EM LATAM CREDIT: MNI EM Credit Market Wrap - LATAM (21 May)

Source: BBG

Measure Level Δ DoD

5yr UST 4.14% +7bp

10yr UST 4.58% +9bp

5s-10s UST 43.6 +2bp

WTI Crude 61.6 -0.5

Gold 3315 +25.3

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 850bp -3bp

BRAZIL 6 1/8 03/15/34 255bp -3bp

BRAZIL 7 1/8 05/13/54 365bp -3bp

COLOM 8 11/14/35 412bp -0bp

COLOM 8 3/8 11/07/54 501bp +1bp

ELSALV 7.65 06/15/35 421bp +2bp

MEX 6 7/8 05/13/37 274bp -0bp

MEX 7 3/8 05/13/55 339bp +2bp

CHILE 5.65 01/13/37 153bp -0bp

PANAMA 6.4 02/14/35 329bp +9bp

CSNABZ 5 7/8 04/08/32 551bp -4bp

MRFGBZ 3.95 01/29/31 259bp +3bp

PEMEX 7.69 01/23/50 631bp +4bp

CDEL 6.33 01/13/35 208bp -1bp

SUZANO 3 1/8 01/15/32 210bp -4bp

FX Level Δ DoD

USDBRL 5.66 -0.01

USDCLP 943.81 -0.26

USDMXN 19.4 +0.10

USDCOP 4176.56 +7.30

USDPEN 3.68 -0.01

CDS Level Δ DoD

Mexico 121 3

Brazil 167 4

Colombia 228 4

Chile 58 2

CDX EM 96.77 (0.20)

CDX EM IG 100.84 (0.10)

CDX EM HY 92.69 (0.28)

Main stories recap:

Comments

· Concerns about debt sustainability amid the raging budget battle in Congress pressured US Treasury yields higher at the open and then a poorly received 20-year U.S. Treasury auction led to further weakness with equities also reacting negatively.

· EM USD bonds were unfazed early on with Asia spreads tightening 1-2 bps while in CEEMEA there was generally a widening bias in a flat/+20bps range.

· The primary market was active once again with two new deals pricing in Asia and seven in CEEMEA.

· LATAM primary was quiet, though there were two new Argentina deals simmering on the back burner.

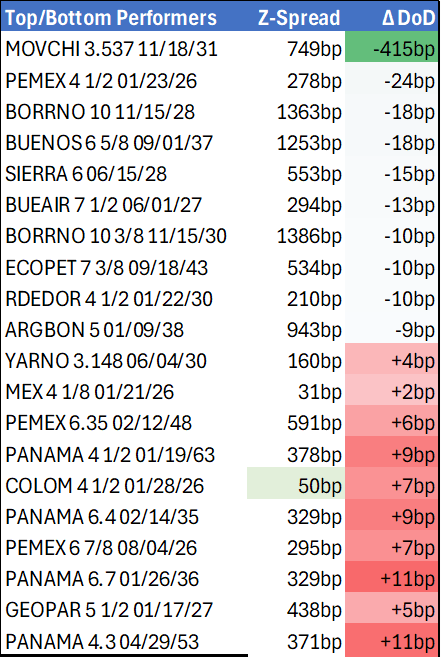

· In the LATAM secondary market, Telefonica Moviles Chile (MOVCHI) bonds were up 12 points on news that the liquidity challenged Chilean telecom company was getting a 5-year loan for CLP371bn (USD393mn) from the parent company Telefonica of Spain.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Tariff Tied Headline Risk & Fed Independence Meddling

- Treasuries look to finish mostly lower Monday, curves twist steeper as the short end outperforms a sell-off in the long end, risk sentiment hampered as stocks hold at or near session lows.

- Headline risk continues to rattle markets, latest focus partially tied to headlines that the WH is in the process of replacing Sec of Defense Hegseth following reports of another Signal Chat leak made the rounds. Politico reported GOP Rep Bacon said "Hegseth should Go". Conversely, WH Press Sec Leavitt just said the NPR report is false.

- Global trade remains the greater concerns, markets await something concrete in tariff negotiations vs. hopes and promises that talks with dozens of countries is going well, while Pres Trump berates Fed Chairman Powell and reiterating a call for "preemptive cuts".

- Curves near late highs: 2s10s currently +13.246 65.492 vs. 66.377 high, 5s30s +8.604 at 94.411. Jun'25 10Y futures -13.5 at 110-24 vs. late overnight low of 110-22. Technical at 110-15/109-08 (Low Apr 15 / 11 and the bear trigger). In turn, projected rate hike pricing gain momentum vs. morning levels (*) as follows: May'25 at -4bp (-3.4bp), Jun'25 at -19.8bp (-19bp), Jul'25 at -43.6bp (-40.1bp), Sep'25 -63.4bp (-59.9bp).

- Stocks reacting negatively, extending lows with SPX eminis slipping to 5127.25 low, Consume Discretionary and IT sectors underperforming. US$ broadly weaker, BBG index -8.47 at 1216.21.

- Tuesday Data Calendar: several Fed speakers, Richmond Fed data and Tsy $69B 2Y Note Sale.

US STOCKS: Late Equities Roundup: Hugging Lows

- Stocks are holding near deep session lows in late Monday trade, Consumer Discretionary and Information Technology sectors continue to underperform with lack of clarity and communication over trade negotiations widely sited.

- Currently, the DJIA trades down 1258.06 points (-3.21%) at 37884.8, S&P E-Minis down 180.5 points (-3.4%) at 5132 (April 10 lows, still off April 7 low of 4832.00, The Nasdaq down 596.8 points (-3.7%) at 15689.37.

- Information Technology and Consumer Discretionary sectors continued to underperform, semiconductor makers primarily weighing on the IT sector: Super Micro Computer -7.60%, Arista Networks -6.04%, NVIDIA -5.76%, Palo Alto Networks -5.47%, Oracle -5.41% and Broadcom -4.91%.

- The Consumer Staples sector weighed down by Tesla -6.91%, DoorDash -5.87%,Chipotle Mexican Grill -4.48%, Carnival -4.22%, Ross Stores -4.01% and TJX Cos -3.93%.

- A mix of Financials, interactive media and pharmaceuticals outperformed in late trade: Discover Financial Services +3.34%, Fidelity National Information +3.00%, Netflix +1.40%, Moderna +1.34% and Dollar General +1.15%.

- Equity earnings resume after the close: Hexcel Corp, Medpace Holdings Inc, W R Berkley Corp, AGNC Investment Corp and Western Alliance Bancorp reporting.

PIPELINE: Corporate Bond Update, $5B American Express 4Pt Priced

- Date $MM Issuer (Priced *, Launch #)

- 04/21 $5B *American Express $1.6B 4NC3 +98, $400M 4NC3 SOFR+126, $1.5B 6NC5 +108, $1.5B 11NC10 +128

- 04/21 $700M Excelerate Energy 5NC2

- 04/21 $2B QXO Inc. 7NC3 investor calls