EM ASIA CREDIT: MNI EM Credit Market Update - Asia

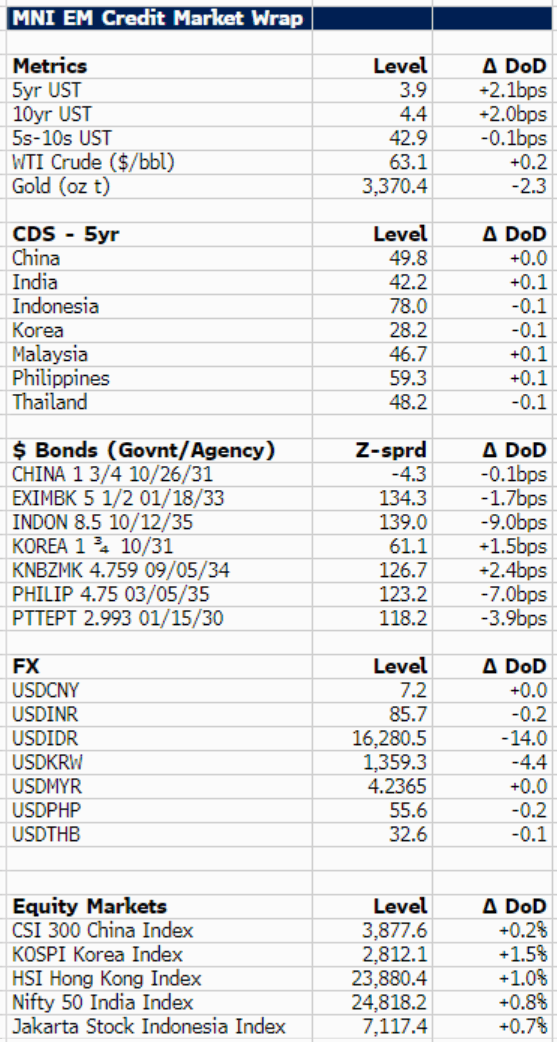

U.S. 10yr Treasury yields are 1bp higher 4.4%, with China ramping up concerns about U.S metal tariffs and the impact on supply chains. Overnight in LATAM, we saw spreads trending wider with low beta moving out about 1-2 bps while higher beta names widened by about 5bps. Pemex outperformed again amid reports that the Mexican government can engineer a turnaround for the troubled energy company.

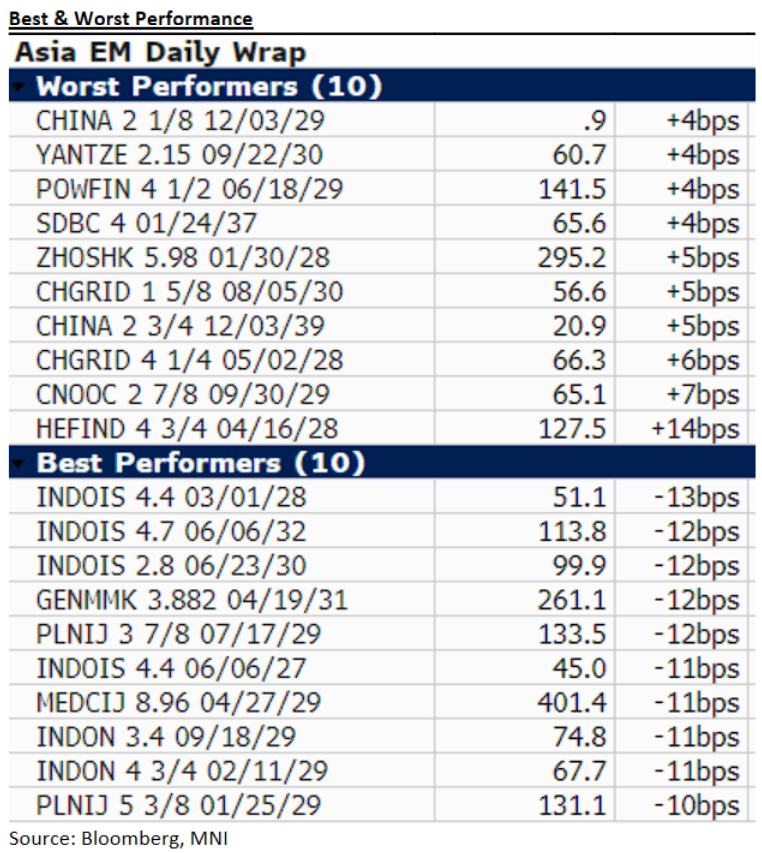

In Asia, EM credit is mostly better with govie/agency $ spreads up to 9bp tighter. The outperformers being Indonesia, whose trade delegation goes to the U.S. next week, -9bp tighter ($ 10/35). Also the Philippines, which released inflation data in line with consensus, is -7bp tighter on the day ($ 3/35).

In terms of news flow, we see a new $2bn debt program from Thai Bev, a dollar deal would be a debut if it comes. Also, Czech courts have lifted the ban on signing a nuclear reactor deal with Korea Hydro & Nuclear Power. No new issues or mandates for now.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SNB: Schlegel Acknowledges CHF Strength - Media

The Swiss Franc has appreciated 'really a lot', SNB Chairman Schlegel said this morning in Zurich according to media reports.

- Chairman Schlegel is usually not known for such pronounced commentary on CHF valuations.

- That follows CHF REER having temporarily peaked to highest levels since end-2023 in the last weeks - Schlegel also highlights again they 'intervene in FX as needed' - that is in line with previous rhetoric.

- There was no indication of recent material SNB intervention apparent in domestic sight deposit data.

- Swiss April CPI yesterday came in 0.2pp below consensus at 0.0% Y/Y, markets now price about a 1/3 chance of an outsized 50bp cut to -0.25% at the June SNB meeting.

HONG KONG: HKMA Diversifies Away From USD, Reduces UST Duration in Holdings

HKMA chief Eddie Yue states that the HKMA Exchange Fund has been reducing duration in UST holdings, and has been diversifying into non-US assets. They also note they've been diversifying their FX exposure across the investment portfolio in order to manage risks.

HKMA's Exchange Fund holds assets totalling HKD 4trl ($525bln) as of end-2024, of which over half is 'Debt Securities', in which USTs would likely be the bulk of the category. HKMA's Exchange Fund has an objective of ensuring the "entire Monetary Base, at all times, is fully backed by highly liquid US dollar-denominated assets" as well as ensuring "sufficient liquidity for the purpose of maintaining monetary and financial stability".

- As such, any shifts to the duration of their UST holdings is likely made to keep HKMA's investment objectives on track, particularly as the USD/HKD trading band errs toward the strong-side - triggering HKD selling by the HKMA on both Friday and Monday.

ITALY DATA: Stronger-than-expected April Services PMI, But Export Demand Soft

The Italian services PMI was 52.9 in April, above the 51.3 expected and 52.0 prior. It’s broadly back in line with February’s 53.0 reading, allowing the PMI to remain in expansionary territory for the fifth month. Despite this, the latest flash national accounts suggested the services industry made no contribution to sequential value-added growth in Q1.

The press release suggests further weakness in export demand, usually an important source of Italian growth.

Key notes from the release:

- “Where panellists reported increased activity levels, they typically linked this to greater inflows of new work and recent new customer intakes”….“ According to survey respondents, there were various factors driving the improvement, namely new project wins, recent customer onboarding and a general boost in demand for services”.

- “Meanwhile, there was a ninth consecutive monthly drop in new work from abroad in April. International sales were reportedly limited by weakness in key export markets.”.

- “Services firms in Italy continued to hire additional staff in April”.

- “Reflective of increased purchasing prices, as well as greater staff and energy related costs, there was a further rise in overall operating expenses”…“ Although average charges rose again in April, there was a loss of momentum as the rate of inflation cooled to its weakest in the year-to-date”.

- “Looking ahead, increased levels of uncertainty and concerns towards the economic climate weighed of firms' expectations regarding activity over the coming 12 months”.