EUROPEAN INFLATION: MNI Eurozone Inflation Preview – August 2025

Full report here: LINK

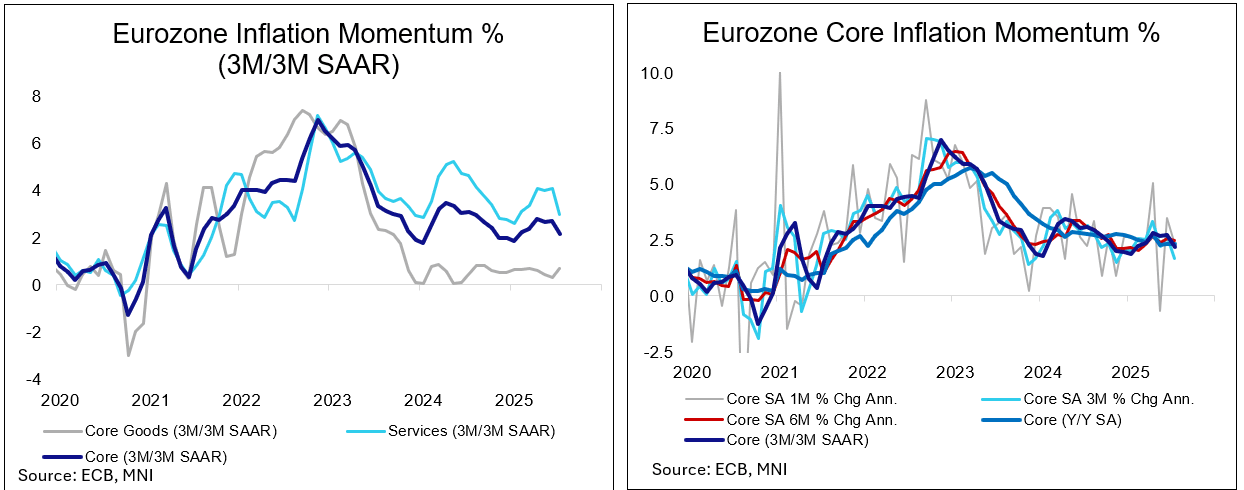

Clear Downside Surprise Needed For Dovish Tilt

- The August Eurozone inflation round is split across two weeks, with the main prints of Spain, France, Italy, and Germany all scheduled for this Friday before the Netherlands and the Eurozone-wide figures follow next Tuesday.

- Analysts are looking for headline to pick up marginally to 2.1% Y/Y, while core inflation is expected to slow to 2.2%.

- Across categories, the main driver this time will be energy inflation base effects, putting upside pressure on headline. Analysts see the category around -1.6% Y/Y in August after -2.4% in July.

- Services inflation is expected to continue its downtrend seen this year, with consensus standing around 3.0-3.1% after 3.2% in July.

- Core goods meanwhile are seen to give away some of their July firmness, at 0.7% Y/Y, while views on food/alcohol/tobacco inflation are more mixed this time where consensus might be for a roughly unchanged print at 3.2%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS/SUPPLY: Fairly Narrow Range Of Expected Borrowing Estimates (2/2)

Our estimates made last week for borrowing requirements ($950-1,000B in Jul-Sep aka FYQ3, $600B for Oct-Dec aka FY Q4) appear to chime with several estimates we've seen since then (note it's almost unanimous that a $850B end-September cash target will be included in today's estimates). These include:

- Deutsche: Q3 borrowing requirement $960B, Q4 $680B

- Jeffries: Q3 borrowing requirement $957B, Q4 $575B

- Wrightson ICAP: Q3 borrowing requirement $980B, Q4 $650B

Estimates that we included in our refunding preview:

- CIBC: Marketable borrowing requirement of $942B in Jul-Sep on $471B financing need, Oct-Dec $726B marketable borrowing on $649B financing need

- JPMorgan: $1,087B and $572B borrowing requirements this quarter/next quarter respectively

- TD: $1,051B Jul-Sep quarter, $534B Oct-Dec. Tariffs could mean cash flows more positive.

- Wells Fargo: Marketable borrowing in Q3 $946B ($393B cash balance, $413B budget deficit); Q4 $592B

EUR: Sharpest One-Day Downmove Since Trump's Election Results

Persistent EUR/USD sales are pressing the rate lower still well after the London close, with EUR/USD now south of 1.1600 for the first time since mid-July's show below the handle (which proved to be short-lived, and may have cleared out S/T EUR positioning). The pair's ~180 pip losses are the largest one-day decline since November last year - the session capturing Trump's election results.

- The scale of today's reversal signals the markets' surprise at the terms of the EU-US trade deal. The 15% export tariff, minimal industry carve-outs and reduction of many tariffs to zero for EU-bound US products have opened the deal up for criticism - particularly in France. This leaves risks to growth larger than the ECB had anticipated, even as the worst case scenario has been avoided.

- As a result of today's price action, the 14-day RSI has slipped hard, below 50 for the lowest reading of the month and third-lowest of Trump's Presidential term so far. While medium-term trend indicators continue to highlight a dominant uptrend, today's price action shows the potential for near-term corrections lower.

- The pair has revisited the 50-dma - a level which has helped contain weakness on several occasions this year - and a containment of losses above 1.1565 will mean the M/T uptrend is still intact. Conversely, a break below this mark would signal a stronger reversal - making 1.1431 the initial downside target.

PIPELINE: Corporate Bond Roundup: $12B Mexico 5Y Launched

- Date $MM Issuer (Priced *, Launch #)

- 07/28 $12B #Mexico 5Y +170 (last time Mexico issued: $4.5B on June 23: $2.5B 7Y +175, $2B +12Y +230)

- 07/28 $2B #Deutsche Bank $1.7B 6NC5 +98, $300M 6NC5 SOFR

- 07/28 $1.5B Community Health Systems 8.5NC3 9.5%a

- 07/28 $Benchmark RBC 4NC3 +62.5, 4NC3 SOFR, 6NC5 +73, 6NC5 SOFR

- 07/28 $600M #Ally Financial 8NC7 +137

- 07/28 $Benchmark M&T Bank 10NC5 +145

- 07/28 $650M EW Scripps 5NC2 investor calls (expected to launch 7/29)