MNI INTERVIEW: RBA Strategy Risks Failure - Ex Chief Economist

The Reserve Bank of Australia is likely to fail in its attempt to curb inflation while preserving labour market gains and without generating a negative output gap, doing further damage to its credibility, the RBA’s former head of research told MNI, warning that another rate hike is likely in May.

John Simon, who led the Bank’s economic research department from 2014 to 2024, said Governor Michele Bullock’s assertion that inflation can return to target without a negative output gap — provided expectations remain anchored — rests on increasingly fragile foundations. Pointing to her remarks following Tuesday’s hike that expectations will remain anchored only if “people think we will do what we need to do to get inflation down,” he noted that two- to three-year inflation expectations have continued to drift higher and added that the Bank is effectively attempting to “have it both ways.” (See MNI RBA WATCH: Timing Drove Split Vote, Not Direction-Bullock)

“It’s like 'we assume we’re going to remain credible, and that gives us essentially the freedom not to act,'” Simon said. “They want to use credibility built up in the past to move interest rates less than otherwise, but that undermines credibility in a structural sense.”

If credibility were fully intact, he argued, policy tightening would indeed be less necessary. “If you have perfectly anchored, credible belief in the central bank, then you don’t need to do anything — people will adjust their behaviour themselves. But that’s not how expectations are formed. People look at what’s happening now.”

Simon has long called for a more hawkish RBA and higher rates. (See MNI INTERVIEW: RBA Needs More Hawkish Tone - Fmr Research Boss)

INFLATION EXPECTATIONS

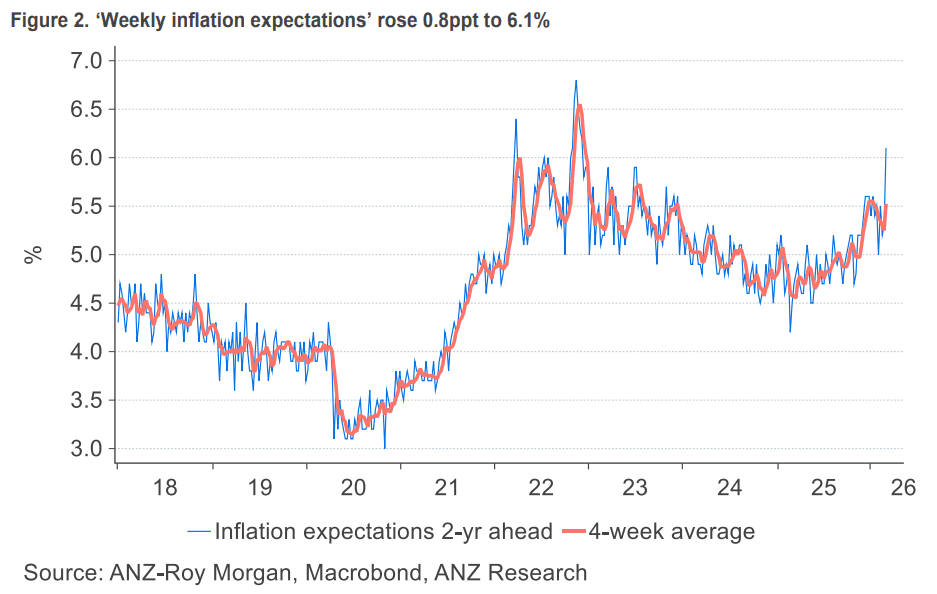

He warned that elevated oil prices could reinforce already rising medium-term inflation expectations, even if such shocks are typically transitory. “You need a lot to go right for them to be able to look through an oil price shock,” he said, noting inflation is already trending towards 5%.

While Bullock emphasised domestic inflation pressures as the primary driver of the latest rate hike, downplaying the impact of the Iran conflict on global energy prices, Simon said sustained energy costs would still feed into expectations. (See chart)

Simon was also critical of the Bank’s stated objective of preserving labour market gains, describing the concept as incoherent. “If they still believe it, they’ve got a problem with delivery because it relies on perfectly-anchored expectations, which I don’t think we have,” he said. “But if it’s just rhetoric, that’s arguably worse.”

He argued that the RBA cannot sustainably influence structural labour market outcomes such as the non-accelerating inflation rate of unemployment (NAIRU). “The best it can do is keep the economy close to its sustainable level. It can’t preserve labour market gains,” he said, adding previous arguments that tight policy could permanently lower the NAIRU reflect “confused thinking.”

The Bank’s apparent aim of achieving a “smooth landing” without a negative output gap or rise in unemployment above the NAIRU is highly unorthodox, Simon said. “You might aim to avoid a recession while still generating a negative output gap — that’s consistent with how most economists think about the economy. But to suggest you can have no negative output gap at all is a step beyond that.”

MAY HIKE

Simon noted another rate increase at the May meeting — where markets see about a 69% chance of a move higher — is likely, though the path beyond will depend on global developments.

While downside risks from the global environment — including geopolitical tensions — could weigh on growth, Simon said domestic inflation pressures alone justify further tightening. He added that upcoming inflation data, particularly headline figures incorporating higher oil prices, are likely to be “ugly,” complicating the policy outlook, while markets should also focus strongly on two- and three-year inflation expectations.