EM LATAM CREDIT: MNI EM Credit Market Wrap - LATAM (23 Apr)

Source: BBG

Measure Level Δ DoD

5yr UST 4.00% +1bp

10yr UST 4.38% -2bp

5s-10s UST 37.6 -3bp

WTI Crude 62.2 -1.5

Gold 3293 -88.1

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 869bp -19bp

BRAZIL 6 1/8 03/15/34 283bp -7bp

BRAZIL 7 1/8 05/13/54 378bp -8bp

COLOM 8 11/14/35 461bp -10bp

COLOM 8 3/8 11/07/54 541bp -10bp

ELSALV 7.65 06/15/35 465bp -30bp

MEX 6 7/8 05/13/37 296bp -5bp

MEX 7 3/8 05/13/55 358bp -6bp

CHILE 5.65 01/13/37 165bp -8bp

PANAMA 6.4 02/14/35 354bp -9bp

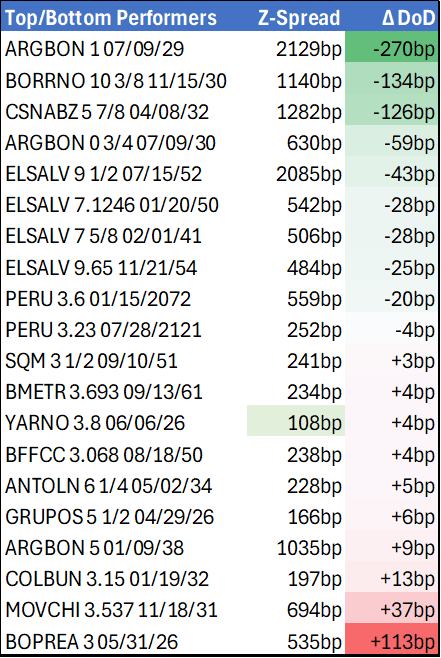

CSNABZ 5 7/8 04/08/32 648bp -42bp

MRFGBZ 3.95 01/29/31 345bp -11bp

PEMEX 7.69 01/23/50 706bp -20bp

CDEL 6.33 01/13/35 232bp -5bp

SUZANO 3 1/8 01/15/32 227bp -12bp

FX Level Δ DoD

USDBRL 5.72 -0.01

USDCLP 942.88 +0.38

USDMXN 19.7 +0.04

USDCOP 4305.99 +11.01

USDPEN 3.69 -0.00

CDS Level Δ DoD

Mexico 145 (5)

Brazil 193 (8)

Colombia 277 (8)

Chile 77 (3)

CDX EM 95.51 0.29

CDX EM IG 99.92 0.05

CDX EM HY 91.06 0.42

Main stories recap:

· President Trump said he never intended to fire Fed Chair Powell and made vaguely positive comments regarding China tariff negotiations while Elon Musk said he will spend more time managing Tesla, all of which was enough to trigger a second day of gains in U.S. equities.

· US Treasuries also stabilized after some heightened volatility in past days and that, along with a strong rally in global equity prices, helped to coax the EM primary market back to life.

· In the Asia and CEEMEA primary market we saw Ajman Bank, Hanwa, Hebei, Kaifeng, OCP and CEZ announced new issues. LATAM followed through with a Peruvian bank BCP subordinated tier 2 issue.

· The EM CEEMEA secondary market was strong with benchmark bond spreads of high beta issuers like Angola, Nigeria and Egypt tightening 20-40bps.

· The same pattern could be seen in LATAM with Brazil high yield names tightening 10-15bps but more cyclical credits that underperformed MTD like CSN moved about 40 bps tighter.

· Argentina and Colombia sovereign bonds tightened 10-20bps even as oil prices fell 2% today while El Salvador outperformed even more, improving by 30bps.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Bullish Outlook

- RES 4: 165.43 High Nov 8

- RES 3: 164.90 High Dec 30 ‘24 and a key medium-term resistance

- RES 2: 164.55 High Jan 7

- RES 1: 164.19 High Mar 18 and the bull trigger

- PRICE: 162.51 @ 16:55 GMT Mar 24

- SUP 1: 160.74 Low Mar 20

- SUP 2: 160.28 50-day EMA

- SUP 3: 158.90 Low Mar 10

- SUP 4: 158.00 Round number support

The recent move down in EURJPY appears corrective and has allowed an overbought trend condition to unwind. Short-term pivot support to watch is 160.28, the 50-day EMA. A break of this level would signal potential for a deeper retracement. Recent gains resulted in a print above resistance at 164.08, the Jan 24 high. A clear break of this hurdle would open 164.90, the Dec 30 ‘24 high.

CANADA DATA: Manufacturing Sales Set To Pull Back After Strong January

The advance estimate of Canadian manufacturing sales shows a 0.2% M/M nominal decline in February, led by falls in food / petroleum and coal products, per StatCan.

- If confirmed, it would mark the weakest reading / first decline (in nominal terms) since September.

- Recall that the prior figure (+1.7% M/M) reflected a strong rise in motor vehicle and primary metals sales, and though real sales rose by just 0.9%, the latter should mean a decent contribution from industry to January GDP (out Friday; consensus is +0.3% M/M after +0.2%).

- However - pending prelim wholesale sales data out this Wednesday - industry in February may have proven sequentially weaker, and comes against a backdrop of uncertainty and volatility amid a nascent US-Canada trade war.

US TSYS: Targeted Tariffs Helps Buoy Sentiment

- Treasuries look to finish near lows Monday as Trump admin trade policy narrowed from universal tariffs to more targeted approach when the April 2 "Liberation Day" arrives.

- Treasury futures extended lows after S&P Flash PMI services (54.3 bbg cons 51.0) and composite (53.5 cons 50.9) data came out higher then expected while manufacturing declined (49.8 bbg cons 51.7).

- Atlanta Fed Pres Bostic (non-2025 FOMC voter, leans hawk) says in a Bloomberg interview that he has reduced his 2025 rate cut expectations to 1 in March's economic projections versus 2 previously, "because I think we will see inflation be very bumpy", and delayed inflation progress warranted pushing back the path to neutral rates.

- The Jun'25 10Y currently trades 110-17 (-18), just above initial technical support at 110-16.5 (Low Mar 24) followed by 110-12.5 (Low Mar 6 & 13). Resistance above at 111-25 (Mar 11 high), support below at 110-12.5/110-00 (Low Mar 6 & 13 / High Feb 7). Tsy 10Y yield climbs to 4.3346% high, curves still mixed: 2s10s +.014 at 29.406, 5s30s -1.943 at 56.480.

- Late tariff headlines saw risk sentiment cool slightly after Trump said he would announce additional tariffs on cars "shortly" and pharmaceuticals at "some point".