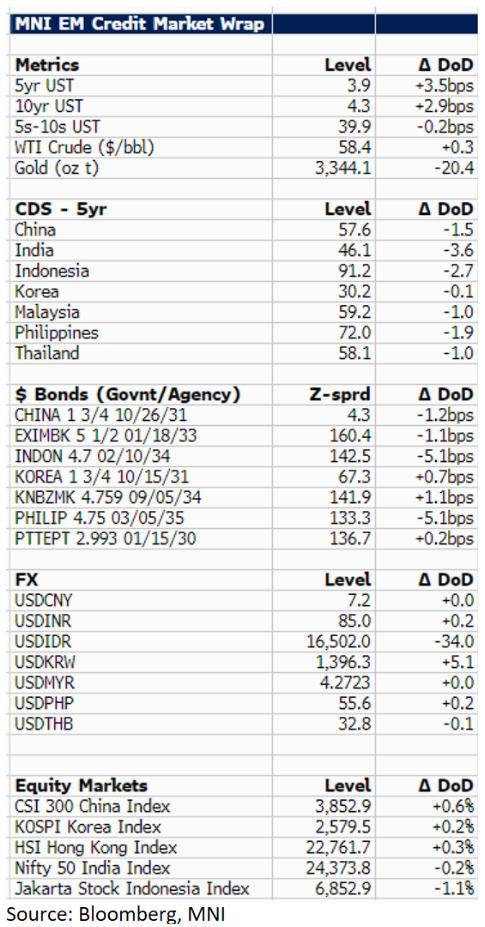

EM ASIA CREDIT: MNI EM Credit Market Update - Asia

U.S. 10y treasury yields widened 3bp during the Asia session with a yield of 4.3% with the market focused on the upcoming announcement from President Trump about a major deal with an unnamed, "big, and highly respected" country. The NYT newspaper has reported it will be the U.K. Meanwhile China continues to reiterate the U.S. needs to revoke its unilateral tariffs.

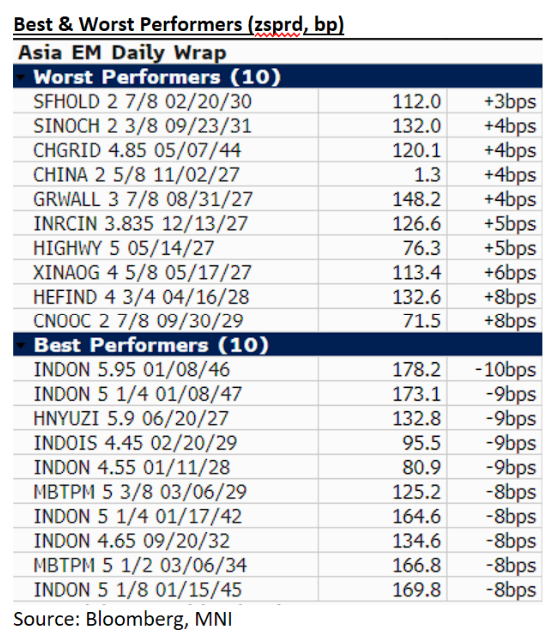

Asia EM credit is mostly better today with Govie/agency $ spreads up to 5bp tighter, the outliers being the Philippines (-5bp) and Indonesia (-5bp). On the geo-political front, India and Pakistan tensions didn’t materially escalate overnight, with markets likely expecting a de-escalation. In terms of new issuance, we have the previously mandated Medco Energi $benchmark 5NC2 in the market with an IPT of 9.125%, we estimated FV at 8.45%. Otherwise no new deal announcements.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOE: Larger MPC cuts possible - but it's former doves calling for them now

- There has been a lot of focus this morning on the Guardian article in which ex-MPC members Bean and Blanchflower argued for large imminent cuts. Bean has argued for a 50bp cut in May and Blanchflower for an intermeeting cut.

- It is important to put the views of these former policymakers into context, however, with both having a dovish leaning (albeit Blanchflower much more than Bean): Bean dovishly dissented in 5/166 MPC meetings (remember that meetings were monthly when he was on the MPC). Blanchflower dissented in half of his 36 meetings (including favouring a 50bp cut in September 2008 when the majority of the MPC voted to keep Bank Rate on hold).

- So in lots of ways, it is to be expected that two former doves remain dovish.

- Having said that, Bean does make some good points. He emphasises how much weight the MPC put on the Agents' feedback during the financial crisis - and we know that the current MPC also pays a lot of attention to the Agents now (particularly with regard to pay expectations). If the Agents' feedback is more concerning than things like the PMIs suggest, then there is a good chance the MPC acts more aggressively than the market expects.

- However, there are still inflationary challenges for the MPC to contend with: the potential passthrough from employer NICs to prices, higher wages than are consistent with a 2% inflation target, food prices starting to pick up and to move even higher later this year with a new packaging tax. For now it looks less likely the UK will introduce extra tariffs which would be inflationary (but can't be fully ruled out).

- However, with confidence suffering we think a cut does look likely in May at least. And there is likely to be at least Dhingra voting for 50bp. We will be watching closely any further MPC comments to see if there is any change in view elsewhere. Lombardelli is on a panel at 17:00BST today while Breeden is at an MNI Connect webinar Thursday (register here).

- What about past May? The next 5 days are hard to predict at the moment, let alone months into the future. We think the BOE will try and keep communications about future actions very restrained.

EQUITIES: FTSE Block trade

FTSE block trade, suggest seller.

- Z M5 2k at 7785.00.

US TSY FLOWS: US Tnotes is through the Overnight high, USDJPY tests 147.00

- The US Tnotes is now also through its overnight high, but initial resistance area is seen further out up to ~112.24+

- The price action is helping the USDJPY through the 147.00 figure, this is well within Yesterday's big range of 144.82/148.18 (low/high).