EM ASIA CREDIT: MNI EM Credit Market Update - Asia

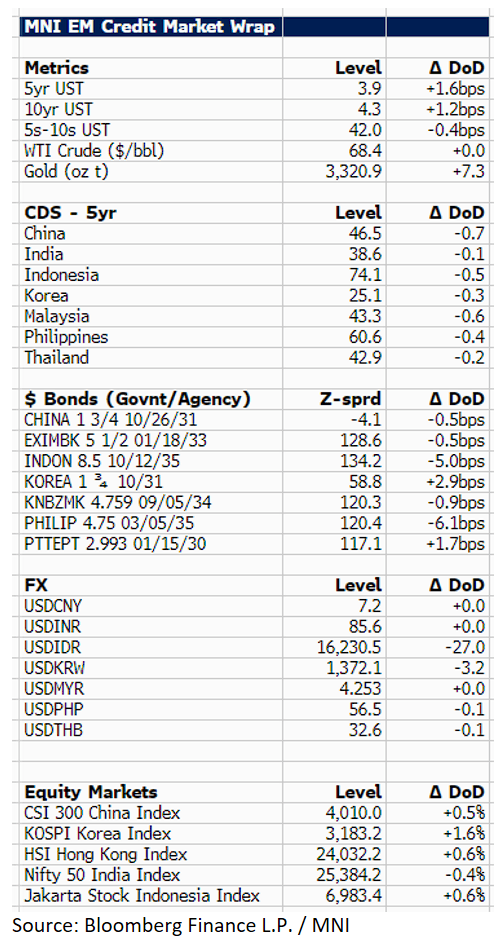

U.S Treasury yields are 1bp higher at 4.3% with U.S. President Trump having announced possible new tariffs overnight, including for emerging markets (Brazil, Thailand).

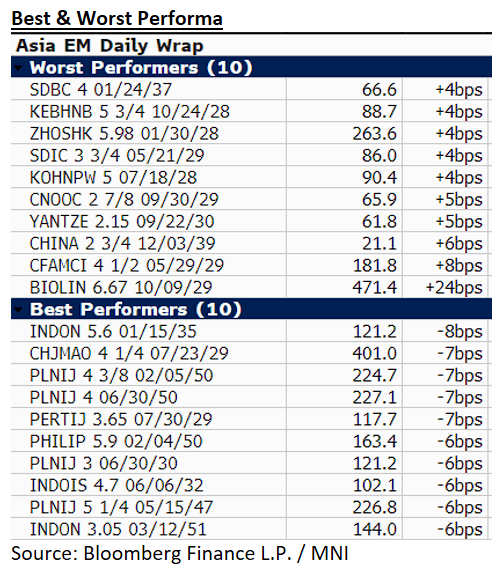

In LATAM spreads were 1-8bp wider. In Asia, EM $ credit was mixed, with spreads ranging from -6bp to +3bp. The outliers being the Philippines (PHILIP 5/35 -6bp), Indonesia (INDON 10/35 -5bp) and Korea (KOREA 10/31 +3bp).

The trading session continued to be dominated by tariffs, U.S. President Trump launched a new set of tariff letters overnight, with emerging markets countries Brazil (50% rate) and the Philippines (20% rate) in the frame. Potential new tariffs on Brazil have also been linked to the political situation in the country, possibly widening the negotiating landscape beyond pure economics for all.

Asia equities are in positive territory with the Korean KOSPI up around 1.5%. In terms of newsflow, Adani Ports reported to have raised $100m, possibly for bond buybacks and San Miguel is looking to exchange $ perps into a new note. Finally, we had reports of possible China State support for the real estate sector coming next week, the information was unverified. We note that valuations are trading at the YTD highs, with Vanke $ bonds up 1pt today. There were no new deals today.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: Longer dated Put Fly

ERH6 98.50/98.25/97.75p fly bought 2.75 in 5k.

EQUITIES: Equities Have Stabilised After Pre-London Sell Off

Global equity benchmarks are off the session lows that were registered during the Asia-London handover.

- We noted at the time that there was no clear driver for the sell off, with the move initially starting in Chinese & HK equities, before spilling over into e-minis and European equity index futures.

- The moves weren’t huge in scale but were fairly swift.

- We still haven’t tracked down a major headline driver, with some suggesting that optimism surrounding Sino-U.S. trade talks had faded a little.

- Late Monday comments out of the U.S. were relatively positive, with talks set to recommence at 10:00 London.

- While there hasn’t been any official communique out of China, Chinese state broadcaster CCTV noted that “the U.S. should realistically view the progress made and revoke negative measures against China.” CCTV also noted that Beijing is “earnest” when it comes to the trade talks.

- Note that story was published a few hours ahead of the sell off and was seemingly used retroactively to explain a market move that lacked a clear fundamental driver (although it may have had a lagged impact given the Chinese & HK market lunch breaks).

- The moves underscore wider sensitivity to any swings in Chinese sentiment during times of elevated global trade uncertainty.

- European equity futures have bounced, with e-minis stabilising, while China & HK equity benchmarks ticked away from lows.

SWEDEN: Riksbank Business Survey Screens Dovish, Limited FX Impact For Now

The Riksbank Business Survey screens dovish at first glance. The activity signals highlight downside risks to demand, largely stemming from trade-related uncertainty. Although businesses selling to households are planning to increase their prices, the key excerpt (which is not in the press release, only the full report) is that "they are not planning to raise prices more or more often than normal".

- The survey appears to support market pricing that implies a near-80% implied probability of a June cut.

- NOKSEK is moving back to fresh session lows at typing, but this appears to be a function of latest NOK weakness, rather than a SEK move.

Highlights from the report:

- "The economic situation has weakened during the spring, and companies’ view of the economic outlook for the coming months has become significantly gloomier"...."The more pessimistic view is mainly linked to the increased trade policy tensions and the uncertainty they are creating. Companies are concerned that global economic activity will slow down and negatively affect demand in the period ahead."

- "Industrial activity is weak and has deteriorated during the spring. The uncertainty is making customers hold off on purchases and investments, which is making manufacturing companies particularly negative about the development of the economy"....."

- "In retail trade, companies state that the economic situation is generally satisfactory and several have noticed that sales volumes have increased during the spring"...."Some argue that households have already become cautious, while others see it as a risk that has not yet materialised. The restaurant industry is one of those that have already seen effects on sales."

- "Companies selling to households are planning to increase their prices, above all due to increased purchasing costs. "..."The extent to which selling prices can be increased will largely depend on the development of demand and competition and how competitors act. Overall, they are not planning to raise prices more or more often than normal."

- "Among business-to-business sellers, fewer than before are planning to increase prices over the next year. In particular, weaker demand will make it more difficult to raise them."

- "The majority of companies state that they have been affected by the import tariffs introduced, most of them to a small extent. However, the different announcements on tariffs are creating an unpredictability that is making customers more cautious and companies’ planning more difficult."