BSP: MNI BSP Preview - Oct 2025: On Hold But May Ease In Dec

Oct-08 01:41

- The consensus for tomorrow’s BSP meeting outcome is no change from the current 5.00% policy rate. Still, some sell-side expect a 25bps cut, with 6 out of the 25 economists surveyed by Bloomberg forecasting such a move (the remainder see rates holding steady). We sit in the no change camp, although note it may be a reasonably close call between this and a further 25bps cut.

- From an inflation standpoint, yesterday’s update for September didn’t materially change the outlook (BSP said as much after the data printed). Given this broadly unchanged backdrop and the fact that BSP Governor Remolona turned a little less dovish at the last policy meeting, it doesn’t point to a compelling case to ease from an inflation standpoint.

- Whilst downside growth risks may argue for a cut, fresh USD/PHP gains following a further BSP cut, could be an unwelcome development for the BSP. Additionally, the central bank gets an important Q3 GDP update on Nov 7, which comes ahead of the Dec BSP meeting. Hence the central bank may wait to assess growth trends at that meeting (with a window to cut), particularly given a broadly unchanged inflation backdrop in recent months.

- See the full preview at this link:

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

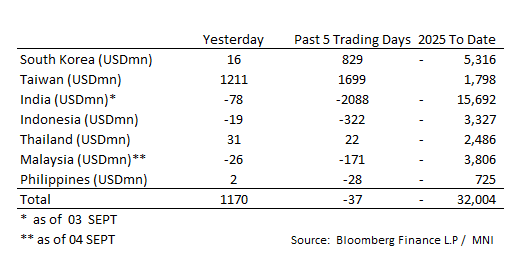

ASIA STOCKS: Equity Flow Update for Major Regional Bourses

Sep-08 01:40

Taiwan has had its largest inflow in a month.

- South Korea: Recorded inflows of +$16m as of Friday, bringing the 5-day total to +$829m. 2025 to date flows are -$5,316m. The 5-day average is +$166m, the 20-day average is -$13m and the 100-day average of +$62m.

- Taiwan: Had inflows of +$1,211m yesterday, with total inflows of +$1,699 m over the past 5 days. YTD flows are positive at +$1,798m. The 5-day average is +$340m, the 20-day average of -$139m and the 100-day average of +$209m.

- India: Had outflows of -$78m as of the 3rd, with total outflows of -$2,088m over the past 5 days. YTD flows are negative -$15,692m. The 5-day average is -$418m, the 20-day average of -$215m and the 100-day average of -$3m.

- Indonesia: Had outflows of -$19m as of the 3rd, with total outflows of -$322m over the prior five days. YTD flows are negative -$3,327m. The 5-day average is -$64m, the 20-day average +$21m and the 100-day average -$13m.

- Thailand: Recorded inflows of +$31m Friday, with inflows totaling +$22m over the past 5 days. YTD flows are negative at -$2,486m. The 5-day average is +$4m, the 20-day average of -$40m and the 100-day average of -$14m.

- Malaysia: Recorded outflows as of the 4th of -$26m, totaling -$171m over the past 5 days. YTD flows are negative at -$3,806m. The 5-day average is -$34m, the 20-day average of -$34m and the 100-day average of -$11m.

- Philippines: Recorded inflows of +$2m Friday, with net outflows of -$28m over the past 5 days. YTD flows are negative at -$725m. The 5-day average is -$6m, the 20-day average of -$5m the 100-day average of -$4m.

AUSTRALIA: Survey Data Focus Of This Week

Sep-08 01:28

Survey data are released this week and there is not much else. They will be important to gauge if the economic recovery continued in Q3 and how price pressures evolved.

- Tuesday sees September Westpac consumer confidence which rose each of the four months to August helped by lower rates and the prospects of further RBA easing. At 98.5 last month, it is now approaching the neutral 100-level.

- The NAB August business survey is also out on Tuesday. Business confidence has been trending higher since March and is positive again. Conditions however remain soft, although June/July printed above the 2025 average. Employment and cost/price components will be monitored closely.

- Melbourne Institute consumer inflation expectations for September are released on Thursday. It moderated substantially to 3.9% in August but the 3-month average has been around 4.5% since June.

- The RBA’s head of payments policy Connolly will participate in a panel on Thursday at 1130 AEST and assistant governor (financial system) Jones on Friday at 1200 AEST.

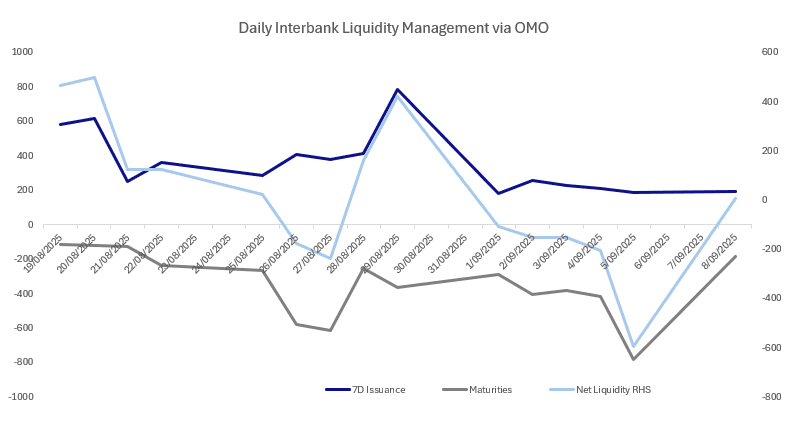

CHINA: Central Bank Injects CNY8.8bn via OMO

Sep-08 01:28

- The PBOC issued CNY191.5bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY182.7bn.

- Net liquidity injects CNY8.8bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.41%, from prior close of 1.43%.

- The China overnight interbank repo rate is at 1.31%, from the prior close of 1.30%.

- The China 7-day interbank repo rate is at 1.50%, from the prior close of 1.45%.