France Unbowed) and far-right (National Rally and Union of the Right for the Republic) have already indicated that they will vote against expressing confidence in the gov't, as have the environmentalist Greens.

- Centre-left Socialist Party (PS) First Secretary Olivier Faure said to Le Monde that it would be "unimaginable" for his party to vote in favour of the Bayrou gov't, and has said his deputies will vote against. The PS has left the door open, saying if the gov't "revises its copy" on spending cuts, then its stance may change. However, this appears unlikely at present as the PS and Greens have talked up the idea of them forming a minority gov't post-Bayrou.

Chart 1. Prospective Confidence Vote in National Assembly

Source: Le Monde, MNI

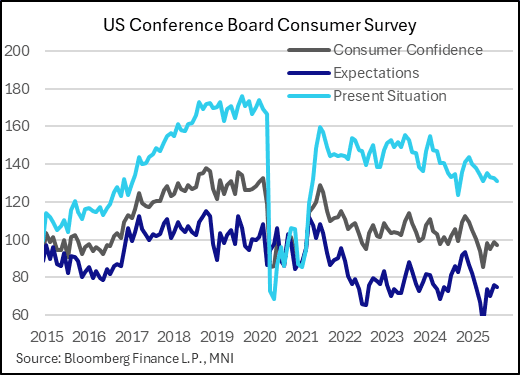

US DATA: Continued Weak Consumer Sentiment As Inflation Concerns Linger

The Conference Board's survey of consumer confidence showed slightly better than expected sentiment in August, but actually dimmed slightly vs an upwardly-revised July. While "soft" indicators of consumer activity haven't been particularly reliable in gauging actual underlying activity in recent years, by the same token there is no evidence here of an imminent resurgence in consumption.

- The headline consumer confidence composite index of 97.4 was better than the 96.5 expected but meant a decline from an upwardly revised 98.7 in July (97.2 prev est). Similarly, expectations (74.8 vs 76.0 prior) and present situation (131.2 vs 132.8 prior) saw slight relapses in August after improvements both outright and upwardly revised in July.

- The present situation print was a 4-month worst, with evidence of a deterioration in the labor market (as noted elsewhere) helping subdue sentiment. Assessments of families' current and expected financial situations were slightly stronger in August vs July, but outlooks for income prospects were less positive and there was a tickup in expectations of the US facing a recession in the next 12 months.

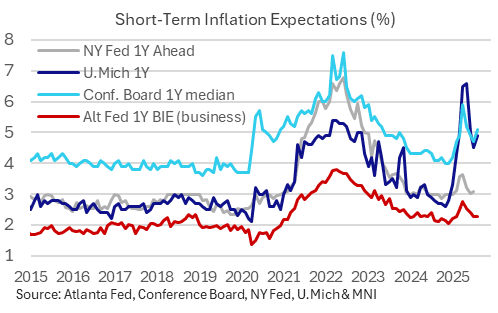

- It also came alongside a reacceleration in inflation expectations: at 6.2%, the average 12-month ahead expectation is a 3-month high (5.7% prior), with median expectations back above 5.0% (5.1%, 4.7% prior) for the first time in 3 months. The report noted “Consumers’ write-in responses showed that references to tariffs increased somewhat and continued to be associated with concerns about higher prices. Meanwhile, references to high prices and inflation, including food and groceries, rose again in August."

- We note that the UMichigan August survey also saw a slight rebound in 1-year inflation expectations.

- Instead of sharp improvement after seeming relief over policy uncertainty including tariff "deals" made through early August and the passage of the administration's signature fiscal bill in early July (survey cut-off date was Aug 20), the main aggregates appear to be settling into subdued ranges. Indeed as the report notes, the expectations gauge remained below the 80 mark that "typically signals a recession ahead" (it's been <80 for 7 consecutive months now).