EM ASIA CREDIT: MNI EM Credit Market Update - Asia

Asia EM USD sovereign and agency spreads are trading in a -1bp to +2bp range this morning, while regional equities are mostly in positive territory, led by the Korean KOSPI (+2%). In primary markets, KEB Hana Bank priced its 3Y USD deal overnight broadly in line with fair value (T+43bp). This morning, China Water Affairs brought a USD 5NC3 deal (IPT 6.375% area; our fair value around 6.2%), while Korea has mandated banks for a new USD 5Y issue likely to come next week. Separately, Sunac China’s creditors have agreed to the company’s restructuring plan.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Closed Cheaper Ahead Of A Busy Week Of Local Data

NZGBs closed 2-4bps cheaper, with the 2/10 curve steeper.

- Swap rates closed 1-3bp higher.

- (Bloomberg) “Economic activity is expected to pick up over the second half of 2025 but there is uncertainty surrounding the pace of recovery, the Treasury Dept. says in its Fortnightly Economic Update released Monday in Wellington.”

- The focus of the week will be on Thursday’s Q2 GDP data release. Bloomberg consensus is in line with the RBNZ’s August forecast of -0.3% q/q bringing the annual rate to flat after declining 0.7% y/y in Q2. 25bp rate cuts are expected at both the October 8 and 26 November meetings.

- August monthly price series including food, electricity, rent, petrol and travel print on Tuesday. Food price inflation has been picking up. There is a risk that Q3 CPI inflation exceeds the 3% top of the RBNZ’s target band. The bank is forecasting 3% for the quarter.

- On Wednesday, Q3 current account data is out and the deficit is expected to narrow to 4.8% of GDP but with it widening to $2.7bn from $2.32bn in Q2.

- There is also Westpac Q3 consumer confidence on Wednesday.

- RBNZ dated OIS pricing closed little changed across meetings. 22bps of easing is priced for October, with a cumulative 40bps by November 2025.

CHINA: Bond Futures Rise Monday

- China's bond futures higher Monday, with the 10-Yr leading.

- Up +0.10 the 10-Yr is at 107.78, below the 20-day EMA of 107.90.

- The 2-Yr future is lower by -0.01 at 102.35, to remain below the 20-day EMA of 102.38.

- The 10-Yr CGB is lower by -1bp at 1.79%

JPY: Asia Wrap - USD/JPY Trading Sideways On A 147 Handle

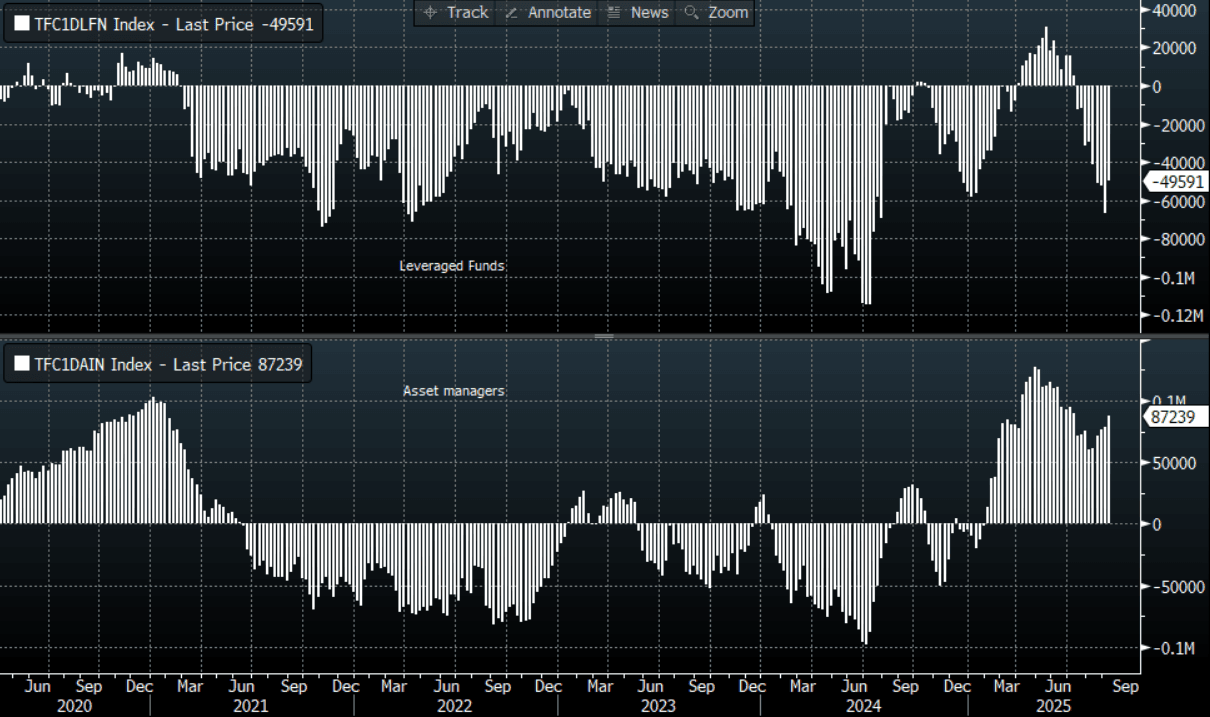

The USD/JPY range has been 147.37 - 147.79 in the Asia-Pac session, it is currently trading around 147.40, -0.20% on a Japanese holiday. USD/JPY continues to trade sideways with no clear trend. The price remains in the middle of its recent 146-149 range, and we need a convincing break to see a clearer direction again. CFTC data shows leveraged funds paring back some of their short JPY position last week but remain core short, looking for this support to continue to hold. A move back below 145/146 is needed to potentially start seeing these positions being flushed out.

- MNI INTERVIEW: Powell Won't Signal String Of Fed Cuts-Lockhart. Federal Reserve Chair Jerome Powell will justify next week’s widely expected interest rate cut by citing rising downside risks to employment but refrain from signaling a string of cuts beyond September because the Fed must also contend with inflation heading in the wrong direction, former Atlanta Fed President Dennis Lockhart told MNI.

- "JAPAN'S HAYASHI TO ANNOUNCE ENTRY IN LDP RACE TOMORROW: NIKKEI" - BBG

- "TAKAICHI LEADS LDP RACE AT 29%, KOIZUMI AT 25% IN YOMIURI POLL" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 150.00($1.04b).Upcoming Close Strikes : 146.00($1.41b Sept 16), 150.00($1.49b Sept 16), 145.70($1.22b Sept 17) - BBG.

- CFTC data shows last week asset managers again added to their JPY longs again as they look to rebuild their position +87239( Last +78427), leveraged funds reduced their short position perhaps losing confidence the support will continue to hold -49591(Last -66914).

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P