MNI EUROPEAN OPEN: US-China Look To Fulfil Geneva Agreement

EXECUTIVE SUMMARY

- US, CHINA REACH DEAL TO EASE EXPORT CURBS, KEEP TARIFF TRUCE ALIVE - RTRS

- BESSENT EMERGES AS A CONTENDER TO SUCCEED FED’S POWELL - BBG

- SURPLUS, DEFICIT NATIONS NEED TO ADJUST POLICIES - LAGARDE - MNI

- JAPAN MAY CGPI RISES 3.2% Y/Y, IMPORT PRICE DROPS - MNI BRIEF

- JAPAN'S MOF SAYS SPECULATION OF JULY JGB BUYBACK UNREALISTIC - BBG

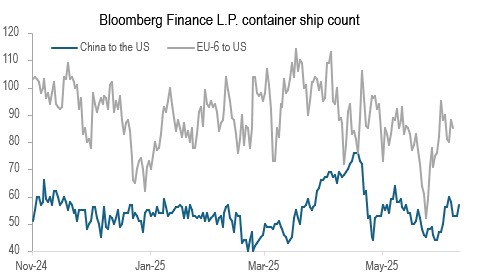

Fig 1: Shipping To US Normalising But Frontloading May Reduce H2

Source: Bloomberg Finance L.P./MNI

UK

FISCAL (BBC): “Rachel Reeves is preparing to unveil her highly anticipated spending review, setting out how much money the NHS, schools, police and other public services will get over the next few years. The chancellor will emphasise plans to "invest in Britain's renewal" by spending an extra £113bn on infrastructure, such as energy and transport projects in her speech on Wednesday.”

EU

EUR (BBG): “European Central Bank Governing Council member Yannis Stournaras said the US’s unpredictable behavior on tariffs is undermining the dollar’s status as the global reserve currency and is an opportunity for the euro, according to an interview in Handelsblatt.”

TRADE (MNI): Surplus and deficit nations need to act to defuse global trade tensions, European Central Bank President Christine Lagarde said in a speech in Beijing on Wednesday. “We must pursue cooperative solutions – even in the face of geopolitical differences. And that means both surplus and deficit countries must take responsibility and play their part,” Lagarde said at the People's Bank of China in Beijing.

SWEDEN (MNI INTERVIEW): Swedish debt market liquidity has improved and recent market turbulence and curve steepening is not triggering any shift in issuance strategy, Klas Granlund, Head of Debt Management at Riksgalden, the Swedish Debt Management Office, told MNI.

POLAND (POLITICO): “Polish Prime Minister Donald Tusk is expected to comfortably survive a confidence vote on Wednesday but the result will do little to assuage the challenges posed by the victory of conservative nationalist Karol Nawrocki in the June 1 presidential election.”

NATO (POLITICO): “Lithuania “will never give up” on the idea that Ukraine has to be in NATO, Defense Minister Dovilė Šakalienė told POLITICO.”

FRANCE (POLITICO): “French authorities are seriously considering restricting public access to some of the world's most popular social media sites to prevent children from accessing pornography and to stop them being radicalized.”

US

US/CHINA (RTRS): “U.S. and Chinese officials said on Tuesday they had agreed on a framework to put their trade truce back on track and remove China's export restrictions on rare earths while offering little sign of a durable resolution to longstanding trade differences.”

FED (BBG): “A growing chorus of advisers inside and outside the Trump administration are pushing another name to serve as the next chair of the Federal Reserve: Treasury Secretary Scott Bessent.”

PROTESTS (RTRS): “Los Angeles Mayor Karen Bass declared a limited curfew starting at 8:00 p.m. PT (0300 GMT) Tuesday night, after nearly 200 arrests on Tuesday. The curfew will cover one square mile (2.5 square km) of downtown Los Angeles and last several days.”

OTHER

GLOBAL (MNI): The World Bank slashed this year's global growth forecast almost half a percentage point to 2.3% on the U.S.-led trade war and said economic expansion over the next two years is set to be the weakest since the 1960s.

JAPAN (MNI BRIEF): Japan’s corporate goods prices slowed in May but remained higher than Bank of Japan projections, supported by persistent cost pressures in labour, logistics and key commodities, data released by the BOJ on Wednesday showed.

JAPAN (BBG): "Japan has no plans to buyback government bonds in July and speculation of this is unrealistic, the finance ministry said. A Ministry of Finance official said in an email the market’s speculation of Japanese government debt buybacks from July is unrealistic and not envisioned."

US/MEXICO (BBG): “The US and Mexico are closing in on a deal that would remove President Donald Trump’s 50% tariffs on steel imports up to a certain volume, according to people familiar with the matter, a revamp of a similar deal between the trade partners during his first term. “

CHINA

US/CHINA (CHINA NEWS SERVICE): “China and the U.S. have reached a framework in principle for implementing the consensus agreed at the Geneva talks and June 5 heads of state call, said Li Chenggang, international trade negotiator and vice minister of commerce. Li said communication in London was professional, rational, in-depth and candid.”

TRADE-INS (YICAI): “China’s old-for-new subsidy policy has been suspended or limited in some areas such as Chongqing and Guangzhou, in the lead-up to the June 18 mid-year shopping festival, according to Yicai, which cited information obtained from multiple sources.”

CONSUMPTION (YICAI): “China should direct more investment towards consumption to promote corporate innovation, industrial upgrading and release consumer spending, according to Xu Mingzhi, assistant economics professor at Peking University. “

MNI: PBOC Net Drains CNY50.9 Bln via OMO Wednesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY164 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY50.9 billion after offsetting the maturity of CNY214.9 reverse repo today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4886% at 09:36 am local time from the close of 1.5063% on Tuesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 49 on Tuesday, compared with the close of 46 on Monday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.1815 Weds; +0.96% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1815 on Wednesday, compared with 7.1840 set on Tuesday. The fixing was estimated at 7.1815 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND APRIL NET MIGRATION ESTIMATE +1,810; MAR. +1950

JAPAN MAY PRODUCER PRICES -0.2% M/M; EST. +0.2%; APR. +0.3%

JAPAN MAY PRODUCER PRICES +3.2% Y/Y; EST. +3.5%; APR. +4.1%

SOUTH KOREA MAY ADJUSTED JOBLESS RATE 2.7%; EST. 2.7%; APR. 2.7%

SOUTH KOREA MAY EMPLOYED +245K Y/Y; APR. +194K Y/Y

SOUTH KOREA JUNE 1-10 EXPORTS +5.4% Y/Y; PRIOR -23.8%

SOUTH KOREA JUNE 1-10 IMPORTS RISE 11.5% Y/Y; PRIOR -15.9%

SOUTH KOREA MAY HOUSEHOLD LENDING KRW1,155.3T; APR. KRW1,150.1T

MARKETS

US TSYS: Asia Wrap - A Quiet Session, Focus On CPI

The TYU5 range has been 110-03+ to 110-08+ during the Asia-Pacific session. It last changed hands at 110-07+, up 0-01 from the previous close.

- The US 2-year yield is dealing around 4.012%, down 0.01 from its close.

- The US 10-year yield is trading around 4.466%, unchanged from its close.

- Bloomberg - “Treasury 10-year contracts are heading lower as today’s debt auction is unlikely to offer enough juice for it to run smoothly given there is a 30-year sale to follow and CPI data due. Indeed, investors appear to be nervous about the outcome of the longer duration offering which by default could make it more difficult for the ten-year which needs to be first.”

- Bloomberg - “Morgan Stanley strategists expect a surprise decrease in inflation data and declining oil prices to reduce the bond market's inflation expectations over the next two years.”

- The 10-year yield held its support around the 4.35% area last week. While this level holds focus will remain on potentially extending higher, CPI tonight will dictate direction.

- Data/Events: CPI, Federal Budget Balance

JGBS: MoF: Buyback Unrealistic, RTRS Poll: BoJ On Hold This Year

JGB futures are stronger and near session highs, +15 compared to settlement levels

- BBG notes: " Buying back of super-long government bonds from July is unrealistic and not envisioned, an official from Japan's Ministry of Finance said in an email to Bloomberg News."

- Reuters Poll Summary – Bank of Japan Outlook: 52% of economists expect the BOJ to hold its key interest rate at 0.50% through year-end, up from 48% in May; 55% expect the BOJ to slow bond purchases starting April 2026, while 45% see no change;78% forecast a rate hike to at least 0.75% by end-Q1 2026; and 75% expect a reduction in super-long JGB issuance, while 25% see it unchanged.

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's CPI data.

- Earlier US-China trade talk headlines from London had little impact on the markets.

- Cash JGBs are slightly mixed across benchmarks, with a mild steepening bias. The benchmark 10-year yield is 1.2bps lower at 1.466%.

- Swap rates are flat to 2bps lower. Swap spreads are tighter.

- Tomorrow, the local calendar will see BSI Industry Survey, Weekly International Investment Flows and Tokyo Avg Office Vacancies data alongside an auction for Enhanced-Liquidity of 15.5 - 39-year JGBs.

AUSSIE BONDS: Cheaper Ahead of US CPI, AU-US 10Y Diff Near Bottom Of Range

ACGBs (YM -5.0 & XM -2.0) are weaker after trading in narrow ranges on a local-data-light session.

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's CPI data. Analyst unrounded estimates see core CPI inflation accelerating mildly to 0.27% M/M (median, 0.28% average) in May after 0.24% M/M in April. (See link)

- Focus has also been on US-China trade talks, with headlines from London crossing earlier. The market reaction has been fairly muted, with the main outcome being agreement to move forward with what was agreed at the Geneva talks in May (although both US and Chinese leaders need to sign off on implementation).

- Cash ACGBs are 2-4bps cheaper with a flatter curve and the AU-US 10-year yield differential at -20bps.

- The bills strip has cheapened, with pricing -2 to -3.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in July is given a 79% probability, with a cumulative 72bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty apart from a speech from RBA Jacobs, Head of Domestic Markets Department – Australia’s Bond Market in a Volatile World – at the Australian Government Fixed Income Forum, Tokyo.

BONDS: NZGBS: Closed With A Twist-Flattener Ahead Of US CPI

NZGBs closed showing a twist-flattener, with yields 2bps higher to 1bp lower.

- Bloomberg - "New Zealand's annual net immigration fell to 21,317 in April, a two-and-a-half-year low, which could slow the country's economic recovery and lead to more interest-rate cuts."

- "The decline in net immigration is partly driven by New Zealand citizens leaving the country to seek better incomes, which could dampen demand and prompt the Reserve Bank to provide policy stimulus."

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's CPI data.

- Focus has also been firmly on US-China trade talks, with headlines from London crossing earlier. The market reaction has been fairly muted, with the main outcome being agreement to move forward with what was agreed at the Geneva talks in May (although both US and Chinese leaders need to sign off on implementation).

- Swap rates closed showing a flatter curve, with yields 2bps higher to 2bps lower.

- RBNZ dated OIS pricing closed firmer across meetings. 4bps of easing is priced for July, with a cumulative 27bps by November 2025.

- Tomorrow, the local calendar will see Card Spending data, ahead of BusinessNZ Manufacturing PMI on Friday.

FOREX: Asia FX Wrap - Quiet Session Ahead Of US CPI

The BBDXY has had a range of 1209.44 - 1212.04 in the Asia-Pac session, it is currently trading around 1211.”With weaker data eroding the UK’s relative yield advantage and the Federal Reserve clinging to its higher-for-longer script, GBP/USD now faces a more challenging landscape. The pound has rallied nearly 8% year-to-date against the dollar, but the backdrop may be shifting”(BBG). PPG Macro on X: “UK (un)employment. HMRC PAYE employees total for May fell 109k. Even allowing for revisions, payrolled employment has fallen for 7 months in a row. 6-month average fall of 41.7k. The equivalent of nonfarm payrolls falling at over 200k a month.”

- EUR/USD - Asian range 1.1406 - 1.1439, Asia is currently trading 1.1415. EUR has drifted down during the Asian session in response to the move lower in US stocks. Dips should continue to find demand, first support around 1.1350 then the 1.1100/1200 area.

- GBP/USD - Asian range 1.3475 - 1.3510, Asia is currently dealing around 1.3485. The GBP looks to be failing in its attempt to gain any momentum above the pivotal 1.3500 weekly pivot. Poor data yesterday capped the move, support seen back towards 1.3400 and then 1.3200.

- USD/CNH - Asian range 7.1823 - 7.1897, the USD/CNY fix printed 7.1815. Asia is currently dealing around 7.1865. Sellers should be around on bounces while price holds below the 7.2500 area.

- Cross asset : SPX -0.29%, Gold $3340, US 10-Year 4.47%, BBDXY 1211, Crude oil $64.95

Data/Events : US CPI

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD/JPY Doing Work Around The 145.00 Interest

The Asia-Pac USD/JPY range has been 144.66 - 145.16, Asia is currently trading around 145.00. USD/JPY has had a muted session trading around some decent Option interest in the 145.00 area.

- Japan's May PPI was below market expectations, falling 0.2% m/m (against a +0.2% forecast). April's rise was revised to +0.3% (from 0.2%). In y/y terms, we printed 3.2%, against a 3.5% forecast (prior was 4.1%). In terms of the detail, manufacturing PPI was down 0.4%m/m. Weakness was evident in commodities, particularly petroleum, coal (-4.8%m/m). Iron ore and steel were also down in m/m terms. Import prices for commodities were down 1.1%m/m, continuing a negative trend, now off 10.3% in y/y terms.

- (Dow Jones) - “October may be the last chance for the Bank of Japan to raise interest rates, says Norinchukin Research Institute economist Takeshi Minami. Consumer inflation is expected to slow in the summer and slip below 2% after the start of 2026, he says.”

- Some large option interest around these levels has seen it do some work around 145.00.

- The market still seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase.

- With the failure to break below 142.00 last week, price is back in its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction. US CPI tonight will dictate price action. Expiries below show a lot of interest around the 145.00 area.

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($1.14bm). Upcoming Close Strikes : 143.00($1.28b June 12), 140.00($1.22b June 12), 145.00($4.54b June 16).

CFTC data shows Asset managers maintained their already extensive JPY longs, and leveraged funds try again to build their own longs.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

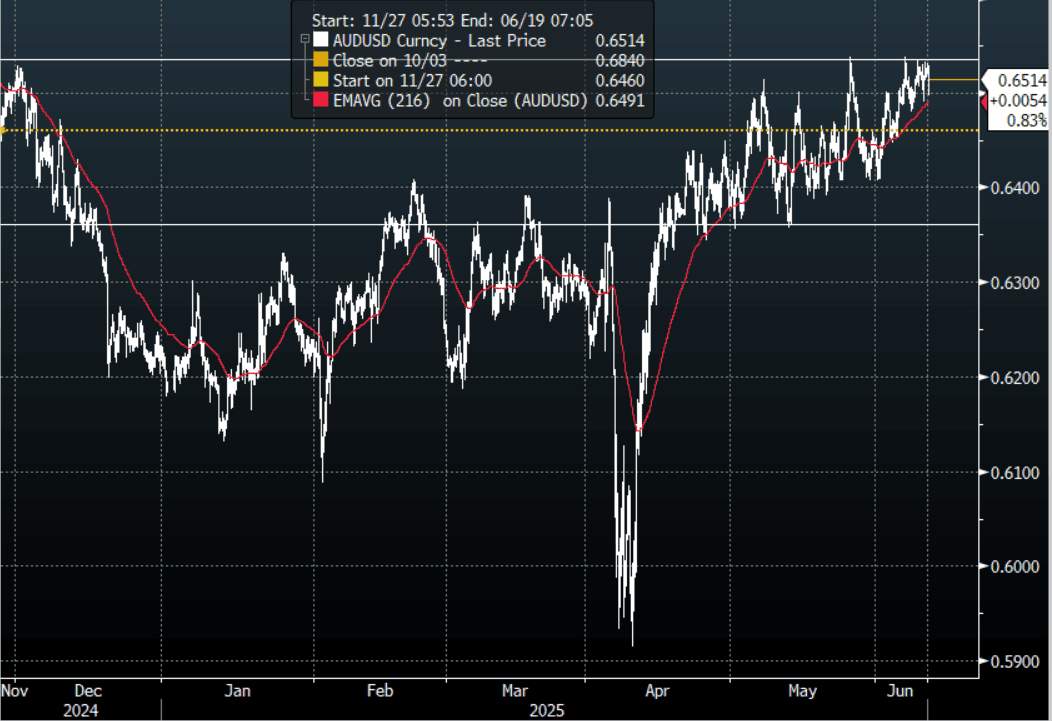

AUD: Asia Wrap - AUD/USD Drifts Lower Into US CPI

The AUD/USD has had a range of 0.6497 - 0.6532 in the Asia- Pac session, it is currently trading around 0.6515. The AUD has drifted lower for most of our session as US stocks fail to push on after positive headlines on the conclusion of the US-China talks. Another failure to get back above 0.6550, CPI tonight will determine if it gets tested again.

- AUS Bond Auction: ACGB Nov-32 Auction Goes Smoothly But With Less Demand: Today's auction reflected solid pricing for ACGBs, with the weighted average yield coming in 0.65bps below prevailing mid-yields, according to Yieldbroker.

- The AUD continues to see demand back towards the 0.6500 area, but the inability to break above 0.6550 on multiple occasions will have any bulls a little concerned.

- Price remains in the 0.6350 - 0.6550 range, a sustained break above 0.6550 is needed for the move higher to accelerate. Price looks like it wants to test the top end of the range, tonight's US CPI print will have a say in that.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6350 is needed to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6495(AUD400m), 0.6365(AUD550m). Upcoming Close Strikes : 0.6350(AUD 711m June 12), 0.6600(AUD643m June 12)

- CFTC Data shows Asset managers maintaining their shorts, the Leveraged community though continued to add to their shorts again.

AUD/JPY - Today's range 94.20 - 94.75, it is trading currently around 94.35. Price broke the multiple tops around the 94.00 area over NFP’s. It has since managed to hold these gains, while this continues focus will turn to the high towards 96.00. Support should now be back towards the 93.00/50 area.

Fig 1: AUD/USD spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

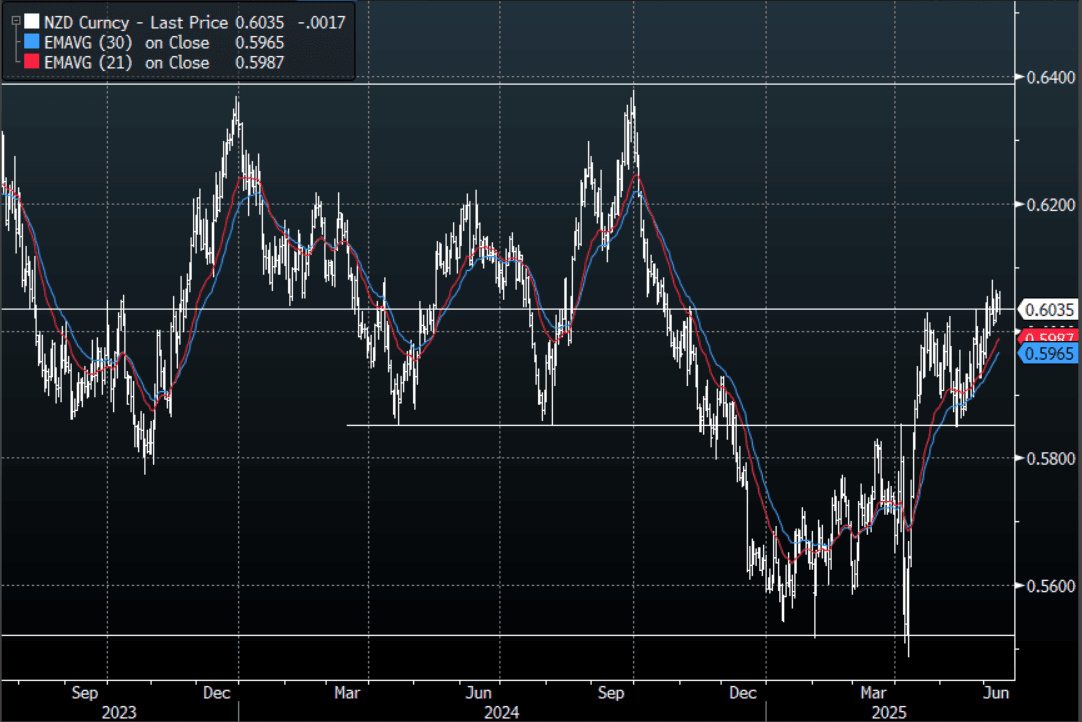

NZD: Asia Wrap - Drifts Lower, Holds Above 0.6000

The NZD/USD had a range of 0.6025 - 0.6062 in the Asia-Pac session, going into the London open trading around 0.6035. The NZD has drifted lower for most of our session as US stocks fail to push on after positive headlines on the conclusion of the US-China talks. The NZD has looked to be building for an extension higher, CPI tonight will determine if this can come to pass.

- Bloomberg - “New Zealand's annual net immigration fell to 21,317 in April, a two-and-a-half year low, which could slow the country's economic recovery and lead to more interest-rate cuts.”

- “The decline in net immigration is partly driven by New Zealand citizens leaving the country to seek better incomes, which could dampen demand and prompt the Reserve Bank to provide policy stimulus.”

- The NZD continues to find demand back towards the 0.6000 area as dips remain well supported, bulls will be hoping this holds to have another crack at extending higher.

- The support back towards 0.5850 has held very well, and while this continues to hold expect buyers to be around on dips. A clear break above 0.6050/0.6100 could provide the spark for the next leg higher. The market remains short and above here they could be forced to pare back.

- CFTC Data showed Asset managers maintaining their shorts, while the leverage actually added to their shorts last week.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6100(NZD353m), 0.6145(NZD348m). Upcoming Close Strikes : none

AUD/NZD range for the session has been 1.0769 - 1.0793, currently trading 1.0790. A top looks in place now just above 1.0900, the cross topped out on Monday towards the 1.0800/25 sell area, the first target looks to be around 1.0650.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Regional Gains Amid Trade War Hope

China's major bourses were among the regional leaders today as news filtered in on positive steps from the US China discussions. The KOSPI followed suit hitting highest since the end of 2021 led by chip makers hopeful of a trade resolution. Hong Kong listed China Rare Earth surged over 12% on the hope that trade tensions could ease.

- The Hang Seng led the way for the major Chinese bourses, erasing yesterday's losses to be up +0.95%. The CSI 300 followed suit rising +0.82%, the Shanghai Comp +0.54% and the Shenzhen Comp +0.72%.

- The KOSPI is in fast approaching the 3,000 mark at 2,898 and rose +0.94% today, following yesterday's gains of +0.56%

- The FTSE Malay KLCI is up +0.49% more than erasing yesterday's losses.

- The Jakarta Composite's gains of +1.65% yesterday were forgotten today as it fell -0.40%.

- The FTSE Straits Times fell -0.54% whilst the PSEi in the Philippines rose +0.45%

- The NIFTY 50 has eked out modest gains this morning of +0.20% and is on its sixth consecutive day of positive results.

OIL: Crude Little Changed As Waits For Upcoming US CPI Data

Oil prices are moderately lower during today’s APAC trading having already priced in some optimism on the outcome of US-China trade talks this week. Commerce Secretary Lutnick said that the Geneva Consensus was agreed to but it is now up to both presidents to agree to its implementation which could also allow further talks to occur. The focus had been on easing export controls.

- Oil prices fell slightly on Tuesday as the market became impatient waiting for a US-China announcement. They are slightly down again today ahead of US CPI data but off their intraday lows with WTI -0.1% to $64.93/bbl after a trough of $64.60, while Brent is -0.1% to $66.78/bbl following a fall to $66.47. The USD index is up 0.1%.

- The EU is putting together a new package of sanctions including a sharp reduction in the G7 price cap for Russia’s oil exports as its drone attacks on Ukrainian cities have escalated. There had been hope that a ceasefire may have enabled sanctions to be eased.

- Bloomberg reported that US oil inventories fell around 400k barrels last week, according to people familiar with the API data. Product stocks were higher with gasoline up 3mn and distillate 3.7mn. The official EIA data is out Wednesday including gasoline demand.

- Later US May CPI prints and is expected to show a 0.1pp pickup in both core and headline to 2.4% y/y and 2.9% y/y. It will be monitored for signs of any tariff impact. The US May federal budget is also released. ECB’s Lagarde, Lane, Cipollone and Buch appear today.

GOLD: Firmer, But Tracking Within Recent Ranges

Gold has ticked higher in the first part of Wednesday trade, last near $3341-42/oz, up around 0.50% versus end Tuesday levels in the US. This comes despite an uptick in the USD, with the BBDXY index around 0.1% stronger so far today. Focus has been firmly on US-China trade talks, with headlines from London crossing earlier. The market reaction has been fairly muted, with the main outcome being agreement to move forward with what was agreed at the Geneva talks in May (although both US and China leaders need to sign off on implementation).

- US equity futures have edged down, with the market perhaps looking for something more around broader tariff relief. This may be helping gold at the margins, although most regional equity markets in Asia Pac are firmer in Tuesday trade.

- For gold techs, the bullish theme remains intact with moving-average studies staying in a bull mode. Initial resistance is at $3403.5, 5 June high with the bull trigger at $3500.1. Initial support is at $3242.4, 50-day EMA.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 11/06/2025 | 0630/0730 | BOE Saporta Speech At Bank of Finland and SUERF Conference | ||

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0930/1130 | ECB Lane At 2025 Government Borrowers Forum | ||

| 11/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 11/06/2025 | 1130/1230 | Chancellor Reeves presents Spending Review to Parliament | ||

| 11/06/2025 | - | *** | Money Supply | |

| 11/06/2025 | - | *** | New Loans | |

| 11/06/2025 | - | *** | Social Financing | |

| 11/06/2025 | 1200/1400 | ECB Cipollone On Digital Payments Panel | ||

| 11/06/2025 | 1230/0830 | * | Building Permits | |

| 11/06/2025 | 1230/0830 | *** | CPI | |

| 11/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/06/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/06/2025 | 1800/1400 | ** | Treasury Budget | |

| 12/06/2025 | 0600/0700 | ** | UK Monthly GDP | |

| 12/06/2025 | 0600/0700 | ** | Trade Balance | |

| 12/06/2025 | 0600/0700 | ** | Index of Services | |

| 12/06/2025 | 0600/0700 | *** | Index of Production | |

| 12/06/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 12/06/2025 | 0900/1100 | ECB Schnabel Visits "House of the Euro" | ||

| 12/06/2025 | 1200/1400 | ECB de Guindos At Financial Integration Conference | ||

| 12/06/2025 | 1220/1420 | ECB Schnabel At Financial Integration Conference | ||

| 12/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 12/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 12/06/2025 | 1230/0830 | * | Household debt-to-income | |

| 12/06/2025 | 1230/0830 | *** | PPI |