EM ASIA CREDIT: MNI EM Credit Market Update - Asia

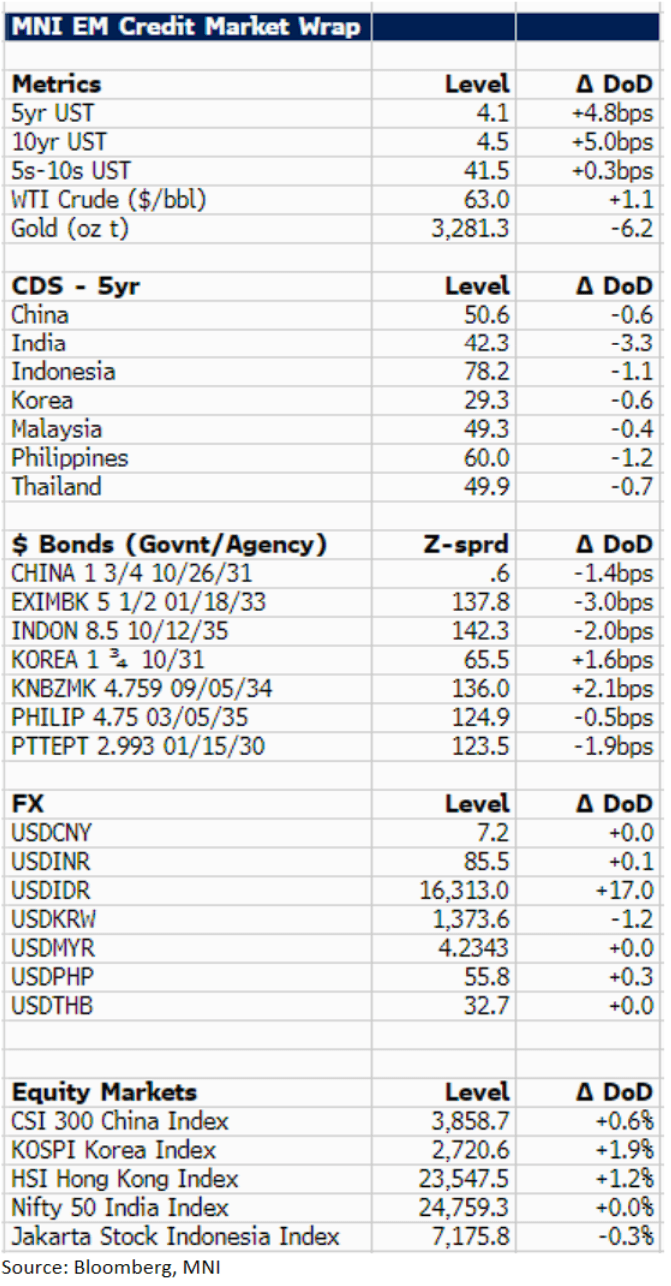

U.S. 10y treasury yields are 5bp higher today at 4.5%. Asia EM credit is mostly better on the day, with govie/agency $ spreads up to 3bp tighter. Our India proxy (EXIMBK 01/33) outperforming and 3bp tighter. We note India's April industrial output released yesterday (+2.7% YoY) was higher than expectations (+1%). South Korea, as expected cuts rates 25bp today to 2.5%. Asia equities also up on the day, with the Korean KOSPI index outperforming (+2%).

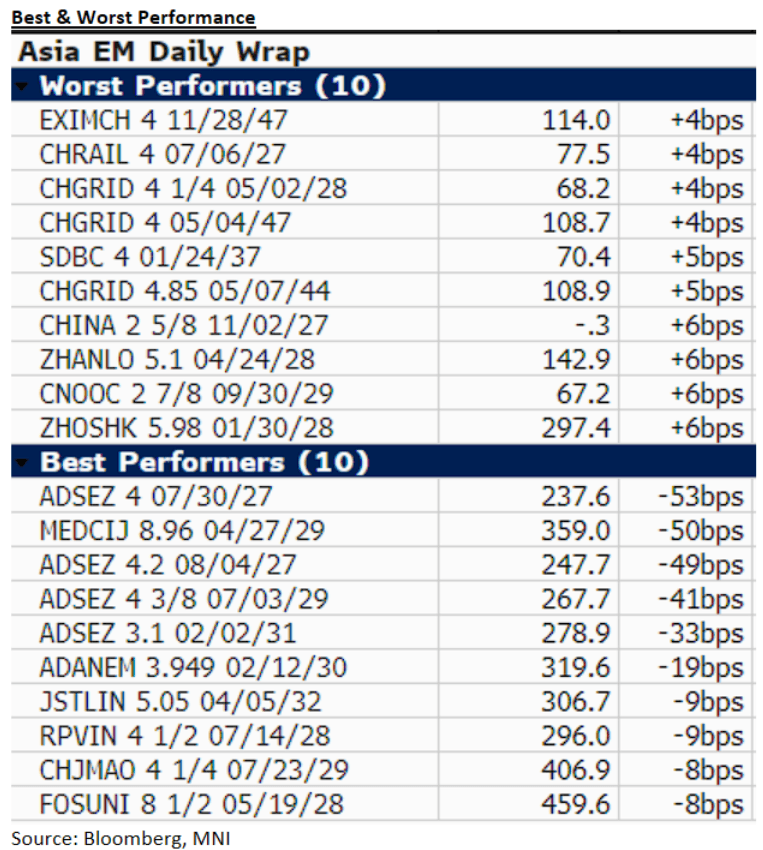

In the corporate space, Adani Ports notified the market of possible $ bond buybacks, bonds higher on the back of the news ($ 7/27s -53bp). Also Bloomberg is reporting that Reliance Industries has interest in BP's Castrol divestiture. Not particularly surprising. In terms of new issuance, we have the Guangxi Communications $benchmark 3y deal with an IPT of 5.2% area. We estimated fair value at 4.8%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGBS: Citi: EGB Spread Performance Looks Overdone, Keep BTP/OAT Wideners

Citi note that “last week’s de-escalation of trade wars and the reversal of threats against Powell helped tighten EGB spreads back to pre-‘Liberation Day’ levels”.

- Drilling down, they observe that “during this move, BTP/Bund has been better correlated with the top-left vol, outperforming vs. other euro risk assets (EUR equities/credit). This perhaps suggests a belief that the economic implications of tariffs for BTPs might be completely offset by additional ECB rate cuts and any substitution out of USD assets".

- However, they warn that “equities are now catching up and the residual of BTP/Bund on our fair value model has started to reverse its richness”.

- As a result, they suggest that “the next BTP move from here might be underperformance that is historically more consistent with these residual levels”.

- They conclude that “that BTP shorts are perhaps still an attractive hedge against any resurgence in tariff risks compared to the BBB corporate credit which might be better suited to position for further de-escalation. Therefore, we continue to hold onto our 10-Year BTP/OAT widener”.

EURIBOR OPTIONS: Call spread vs put spread

ERU5 98.50/98.625cs vs 97.9375/97.8125ps, bought the cs for 0.75 in 5k.

GILTS: Firmer, Recent Ranges Intact

Gilts initially firm given the continued move lower in crude oil futures, although moves away from session highs in core global FI peers limit the rally.

- Futures stick within yesterday’s range, trading as high as 93.25 before fading back to 93.10 last.

- Initial support and resistance located at 92.20/93.34, recent bullish technical theme remains intact.

- Yields ~1.5bp lower across the curve.

- 10s below 4.50%, with yield support located at 4.460% still untested.

- Spread to Bunds remain pinned around 200bp after the pullback from April highs (218.8bp), the April 8 closing level (197.4bp) remains intact.

- GBP STIRs still around levels flagged ahead of the gilt open, showing ~90bp of cuts through year end.

- On the supply front, the DMO will come to market with GBP900mln of the 1.25% Nov-54 I/L line this morning.

- The only previous auction of the line came in January, with a slightly larger auction size of GBP1.0bln. A decent bid-to-cover of 3.06x was seen at the prior auction. Demand will be watched closely at this auction as it is the first long-dated linker auction since the U.S. tariffs were implemented.