EM LATAM CREDIT: Marfrig: Uruguay Plant Sale to Minerva Cancelled - Neutral

(MRFGBZ; Ba2/BB+/BB+) (BEEFBZ; NR/BB/BB) "Marfrig Says Unable to Complete Sale of Uruguay Units to ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC JUST STARTING TO SEE TARIFF EFFECT ON INFLATION

- BOC JUST STARTING TO SEE TARIFF EFFECT ON INFLATION

- GOVERNOR MACKLEM SAYS ELEVATED TREND CPI HAS HIS ATTENTION

US-RUSSIA: Republican Leader Thune Says Senate Ready To Act On Russia Sanctions

Senate Majority Leader John Thune (R-SD) told Fox News that the Senate is "prepared to move on the Russia sanctions bill if required", after President Donald Trump threatened new penalties on Russia within 10 days, if Moscow fails to take steps towards securing a ceasefire with Ukraine.

- Trump told reporters: “I don’t know if it’s going to affect Russia, because [Russian President Vladimir Putin] wants to [...] keep the war going. But we’re going to put on tariffs and the various things you put on. It may or may not affect them. But it could.”

- With the House on recess until September 2 and the Senate expected to follow on Friday, Trump is likely to pursue any potential new sanctions or tariffs via executive action.

- The most powerful tool available to Trump is secondary tariffs on buyers of Russian oil and gas products, this would fall heavily on China, India, Turkey, and Brazil. However, considering challenging trade talks with China, India, and Brazil, Trump may choose to avoid measures that could undermine negotiations.

- The baseline scenario is that Trump's actions, if they come, would target Russian O&G, but fall below the punitive level in Senator Lindsay Graham's (R-SC) 'Sanctioning Russia Act'.

- Trump's Truth Social post earlier, threatening tariffs on India, specifically flagged New Delhi's purchase of Russian oil and military hardware, suggesting that one possible option could target India, while providing a temporary carveout for China during the tariff and export control truce.

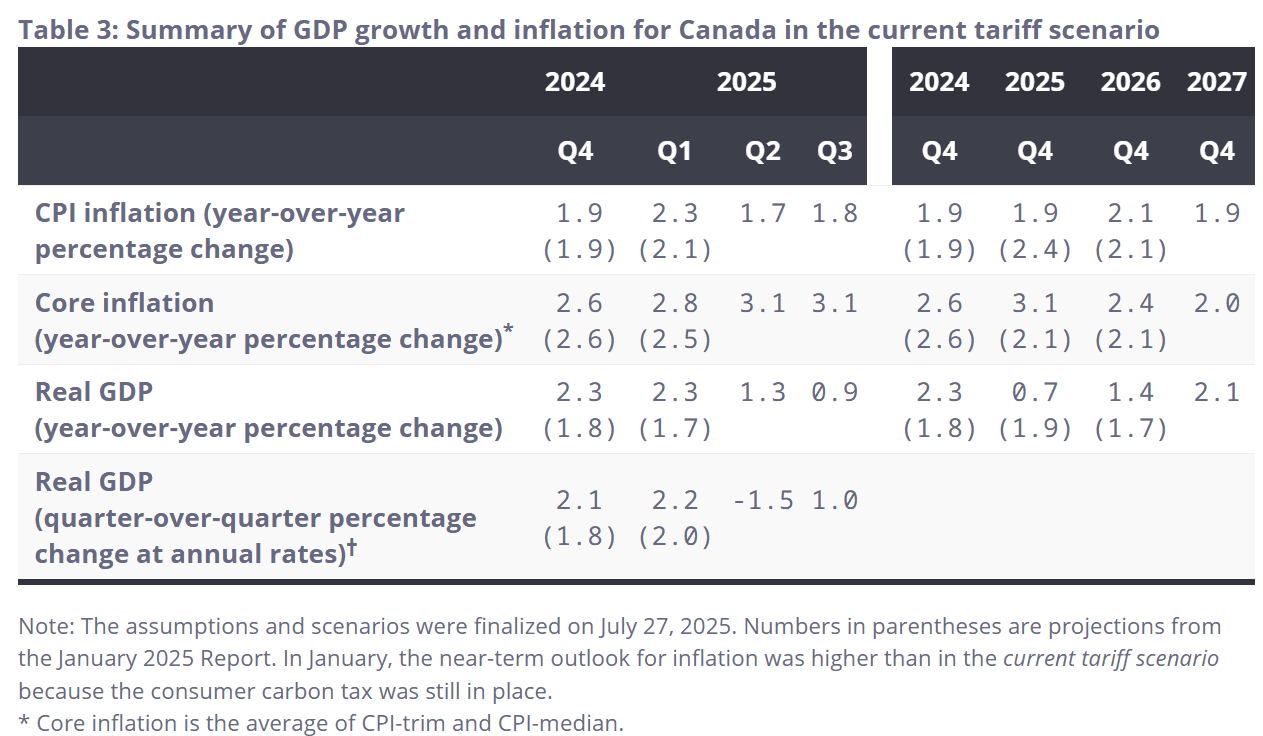

BOC: Latest MPR Projections Increasingly Pessimistic On Growth

In something of a surprise, the BOC's July Monetary Policy Report (MPR) (link) provides three scenarios for its quarterly forecasts, up from two in April's edition and one central forecast most of the time. A "current tariff scenario instead of a base-case projection" and "two alternative scenarios are also presented that, when taken together, encompass a range of potential outcomes". Most attention will be paid to the current tariff scenario though this doesn't appear to incorporate a threatened 35% US tariff as of Aug 1.

- The figures in the latest tables compare the current central outlook to that seen in January's MPR, as opposed to the dual April scenarios. If compared with the April scenarios, July's current-policy CPI forecasts look a lot more like the "less pessimistic" scenario, but the GDP forecasts look relatively pessimistic.

- As noted in the report, in the current tariff scenario "GDP growth picks up in the second half of 2025 as exports stabilize. GDP growth then strengthens to reach 1.8% in 2027, but tariffs permanently lower the path of economic activity. Slow population growth and weak business investment weigh on potential output growth in the second half of 2025. Potential output growth then picks up in 2026 and 2027, mainly due to more robust trend labour productivity growth. Trend labour input growth remains modest. The output gap persists in 2026 and then narrows in 2027 as GDP growth picks up."

- For inflation in the near term, factors include "the end of the downward impact from the elimination of the consumer carbon tax in the second quarter of 2026 Canada’s counter-tariffs, which add up to 0.6 percentage points to inflation, particularly affecting the prices of goods such as food and motor vehicles", offset by "excess supply and slower growth in unit labour costs easing inflation in shelter prices, reflecting slower growth in rent prices and mortgage interest costs the recent appreciation of the Canadian dollar. In 2027, inflation remains close to 2% as the effects of tariffs dissipate and excess supply begins to shrink. The composition of inflation shifts, with inflation in goods prices easing and inflation in services prices stabilizing near historical norms."

- Looking at the forecast tables, consistent with the latest CPI data for June, headline Y/Y inflation is seen remaining under 2% through end-2025 (1.7% Q2, 1.8% Q3, 1.9% Q4). and remaining well-behaved at around 2% through the 2027 forecast horizon. However, core inflation (average of the trim and median measures) is seen remaining above 3% (3.1% in Q2, Q3, and Q4) before subsiding in 2026 and 2027 to 2%.

- Compare this to the April MPR in which the average of the 2 scenarios' Q2 CPI was seen at 1.5% with core at 2.95%, with headline CPI coming down to an average 2.35% in 2026 and 2.05% in 2027.

- But the GDP expectation for Q2 at -1.5% (Q/Q SAAR) is even worse than the downside scenario in April, which was -1.3% (the less pessimistic scenario showed 0.0%). There's a rebound anticipated to 1.0% for Q3. On a Y/Y basis, real GDP is seen pulling back from 1.3% in Q2, to 0.9% in Q3, and 0.7% in Q4, with only a very modest rebound to 1.4% by Q4 2026.