BOE: MNI ANALYSIS: BOE September APF Decision: What you need to know

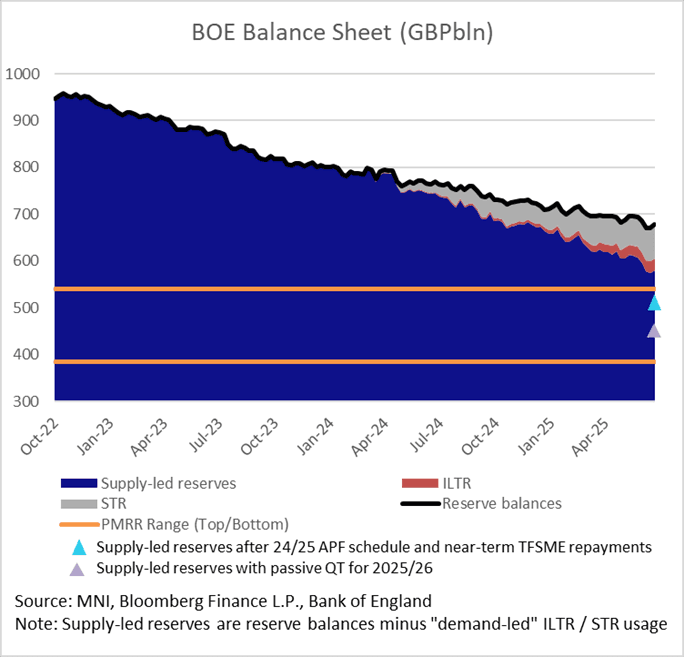

- We think that the market is looking at the wrong measure of reserves when discussing the BOE’s September APF decision: we think that supply-led reserves are much more important than total reserves.

- Supply-led reserves will fall below the top of the preferred minimum range of reserves (PMRR) when taking into account QT for the current period (to Sep25) and TFSME repayments (to Oct 25).

- Even with just passive QT from Oct25-Sep26, supply-led reserves will fall to the middle of the PMRR range.

- We outline the fiscal costs of QT (which are huge).

- At present we think the best decision for QT in the year ahead would be to continue active sales at broadly the same pace as in the current year.

- We also set out in our appendices the main components of the Bank’s balance sheet and how the repo operations work

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US ISM MAY SERVICES COMPOSITE INDEX 49.9

- MNI: US ISM MAY SERVICES COMPOSITE INDEX 49.9

- US ISM MAY SERVICES PRICES 68.7

BOC: Little Shift In Cut Pricing Post-Decision, Despite Subtle Hawkish Shifts

A slight shift in implied market pricing for further 2025 BOC cuts after the decision to hold but basically unchanged despite the decent implied probability of a cut today from 2.75%.

- Cumulative pricing through the July meeting points to 13+bp of cuts through that point (2.61% implied OIS rate, vs 2.59% just before the decision). September retains the first full cumulative cut pricing (2.50%, roughly unchanged vs pre-decision), with end-year rates at 2.37% (unch vs pre-decision).

- The communications kept the door open to a cut but not emphatically (Gov Macklem's opening statment: "We also discussed the path ahead for the policy interest rate. Here, there was more diversity of views. On balance, members thought there could be a need for a reduction in the policy rate if the economy weakens in the face of continued US tariffs and uncertainty, and cost pressures on inflation are contained.")

- And of note, the statement language removed the reference from the prior statement that it could "act decisively" if the economy clearly moved in one direction. And Gov Macklem's commentary includes this note in inflation ("There is some unusual volatility in inflation, but these measures suggest underlying inflation could be firmer than we thought.")

- Expect Macklem to be asked about these seemingly hawkish - or at least less dovish - shifts in the press conference.

- The policy statement sums it up: "With uncertainty about US tariffs still high, the Canadian economy softer but not sharply weaker, and some unexpected firmness in recent inflation data, Governing Council decided to hold the policy rate as we gain more information on US trade policy and its impacts. We will continue to assess the timing and strength of both the downward pressures on inflation from a weaker economy and the upward pressures on inflation from higher costs."

US DATA: Strong Upward Revision To Final May Service PMI

The S&P Global US final service PMI saw a surprisingly strong upward revision for May, implying a strong improvement in activity late in the month. The press release reiterated the strongest output price inflation since Aug 2022 as firms passed on cost increases.

- S&P Global US services PMI: 53.7 (cons & flash 52.3) in May final after 50.8 in April. The 2.9pt increase unwinds much of the 3.6pt drop in April and leaves it close to the 54.3 averaged in 2024 for quick context.

- S&P Global US composite PMI: 53.0 (cons & flash 52.1) in May final after 50.6 in April. This composite averaged 53.7 in 2024 for a pre-Trump administration comparison.

The press release confirmed the steepest increase in output charges since Aug 2022, something mentioned in the flash release. The survey period was extended from May 12-21 in the flash to May 12-28, implying a marked improvement in activity late in the month. Press release highlights (with the full report found here):

- “Concurrent upturns in US service sector activity and new business growth were signaled in May, according to the latest PMI® data from S&P Global.

- Confidence in the outlook also strengthened, whilst firms took on additional staff to a greater degree. However, growth in employment was insufficient to prevent a solid rise in work outstanding.

- Rising backlogs in part reflected delays in the delivery of ordered equipment due to tariffs, which also drove up cost inflation to its highest in nearly two years. Increased costs were passed on to clients via the steepest increase in output charges since August 2022.”

Further details on the higher input cost inflation: “Meanwhile, tariffs and suppliers generally raising their prices meant input cost inflation accelerated steeply in May to its highest since June 2023. Wages were also reported to be factor pushing up overall operating expenses.