MNI INTERVIEW: RBNZ July Meeting Live - Conway

The Reserve Bank of New Zealand’s July 8 Monetary Policy Committee meeting is “live,” but a weak economy and elevated spare capacity will limit how far the Official Cash Rate can rise from 2.25% without severely damaging activity, Chief Economist Paul Conway told MNI.

“July is live, we just wanted a bit more evidence on how this [Iran conflict] is affecting the New Zealand economy, and also on the shock itself,” Conway said, following the four-three vote this week to hold the OCR at 2.25%. (See MNI RBNZ WATCH: Gov Breman Says Hike Incoming After Hold Vote) “In six weeks, which is a long time in economics these days, we’ll understand a bit more about the duration, the persistence in the shock and the magnitude, and we’ll have a better idea of what it’s doing to global oil markets.”

Conway said the MPC struggled to balance risks to the economy while assessing the impact of the Iran conflict and elevated oil prices on second-round inflation pressures. “For the three of us who didn’t want to hike, it was early days, and the shock in terms of how it’s going to percolate through the New Zealand economy,” he said. “We haven’t seen strong evidence of those second-round price effects.”

Governor Anna Breman, who like Conway and the other internal Committee member favoured a hold, cast an additional deciding vote on the MPC, which is currently only six strong pending the appointment of a deputy governor.

Core inflation has eased slightly since April, while longer-term inflation expectations generally dipped and wage growth remains contained, Conway continued, noting that some indicators suggest economic growth weakened more than expected. “The economy was recovering in Q4 and Q1 of this year, but indications are that growth is pretty weak,” he added.

While the Bank will not receive Q2 CPI data until after the July meeting, Conway said policymakers would review monthly selected price indices and business survey data to gauge the impact on prices.

OCR CEILING

How high the OCR ultimately rises will depend on the balance between pricing behaviour and weak demand in determining medium-term inflation pressures, he said.

“There’s a limit to what the economy can absorb,” Conway said, noting that one of the Bank's secondary objectives is to avoid unnecessary economic volatility. "If we push the OCR so high that the economy capitulates, then that’s a fail in terms of our remit.”

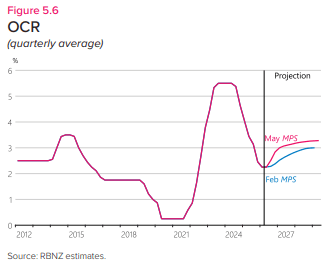

Markets see the OCR at 3% by December and at 3.32% by mid-2027, about 20 basis points higher Hidden PDF

Conway warned that excessively tight policy would risk driving inflation below the bottom of the target band as consumers and businesses lose the ability to absorb higher prices. “We’ve got two large opposing forces operating on medium-term inflation, and the scope for those to be different from what we’re currently viewing is quite large,” he said, referencing alternative scenarios published in the Monetary Policy Statement.

Hiking too early would have risked derailing recovery, while moving too late could allow near-term cost pressures to become embedded in medium-term inflation expectations, Conway said. He also noted that financial conditions have tightened significantly since February, even without a change in the OCR, as the Bank’s projected rate track pushed wholesale interest rates and mortgage rates higher.

NZD-AUD PAIR

The New Zealand dollar has weakened against its Australian counterpart since the beginning of the Middle East conflict, which Conway said reflected the neighbouring countries’ fundamentally different economic positions. (See MNI INTERVIEW: Aussie-NZ Spread To Widen, RBNZ Less Hawkish)

“The interest-rate differential is one reason why the Kiwi dollar is where it is vis-à-vis the Australian dollar,” he said, adding that the lower exchange rate would contribute to a temporary inflation spike this year while also supporting exporters by making New Zealand goods cheaper abroad.

However, the floating exchange rate continues to act as an effective economic shock absorber, and the interest-rate differential across the Tasman should normalise over time. “It’s not a surprise to us, it’s not a source of volatility for us. It’s doing what we would expect it to do," Conway concluded.