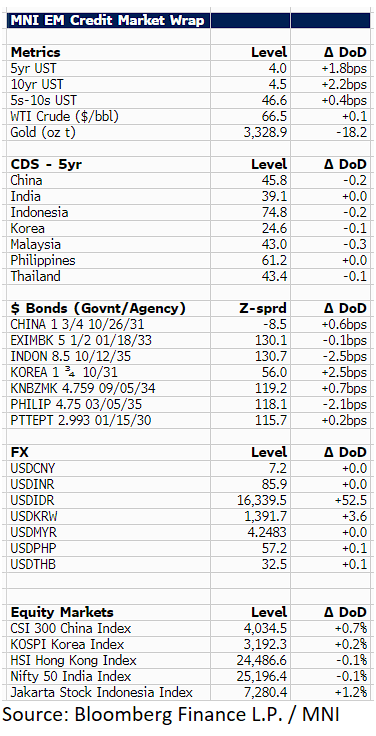

EM ASIA CREDIT: MNI EM Credit Market Update - Asia

U.S Treasury yields are 2bp higher at 4.5%, with President Trump stating overnight he has no plans to fire Federal Reserve Chair Jerome Powell.

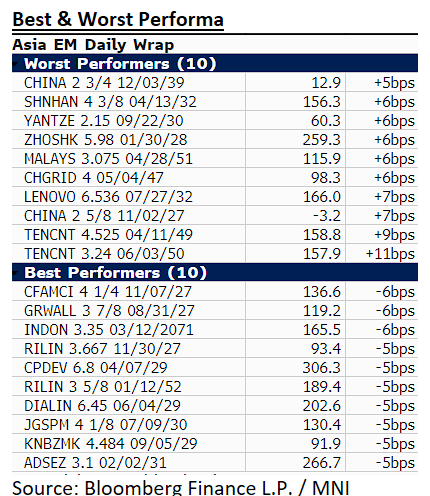

In LATAM spreads overnight were about 5-10bp wider on the day, while Asia EM $ credit was mixed, with spreads ranging between -2bp and 2bp. There were no notable outliers, though it’s worth highlighting that Indonesia (INDON 10/35s, -2bp) agreed to a trade deal with the U.S. at a 19% rate—significantly lower than the previous 32% indicated in the Trump tariff letter. Additionally, Indonesia’s central bank cut rates by an unexpected 25 basis points yesterday.

In other news, Korea Gas may increase LNG imports from the U.S. as part of ongoing trade negotiations, potential doubling U.S. imports. Adani Port spreads are 3bp wider following gains related to $ buyback announcements yesterday. In terms of results, the Bank of the Philippine Islands posted strong H1 numbers, reporting net income growth of 8% year-on-year. Finally, closely followed TSMC, reported operating income +62% YoY as demand for AI chips remains strong.

There were no new issues today.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Bear Steepening, Supply Eyed This Morning

Gilts follow Bunds lower, with a lack of significant escalation in the Israel-Iran conflict and a late NY dip in Tsys factoring into the move early today.

- Futures stick within yesterday’s range, trading as low as 92.37.

- Bullish technical conditions remain intact in the contract, initial support and resistance located at yesterday’s low (92.23) & the 50.0% retracement of the Jun 13-16 down leg (92.95), respectively.

- Yields 2-4bp higher, curve steeper.

- 10s last 4.57%, with last week’s move below 4.50% and break of long-term uptrend support lacking traction and quickly fading.

- 2s10s and 5s30s remain in multi-week ranges, last trading 63.6bp and 122.7bp, respectively.

- SONIA futures now -1.0 to -3.0 after printing flat to -2.0 into the gilt open.

- BoE-dated OIS still showing ~48bp of cuts through year-end.

- Our full preview of tomorrow’s inflation data is available here.

- On the supply front, the DMO will come to market with GBP4.5bln of the 4.375% Mar-30 gilt this morning.

BOJ: Ueda: Won't Rule Out Any Future MonPol Tools

Ueda's press conference continues to have a limited impact on markets, with USDJPY still little changed on the session. Latest headline flow has seen the Governor say that there is no definitive answer on whether long-term rates can be controlled.

In response to a question on whether a return to YCC was possible, he said that he did not want to rule out any future monetary policy tools.

EQUITIES: US and EU Roll pace update

September is the Front Month for US Equity Futures, but not quite just there for European Indices.

ROLL PACE: The EU roll pce is as of Yesterday, but spread volume dominates in early trade.

US:

- SPX: 57%.

- NDX: 50%.

- DOW: 50%.

EU:

- VGA: 35%.

- DAX: 26% (below Pace).

- FTSE: 48%.