EM ASIA CREDIT: MNI EM Credit Market Update - Asia

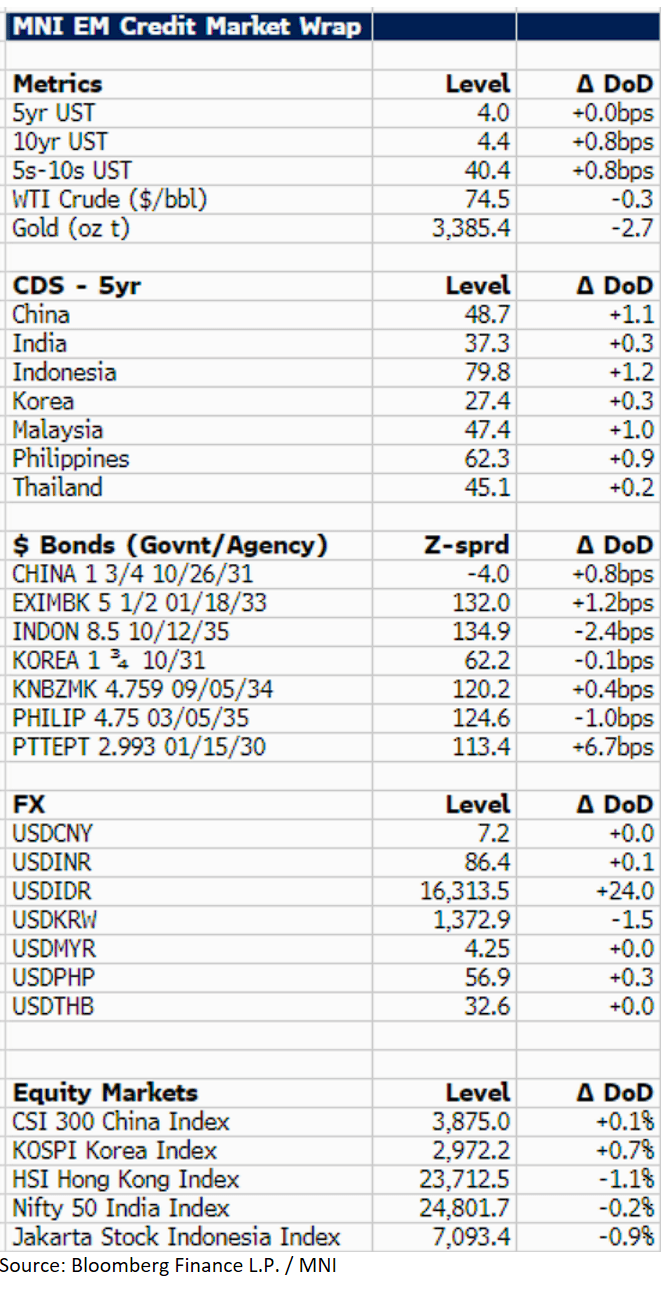

U.S. 10y treasury yields are currently 1bp higher at 4.4% with markets weighing up the possibility of broader U.S. involvement the Middle East, with no clear direction.

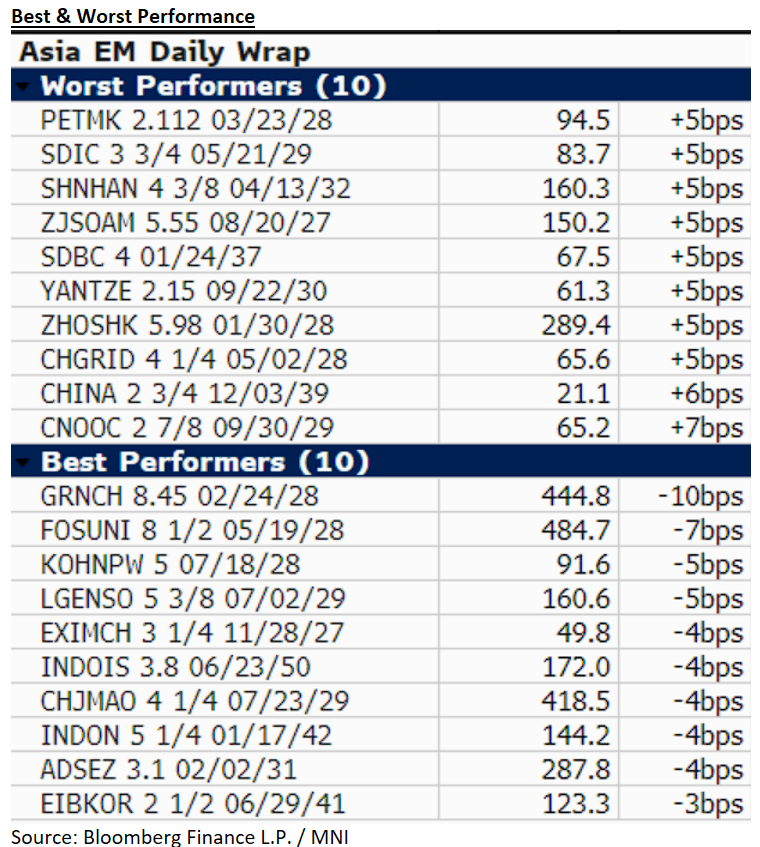

We followed LATAM where prices exhibited little movement, failing to capture the rally in U.S. Treasuries, and resulting in a widening of credit spreads. In Asia EM, $ credit was a bit of a mixed bag, with govie/agency $ spreads in a +1/-1 range, the outlier being Thailand (PTTEPT 01/30 +7bp), which continues to underperform the last few sessions. Thailand reports that its U.S. trade proposal will be submitted on the 30th June.

In terms of credit, we have seen rating affirmations on Bank Tabungan Negara (Moody's) and Perusahaan Listrik Negara (Fitch), both issuers have previously mandated $ deals that have not yet come to the market. In addition, Vedanta sold shares in Hindustan Zinc, with proceeds to be used to deleverage.

Finally, we have a $ 3y mandate for Chinese State backed tourism company, Huangshan Tourism Group, as well as a Republic of Korea new € mandate (3y, 7y).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EU-UK: Deal Reached Ahead Of Leaders' Summit

The UK's Minister for EU Relations, Nick Thomas-Symonds, confirms that a deal has been reached with the EU ahead of the EU-UK Summit taking place later today. Reports in the past hour suggested the EU and UK have reached a deal on fisheries that will allow a broader agreement to be signed at today's UK-EU summit. Chris Mason at the BBC writes "A 12-year deal has been done on fishing access for EU boats into UK waters, which will no doubt prompt a big row. The government will argue it has secured improved trading rights for food and agricultural products into the European Union. A defence and security pact will be central to the deal set out in a few hours. Both sides will emphasise the shared desire for deepening cooperation."

- Joe Barnes at The Telegraph posts on X regarding detail of the deal: "Brexit reset deal - Fishing access until 2038. SPS, no time limits on dynamic alignment

[carbon border adjustment mechanism] and [emissions trading scheme] is dynamic alignment. No youth mobility deal, but a promise to revisit at a later under agreed parameters, including rejoining Erasmus." - In terms of today's schedule, UK PM Sir Keir Starmer and other gov't ministers meet with European Commission President Ursula von der Leyen, Council President Antonio Costa and others at Lancaster House in London at 1015BST (0515ET, 1115CET). At 1230BST (0730ET, 1330CET), Starmer, VdL and Costa will hold a press conference, while a ministerial statement on the agreement will be delivered in the House of Commons after 1530BST.

EGBS: J.P.Morgan Recommends 3s/10s BTP Steepener Boxed Vs. Germany

J.P.Morgan have recommended entering 3s/10s BTP steepeners boxed vs. Germany as a “low beta proxy for an underweight BTP position”.

- They note that after the recent 10-Year BTP tightening vs. Germany the spread “is now trading at levels last seen late 2021 when Mario Draghi was the Prime Minister of Italy, and ECB APP and PEPP net purchases were still ongoing. We find Italian spreads expensive on our fundamental fair value framework and also cross-market vs. Euro credit markets.”

GILTS: Selling Off & Steepening Alongside Tsys

Futures trade as low as 91.20 at the open, comfortably through Friday’s late lows, extending on the downtick that was seen ahead of the weekend (the contract closed Friday’s opening gap higher late in the same session).

- Spillover from weakness in Tsys is the primary driver here, after Moody’s downgraded their U.S. sovereign credit rating by one notch late on Friday.

- Initial support of note located at the May 14 low/bear trigger (90.96), with bears remaining in technical control.

- Initial resistance located at Friday’s high (92.03).

- Yields 1-5bp higher, curve steeper.

- 2s10s still ~12bp shy of cycle closing highs, last ~67bp.

- 5s30s ~11bp below closing cycle highs, last ~127.7bp.

- GBP STIRs hovering around pre-gilt open levels.

- SONIA futures flat to -4.0, BoE-dated OIS showing 42.5bp of cuts through year-end.

- Late Friday saw BoE Deputy Governor Deputy Governor Lombardelli note that the Bank is overhauling its communication methods via a shift away from its main inflation forecast toward multiple scenarios. Not market moving.

- Wednesday’s CPI data headlines the UK calendar this week. We have written a little on that in our global week ahead/late Friday bullets, expect more in our full preview.