MNI EUROPEAN OPEN: Tariff Threat For BRIC Aligned Countries

EXECUTIVE SUMMARY

- TRUMP THREATENS 10% TARIFF FOR ‘ANTI-AMERICAN’ BRICS ALIGNMENT - BBG

- TRUMP SAYS US NEARS TRADE DEALS AS TARIFF DEADLINE DELAYED - RTRS

- OIL TUMBLES AS OPEC+ HIKES AUGUST OUTPUT MORE THAN EXPECTED - RTRS

- JAPAN’S MAY NEGATIVE REAL WAGE WIDENS - MNI BRIEF

- MNI DISCUSSES CHINA'S PLANS FOR A NEW POLICY-BASED BOND - MNI

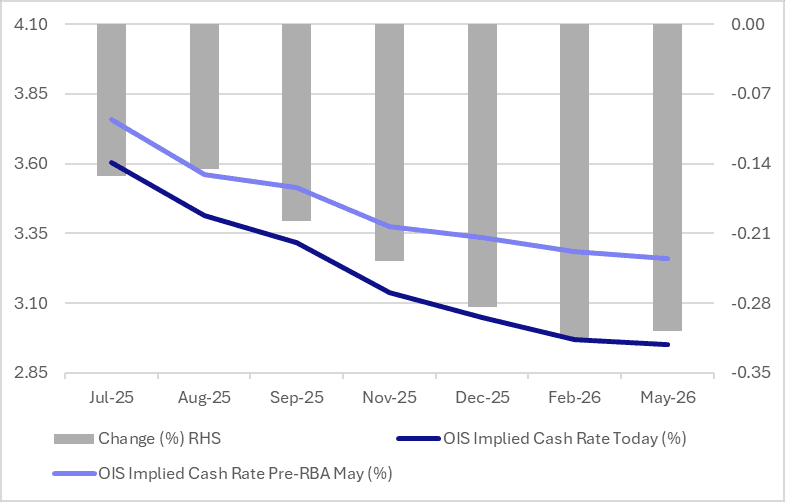

Fig 1: RBA-Dated OIS – Current Vs. Pre-RBA (May)

Source: Bloomberg Finance LP / MNI

UK

BOE (MNI BRIEF): Bank of England Monetary Policy Committee member Alan Taylor explained Friday why the market curve is too high with the equilibrium rate, or R star, well below where the market sees the policy rate settling.

FISCAL (BBG): “ UK Prime Minister Keir Starmer is caught between a political rebellion and a jittery bond market.”

FISCAL (TIMES/BBG): “ Chancellor of the Exchequer Rachel Reeves told cabinet ministers that tax increases in the Labour government’s fall budget are likely to be even more challenging than a £40 billion ($55 billion) package she put in place last year, the Times reported.”

EU

GERMANY (BBG): “A German pension fund has tapped a Chinese firm’s Hong Kong arm to help it invest in local stocks, in a rare move among global allocators that have been cautious about gaining exposure to the nation’s equities.”

CHINA/EU (MOFCOM): “China will take reciprocal measures against imported EU medical devices after the European Commission restricted Chinese companies and products from participating in its public procurement process, according to a notice from the Ministry of Commerce.”

US

TARIFFS (RTRS): “The United States is close to finalizing several trade pacts in coming days and will notify other countries of higher tariff rates by July 9, President Donald Trump said on Sunday, with the higher rates set to take effect on August 1.”

TARIFFS (BBG): “President Donald Trump said he would put an additional 10% tariff on any country aligning themselves with “the Anti-American policies of BRICS,” injecting further uncertainty into global trade as the US continues to negotiate levies with many trading partners.”

OTHER

JAPAN (MNI BRIEF): Japan’s inflation-adjusted real wages, a key gauge of household purchasing power, remained negative for the fifth straight month in May, falling 2.9% y/y following April's 2.0% decline, preliminary data from the Ministry of Health, Labour and Welfare showed Monday.

OIL (RTRS): “Oil prices slipped more than 1% on Monday after OPEC+ surprised markets by hiking output more than expected in August, raising concerns about oversupply.”

MIDDLE EAST (BBG): “ Multiple small vessels attacked a ship in the Red Sea near Yemen’s Al Hudaydah port, causing a fire on board and prompting the crew to abandon ship before the Israel army carried out airstrikes on Houthi-controlled ports in Yemen.”

SOUTH AFRICA (BBG): “South African President Cyril Ramaphosa faces a fresh crisis within his government after a police official accused one of his ministers of interference in an investigation into political assassinations.”

CHINA

INFRASTRUCTURE (MNI): MNI discusses China's plans for a new policy-based bond.

MACRO POLICY (ECONOMIC DAILY): “Authorities need to stabilise employment, enterprises, markets and expectations better, the Economic Daily commentary said, calling for quick policy support.”

NEW LOANS (SECURITIES DAILY): “New yuan loans are expected to reach about CNY2.1 trillion in June, with seasonal factors supporting growth from May’s CNY620 billion, Securities Daily reported, citing Wang Qing, analyst at Gold Credit Rating, who also highlighted last year's low base period comparison.”

MNI: PBOC Net Drains CNY225 Bln via OMO Monday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY106.5 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY225 billion after offsetting the maturity of CNY331.5 reverse repo today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.4286% at 09:39 am local time from the close of 1.4222% on Friday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 45 on Friday, the same as the close on Thursday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.1506 Mon; +1.48% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1506 on Monday, compared with 7.1535 set on Friday. The fixing was estimated at 7.1656 by Bloomberg survey today.

MNI: China CFETS Yuan Index Down 0.05% In Week of Jul 4

The CFETS Weekly RMB Index was 95.30 on Jul 4, down 0.05% compared with 95.35 as of Jun 30.

The gauge, which compares the yuan to a basket of currencies from China's 24 major trading partners, has decreased 6.08% this year, when compares with 101.47 on Dec. 31, 2024.

MARKET DATA

AUSTRALIA JUNE ANZ JOB ADS M/M 1.8%; PRIOR -0.6%

JAPAN MAY LABOR CASH EARNINGS Y/Y 1.0%; MEDIAN 2.4%; PRIOR 2.0%

JAPAN MAY REAL CASH EARNINGS Y/Y -2.9%; MEDIAN -1.7%; PRIOR -2.0%

JAPAN MAY CASH EARNINGS - SAME SAMPLE BASE Y/Y 2.3%; MEDIAN 2.8%; PRIOR 2.6%

JAPAN MAY SCHEDULED FULL TIME PAY - SAME BASE Y/Y 2.4%; MEDIAN 2.6%; PRIOR 2.5%

JAPAN MAY P LEADING INDEX 105.3; MEDIAN 105.2; PRIOR 104.23

MARKETS

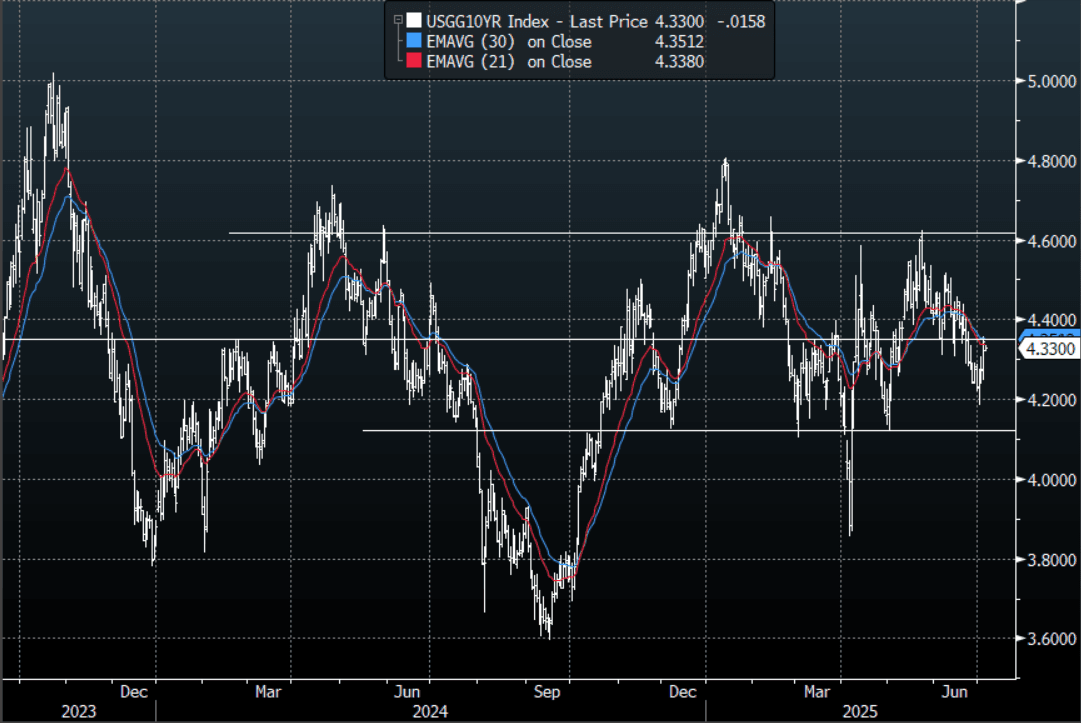

US TSYS: Asia Wrap - Yields Open Lower After Long Weekend

The TYU5 range has been 111-08+ to 111-12+ during the Asia-Pacific session. It last changed hands at 111-10+, up 0-03+ from the previous close.

- The US 2-year yield has moved lower trading around 3.855%, down 0.02 from its close.

- The US 10-year yield has edged lower trading around 4.33%, down 0.02 from its close.

- The 10-year yield saw a strong bounce in reaction to the better NFP print. This 4.35/40% area offers those who would like to express a long the opportunity to fade. A sustained close back above 4.40/4.45% area though would not be great for the bulls and would see more of the longs prepared back.

- US President Trump has posted via Truth Social that the US will start delivering letters outlining tariff levels to various countries starting 12pm Monday, US eastern time. Trade deals will also be announced at the same time.

- (Bloomberg) -- The Treasury’s willingness to fund more at the short-end of the yield curve will further compromise the Federal Reserve’s independence and increasingly leave monetary policy de facto in fiscal hands. The dollar will be a casualty, and the yield curve will steepen.

- Data/Events: Bond investors will be focusing on the Fed Minutes and the demand for 10 & 30-year maturities this week.

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Sharp Bear-Steepener, Fiscal Expansion Fears, 5Y Supply Tomorrow

JGB futures are little changed, -2 compared to settlement levels.

- Japan’s leading economic indicator was at 105.3 in May versus 104.2 in April.

- Bloomberg - "Japanese Prime Minister Shigeru Ishiba said the country is prepared for all possible tariff scenarios, speaking on Fuji TV's "Sunday News The Prime" program. Japan is ready to "stand firm" and defend its interests while anticipating every possible situation, says Ishiba."

- Cash US tsys are flat to 3bps richer in today's Asia-Pac session after resuming trading following the long weekend.

- (Bloomberg) The Treasury's willingness to fund more at the short end of the yield curve will further compromise the Federal Reserve's independence and increasingly leave monetary policy de facto in fiscal hands.

- Cash JGBs are -1bp richer to 8bps cheaper across benchmarks, with a steeper curve. The benchmark 5-year yield is 0.2bp higher at 0.973% ahead of tomorrow's supply.

- (Bloomberg) -- Ryutaro Kimura, senior fixed income strategist at AXA Investment Managers, said that fiscal expansion worries have weighed on Japanese government debt since the 30-year bond auction on July 3, and super-long-term bonds have sold off sharply.

- The swaps curve has bear-steepened, with rates flat to 5bps higher.

- Tomorrow, the local calendar will see Trade Balance and Bank Lending data alongside 5-year supply.

AUSSIE BONDS: Slightly Stronger, Subdued Session, RBA Policy Decision Tomorrow

ACGBs (YM +1.0 & XM +0.5) are slightly stronger ahead of tomorrow’s RBA Policy Decision.

- The RBA is widely expected to cut by 25bps. This is the sell-side consensus, albeit with a small number of economists expecting rates to be left on hold.

- May monthly CPI data should give the RBA confidence to cut. Headline inflation was close to the bottom end of the RBA's 2-3% target band, whilst the trimmed mean eased to 2.4%y/y. Services inflation is still running at a stronger pace, but we continue to move off recent highs for this sub-sector of inflation.

- RBA-dated OIS pricing is slightly softer across meetings. A 25bp rate cut this week is given a 94% probability, with a cumulative 79bps of easing priced by year-end. Notably, today's moves leave meetings pricing 15-32bps softer than levels before the May RBA Meeting.

- Cash US tsys are 1-3bps richer in today's Asia-Pac session after resuming trading following the long weekend.

- Cash ACGBs are 1bp richer with the AU-US 10-year yield differential at -15bps.

- The bills strip is little changed.

- This week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond on Wednesday and A$1000mn of the 2.75% 21 November 2029 bond on Friday.

BONDS: NZGBS: Closed Slightly Richer, RBNZ Policy Decision On Wednesday

NZGBs closed mid-range, 2bps richer.

- Cash US tsys are flat to 3bps richer in today's Asia-Pac session after resuming trading following the long weekend.

- Swap rates closed 1-2bps lower.

- Tomorrow, the local calendar will be empty, with the next major event on the calendar being the RBNZ Monetary Policy Review on Wednesday.

- A majority of members in the NZIER Monetary Policy Shadow Board recommend that the RBNZ keep the cash rate on hold at 3.25%.

- RBNZ dated OIS pricing is little changed across meetings today. 3bps of easing is priced for this week's meeting, with a cumulative 31bps by November 2025.

- Notably, pricing is 9-15bps firmer across 2025 meetings compared to pre-RBNZ decision levels on May 28

- (Bloomberg) RBNZ Chief Economist Paul Conway will give a speech about global tariffs on July 24, from 1:30 pm in Wellington, the central bank says in an emailed advisory. Speech will cover the various ways global tariffs will impact us here in New Zealand, and how the RBNZ is thinking through the impacts on inflation and the economy more broadly.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 3.00% Apr-29 bond and NZ$200mn of the 4.50% May-35 bond.

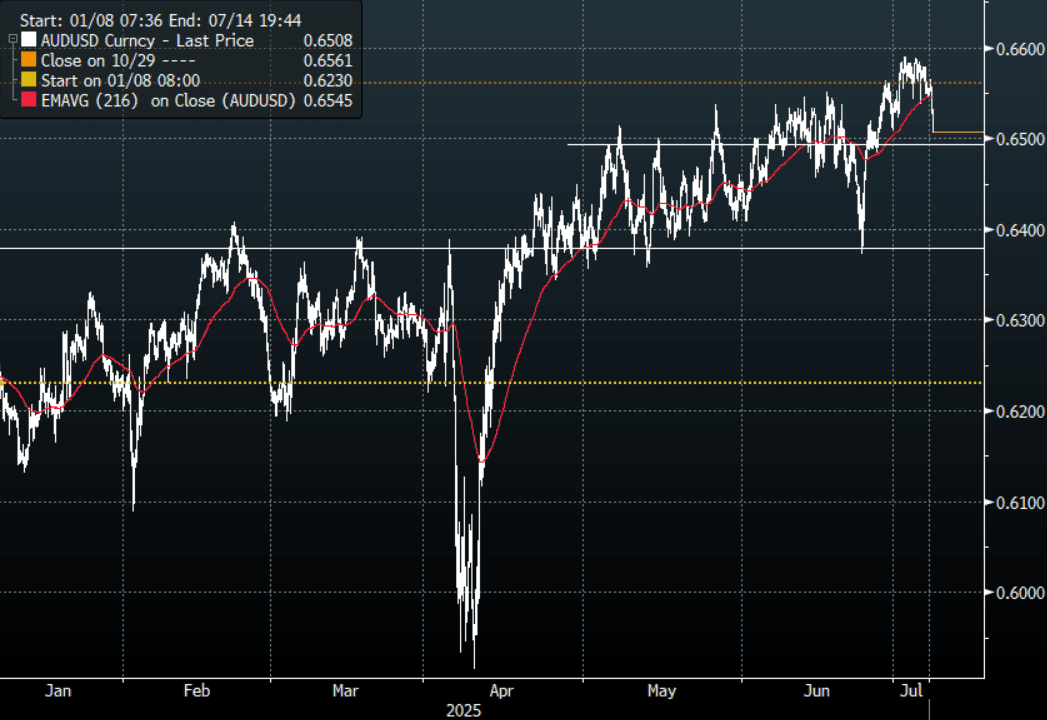

AUD: Asia Wrap - AUD/USD Trades Heavy As Market Eyes Tariff Deadline

The AUD/USD had a range Friday night of 0.6507- 0.6565, Asia is trading around 0.6510. The AUD/USD drifted off the 0.6600 area once again as stocks pared back some of its recent gains as the market eyes the tariff deadline approaching this week. Look for more consolidation again in the AUD/USD as the pair continues to try build a base from which to move higher. The risk to this is clearly around President Trump escalating trade tensions this week, which could make it a choppy week. First support is towards 0.6500 then more importantly the 0.6350/0.6400 area.

- (Bloomberg) -- “Australia’s May spending data presents a conundrum — are consumers struggling, or thriving? Weak retail trade data on Wednesday suggests consumers, plagued by uncertainty, are keeping their wallets shut. Stronger-than-expected broader spending data on Friday shows a weather-related pickup in winter clothes shopping was complemented by a discretionary surge in car sales and hospitality spending.”

- The AUD/USD is attempting to break through the top of its recent range as the pressure on the USD increases. The move higher does seem to be stalling though as the market eyes the tariff deadline. First support is towards 0.6500 then more importantly the 0.6350/0.6400 area.

- The AUD needs a sustained break above 0.6600 to potentially start building momentum for an extended move higher, a close back above 0.6600 and the focus would turn back to 0.6900/0.7000.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD884m), 0.6500(AUD 510m), 0.6700(AUD 652m). Upcoming Close Strikes : 0.6650(AUD857m July 10), 0.6375(AUD722m July 8)

Fig 1: AUD/USD spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

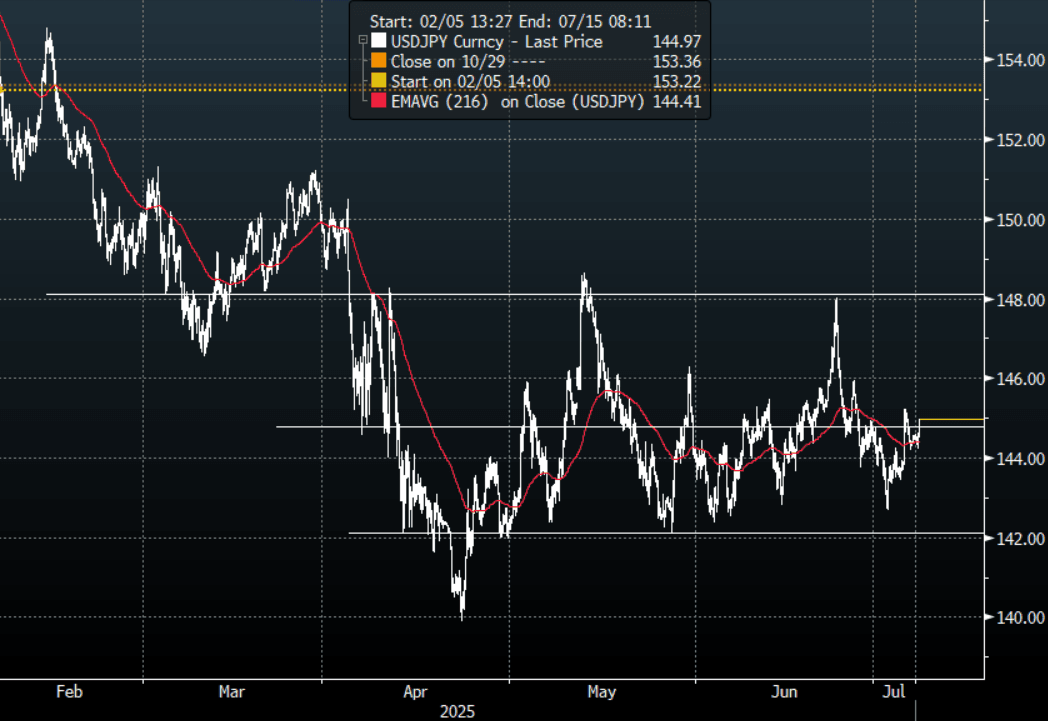

JPY: Asia Wrap - USD/JPY Finds Demand, Still Trades In The Middle Of Its Range

The Asia-Pac USD/JPY range has been 144.23 - 144.99, Asia is currently trading around 144.95, +0.35% having found decent demand back towards the 144.20 area in our session. Price is now back in the middle of the wider 142.00 - 148.00 range and the pair will probably continue to take its cue from the US rates market which opened again this morning after the long weekend.

- MNI Brief: Japan’s May Negative Real Wage Widens. Japan’s inflation-adjusted real wages, a key gauge of household purchasing power, remained negative for the fifth straight month in May, falling 2.9% y/y following April’s 2.0% decline, preliminary data from the Ministry of /health, Labour and Welfare showed Monday. The drop marks the steepest decline since September 2023, when real wages also fell 2.9%.

- Bloomberg - “Japanese Prime Minister Shigeru Ishiba said the country is prepared for all possible tariff scenarios, speaking on Fuji TV’s “Sunday News The Prime” program. Japan is ready to “stand firm” and defend its interests while anticipating every possible situation, says Ishiba.”

- “We will be pushing for zero tariffs on automobiles," Ishiba adds. He notes that Japan is the largest investor in the US and the biggest job creator there.”

- "AOKI: JAPAN, US CONTINUING ACTIVE TARIFF DISCUSSIONS”- BBG

- The rejection of 148.00 points to a potential top being in place now and shows just how quick the market is to return to selling USD’s. USD/JPY was looking for a fresh catalyst to probe the lower end of its range again but NFP did not provide that so we are now back in the middle of the range. The JPY bulls will be hoping the move higher in US yields is capped as a break higher in rates would begin to make a long JPY market vulnerable with its preference to express a short.

- Options : Close significant option expiries for NY cut, based on DTCC data: 143.85($550m).Upcoming Close Strikes : 144.50($840m July9), 142.75(AUD$855m July8).

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

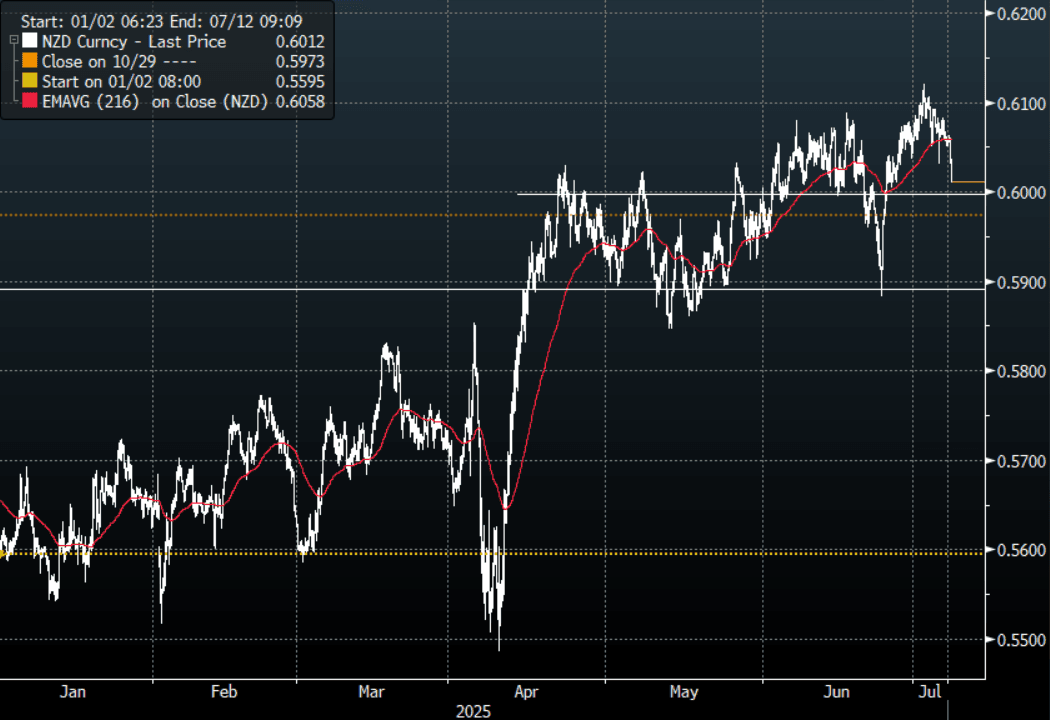

NZD: Asia Wrap - NZD/USD Trades Soft As Risk Eyes Tariff Deadline

The NZD/USD had a range of 0.6009 - 0.6063 in the Asia-Pac session, going into the London open trading around 0.6010, -0.83%. The pair has traded under pressure for most of our session as the deadline for tariffs approaches and the risk this presents to global growth. The NZD should find support again around the 0.6000 area as it tries to build a base from which to move higher, a sustained break below here though would risk a deeper correction back to 0.5850/0.5900.

- "RBNZ SHADOW BOARD RECOMMENDS CASH RATE IS HELD THIS WEEK: NZIER" - BBG

- (Bloomberg) - “This week’s antipodean central bank meetings could set the stage for an Australian dollar rally against the kiwi — and spark a selloff in Aussie government bonds.”

- “The Reserve Bank of Australia is widely expected to deliver a second consecutive interest-rate cut, its first back-to-back easing in six years, while the Reserve Bank of New Zealand is likely to hold firm. That policy divergence is sharpening tactical positioning in FX and rates markets.”

- US President Trump has posted via Truth Social that the US will start delivering letters outlining tariff levels to various countries starting 12pm Monday, US eastern time. Trade deals will also be announced at the same time.

- A huge bounce from sub 0.5900 and the NZD has established a foothold above 0.6000, with the USD breaking lower the NZD/USD looked to be building for a potential break higher of its own. A sustained break back below 0.6000 though could negate this and risk a deeper reversion back to the 0.5850/0.5900 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6075(NZD519m July 9), 0.6000(NZD407m July10).

- AUD/NZD range for the session has been 1.0811 - 1.0832, currently trading 1.0825. The cross is struggling to get any momentum for now. It looks to be in a 1.0750 - 1.0850 range for now as it awaits a catalyst to provide some clearer direction.

Fig 1: NZD/USD Spot hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Stocks Weaken Ahead of Tariff Deadlines

As the July 9 deadline for trade talks draws near, risk appetite worsened in Asia as major bourses fell. Trump has not helped by claiming that those BRIC countries whose policies are not aligned with the US will face an additional 10% levy, weighing heavy on Asia's currencies today.

- China's major bourses are all down today in a weak start to the week. The Hang Seng is down -0.45%, the CSI 300 down -0.59%, Shanghai Comp down -0.20% and the Shenzhen Comp down -0.15%.

- In Taiwan the TAIEX fell -0.93% today.

- The KOSPI was one of the few gainers, up +0.18% today ahead of this week's decision by the BOK.

- The FTSE Malay KLCI is down -0.83% whilst the Jakarta Composite down by just -0.05%.

- The FTSE Straits Times in Singapore was up +0.30% whilst the PSEi in the Philippines was up +0.07%.

- The NIFTY 50 ended Friday up +0.22% but is down in Monday morning trade by -0.11%.

- Following the decision that the OPEC+ increase in production in August will be greater than expected, oil's fall continued decline continued today.

- WTI declined -1.3% to US$66.24 bbl

- Brent declined -0.75% to US$67.98 bbl.

- OPEC+ had speculated that the rise in August output could be in the region of 400k barrels a day. Instead it announced a 548k increase citing summer demand at a time when global growth is challenged by the US tariffs.

- It has been one of President Trump's key policies (lower gas prices) and his ongoing pressure on OPEC+ appears to be paying off.

- The OPEC+ group has not finalized its output decision for September but speculation remains for a further increase.

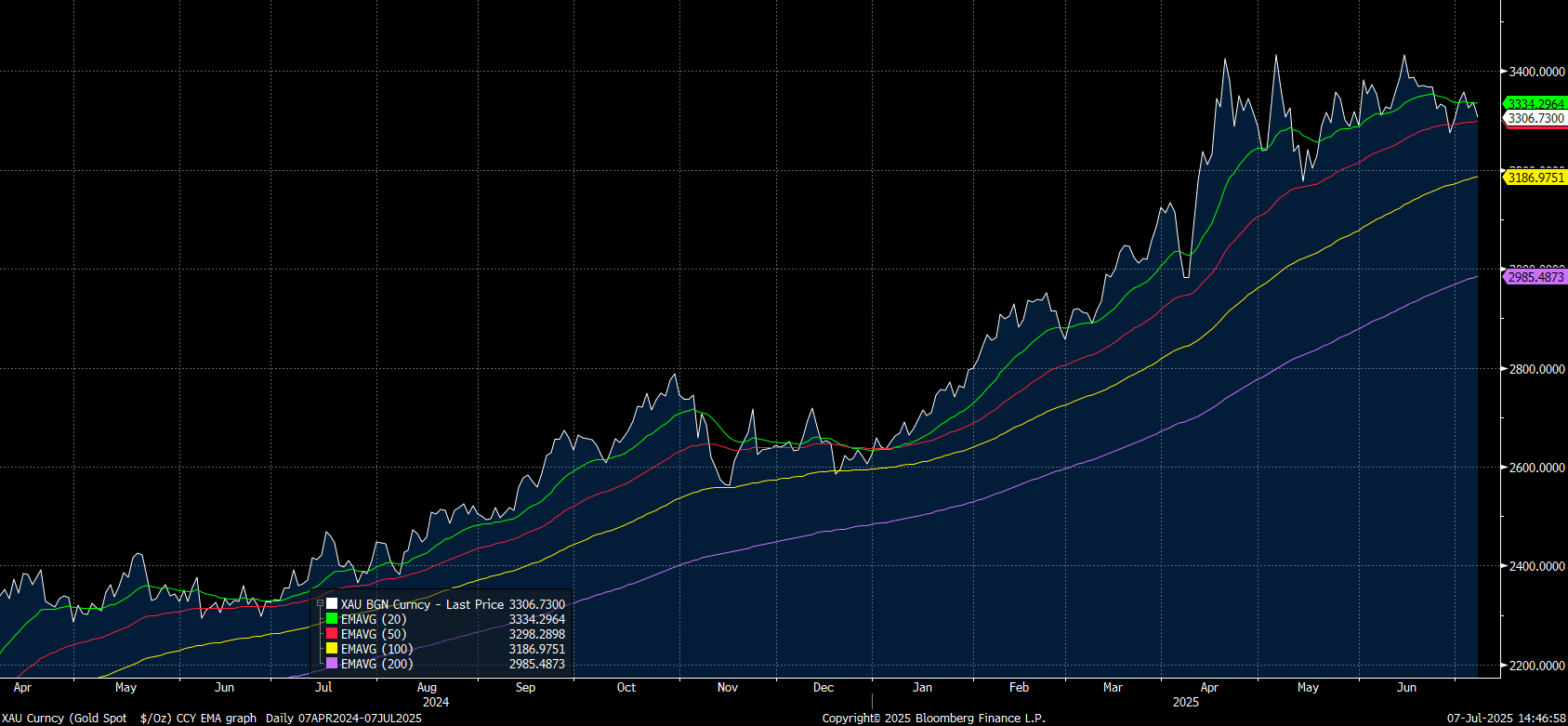

Gold Falls Ahead of Tariff Deadline

- Gold edged lower in the Asia trading day ahead of a week that could be dominated by tariff headlines.

- As the July 9 deadline for US tariffs draws nearer, some of the major equity bourses fell as did gold.

- Gold had opened at US$3,337.16 at this morning's open and by early afternoon was down -0.90% at $3,307.38.

- With the US Treasury Secretary Scott Bessent indicating that there could possibly be extensions due ongoing negations, it seems likely that risk appetite for many asset classes could remain muted this week.

The move lower sees gold edge towards the 50-day EMA of $3,298.28.

source: Bloomberg Finance LP / MNI

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 07/07/2025 | 0600/0800 | ** | Industrial Production | |

| 07/07/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 07/07/2025 | 0900/1100 | ** | Retail Sales | |

| 07/07/2025 | - | ECB Lagarde and Cipollone In Eurogroup Meeting | ||

| 07/07/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 07/07/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 08/07/2025 | 2350/0850 | Balance of Payments | ||

| 08/07/2025 | 0430/1430 | *** | RBA Rate Decision | |

| 08/07/2025 | 0500/1400 | Economy Watchers Survey | ||

| 08/07/2025 | 0600/0800 | ** | Trade Balance | |

| 08/07/2025 | 0645/0845 | * | Foreign Trade | |

| 08/07/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 08/07/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 08/07/2025 | - | ECB de Guindos At ECOFIN Meeting | ||

| 08/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index |