MNI Fed Preview-July 2025: Analyst Outlook

Jul-28 18:43By: Tim Cooper

US

Download Full Report Here

This update of our July 25 Fed preview includes analyst expectations.

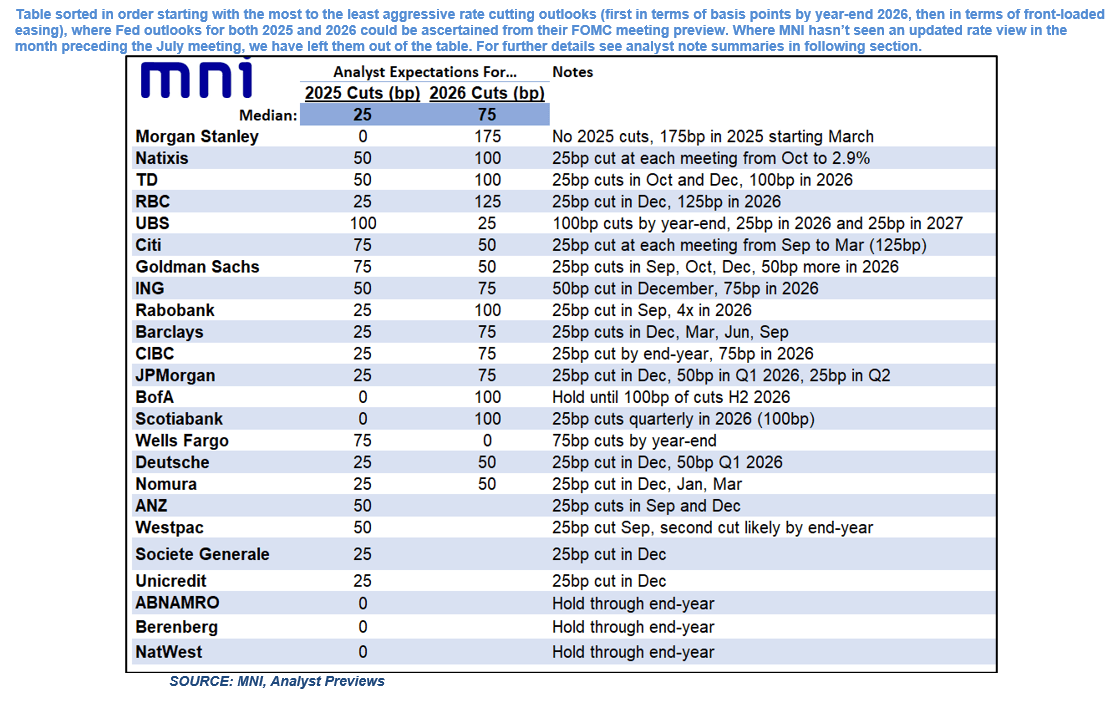

Jul 2025 FOMC Analyst Views: See You In The Fall

No analysts expect the Fed to cut rates or adjust balance sheet policy at the July FOMC, per the 32 meeting previews seen by MNI. This is unchanged from the June meeting at which even at that point, no July cut was seen.

- It’s virtually unanimous that there will be two dissents in favor of a cut at this meeting, with Gov Waller widely expected to do so and Gov Bowman also likely (among analysts who expressed an opinion on this).

- Statement changes are expected to be limited, with perhaps some downgrading of the characterization of growth in the first paragraph, and many seeing the language on uncertainty changing (“has diminished but remains elevated” to remove “has diminished but”).

- Powell’s press conference is expected to see extensive questioning about political interference in the Fed, and his own future as Chair.

- In terms of actual policy, Powell is seen conveying a fairly neutral stance on future cuts, with reiteration of the June Dot Plot (50bp of cuts by year-end) seen as a potential dovish outcome.

- Future action: The median expectation for 2025 rate cuts is 25bp, with a range of zero (including BofA, NatWest, and Scotiabank) further easing, to 100bp (UBS).

- Expectations are very much mixed for the timing of the resumption of easing, mostly split between September and December, but a few seeing October and some only next year.

- At least one sees a 50bp cut at a single meeting by year-end (Natixis, December).

- For analysts that have provided both a 2025 and 2026 rate outlook, the range of expectations for total cuts by end-2026 is 75-175bp with a median 112.5bp. Though this doesn’t include a few analysts who see no cuts in 2025 - implying that they see the Fed easing cycle already at an end.

- That said, the most total cuts are seen by Morgan Stanley (175bp, entirely in 2026), followed by Natixis, RBC, and TD (150bp each through end-2026).

Trending Top

May-22 16:54