CZECHIA: MNI Publishes Election Preview

Oct-02 10:31

Download Full Report Here

MNI's Political Risk team has published its latest Election Preview ahead of Czechia's legislative election on 3-4 October, with Prime Minister Petr Fiala’s centre-right governing coalition facing a major challenge amid a rise in support for nationalist and populist parties. In this preview, we offer a background briefing on the state of play in Czech politics, explanations on the electoral system for the Chamber of Deputies and the main parties and coalitions contesting the vote, election scenario analysis with assigned probabilities, analyst views, and a chart pack of opinion polling and betting market odds.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: Lithuania 10/20-year dual-tranche mandate

Sep-02 10:31

- "The Republic of Lithuania has mandated Erste Group, HSBC and Societe Generale as Joint Lead Managers and Luminor Bank as Co-Manager for a potential EUR-denominated Regulation S dual-tranche transaction, consisting of a long 10-year maturity and a 20-year maturity to be launched in the near future, subject to market conditions." From market source

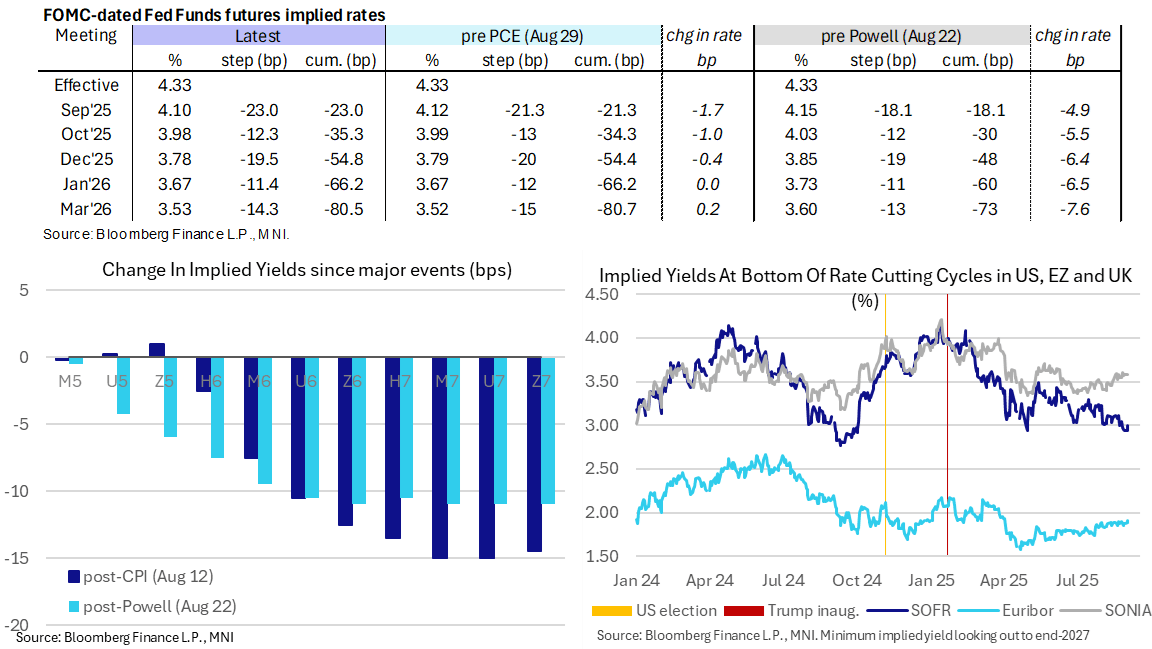

STIR: September Fed Cut Seen Mostly Locked In, ISM Mfg Ahead

Sep-02 10:26

- Fed Funds implied rates for near-term meetings are mixed relative to Friday’s levels post-Labor Day, with slightly higher odds of cut later this month but modestly more hawkish further out.

- Strong increases in WTI prices are having relatively little impact on front rates.

- Cumulative cuts from 4.33% effective: 23bp Sep, 35.5bp Oct, 55bp Dec, 66bp Jan and 80.5bp Mar.

- SOFR futures are up to 5 ticks lower in 2027 contracts vs Friday’s close, although with almost half of that coming yesterday in holiday-thinned trade.

- The SOFR implied terminal yield remains in the H7, at 2.995% (+5bp from Fri) having modestly lifted off last week’s recent lows of ~2.95%. It still points to more than 130bp of cuts ahead.

- Directionally, Fed terminal pricing remains at odds with the trend increase in BoE and ECB expectations over the past couple months.

- Today’s macro focus is on the ISM manufacturing survey before labor data comes into focus tomorrow ahead of Friday’s NFP report.

- Next scheduled Fedspeak comes from St Louis Fed’s Musalem (’25 voter, hawk) on the economy and policy tomorrow at 0900ET.

SONIA OPTIONS: Large Call Spread buyer

Sep-02 10:20

SFIU6 97.40/97.50cs, bought for 0.75 in 20k.