US DATA: Mixed Household Survey, Highest Unrounded Unemp Rate Since Oct 2021

Jun-06 13:15

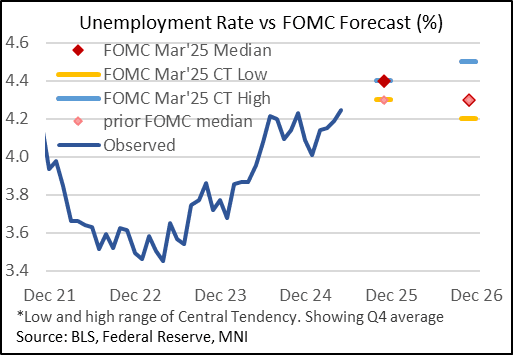

The main standout statistic from May's Household Survey is the tick up in the unemployment rate to 4.244% from 4.187%, which while keeping the rate at 4.2% in line with consensus suggested that upward pressure on the rate continues. Indeed most statistics underlying the unemployment rate largely pointed to steady weakening in the labor market, though the report was mixed overall.

- This was the highest unrounded unemployment rate since October 2021, has been ticking up 0.06pp monthly on average the last 4 months, which is more or less the steady but not rapid deterioration envisaged by the Fed (4.4% median forecast for Q4). In turn the number of unemployed rose 71k to the highest since October 2021 (7,237k).

- The pullback in the size of the labor force - the denominator in the unemployment calculation - was notable and a possible sign of weakness, dropping 625k, the most in 17 months, leaving the employment to population ratio at - 59.72% the lowest on an unrounded basis since January 2022.

- And the participation rate at 62.37% was the lowest since December 2022, with both prime-age (25-54) and 55+ participation dropping 0.2pp, and 16-24 participation plummeting 0.8pp to a 9-month low 55.5%. The number of people not in the labor force rose 813k, a 4-month high (SA).

- The breakdown of the unemployed showed mixed signs. Permanent job losers were steady at 1.92M, leaving the rate at 1.12% and suggesting that ongoing deterioration has stalled a little.

- Job losers increased only 2k, and re-entrants rose for the 4th month in 5 at 53k. Across unemployment categories the only standout was in the "job leavers" category which fell 151k, the most in 38 months - the rate of job leavers is at a 4-year low, a sign of labor market softness.

- Household Survey employment fell 696k, erasing the previous two months' gains, and again contrasting with Establishment survey gains.

- The month saw 108k in those not at work due to bad weather - an unusually high number for May (the prior 3 years averaged 32k).

- The underemployment (U-6) rate was steady at 7.8%. Those working part-time for economic reasons, a rise in which is typically considered a sign of weakness, dipped for a 2nd consecutive month (66k after 90k) to a 4-month low.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: Stoxx600 call buyer

May-07 13:13

SXXP (20th June) 557.5c, bought for 1.6 and 1.7 in ~15k.

ITALY DATA: Weak Retail Sales Momentum Suggests Consumption Drag In Q1

May-07 13:13

Weak Italian retail sales momentum suggests sequential quarterly household consumption growth was tepid - possibly negative – in Q1.

- March nominal retail sales fell 0.5% in March. The three analysts submitting forecasts for the print were between +0.1 and +0.3%. Real sales were also -0.5% M/M, the fifth negative sequential print in the last six months. That dragged 3m/3m growth down to -0.59% (vs -0.42% prior).

- ISTAT retailer confidence has been expansionary throughout the last 3 years, but momentum has been waning in 2025.

- Although the Q1 flash GDP report indicated that domestic demand made a positive contribution to growth, a detailed split across expenditure component was not available.

CROSS ASSET: Estoxx Futures closes the Gap, Bund test a new high

May-07 13:09

- Estoxx futures has now closed the Opening gap down to 5209.00, not a Tech level.

- This latest push lower helps Bund print a new intraday high, but no real trigger for the move, mostly some order related flow, and a continuation since Bond went bid post the French Auctions this Morning.

- Support in VGM5 is at 5178.00, this is only Yesterday's low.

Trending Top

Jun-26 16:22