BOC: Macklem: Expect Second Quarter Will Be Weak

BOC Governor Macklem speaking in the post-G7 meeting press conference reiterated the "uncertainty" theme in setting policy. In his first commentary after this week's hotter-than-expected April CPI report, Macklem sounded if anything a little more focused on growth than inflation. Though that should be taken in the context of national accounts data coming out next week, and he's already putting focus on Q2 rather than the forthcoming Q1 reading.

- He said that central banks need to carefully balance higher inflation vs weaker growth amid tariff-related uncertainty. But "the more we can get uncertainty down, the more we can be more forward looking...as we move forward in our monetary policy decisions".

- Macklem noted we'd get GDP data next week: he noted that exports and inventories boosted Q1 GDP, but consumption and business investment "in particular" would be weaker. And "I expect the second quarter will be quite a bit weaker" as a consequence of pulling forward exports and inventory accumulation. "Where we go from there depends on what happens with tariffs", with prolonged US-Canada trade war uncertainty holding back growth.

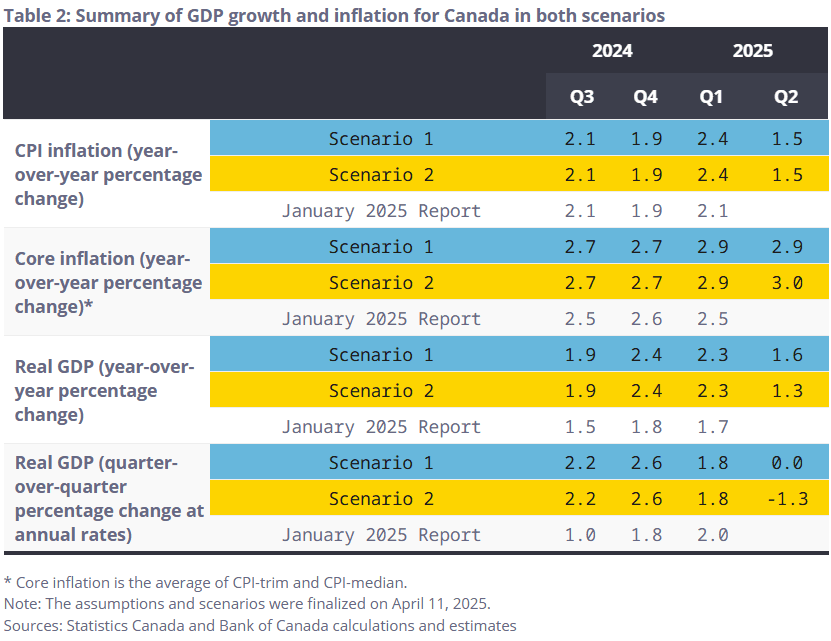

- That seemingly pessimistic appraisal shouldn't be a surprise. The BOC's two scenarios in the April MPR both track Q1 GDP growth at 1.8% Q/Q annualized, with the more benign scenario for Q2 seeing 0.0% growth, with the more negative scenario -1.3%.

- As we noted earlier, consensus for next week's growth figures (per BBG) is for a +1.8% Q/Q annualized GDP reading in Q1 (in line with the BoC's April estimate, and vs +1.5% flash), swiftly followed by -0.5% in Q2 and 0.0% in Q3, effectively teetering on the edge of technical recession. The monthly figure for March GDP will be closely eyed for momentum (flash was 0.1% growth after -0.2% Feb and +0.4% Jan).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

TARIFFS: Little Concrete Progress Evident In Major Deals; Bessent Speaks Weds

Fox's @CGasparino on X.com has an account of Tsy Sec Bessent's comments on a China trade deal that sound closer to the Reuters version of events ("a slog" to get a deal) moreso than Bloomberg's (which reported that he expected the situation to de-escalate):

- "BREAKING: Ive been told by a person close to @SecScottBessent the reports on his remarks about a trade deal with China have being imminent overstate what he said. He meant that there is room for talks and de-escalation but much also depends on China's willingness to compromise on trade as well."

- Gasparino follows this up by reporting that "Bessent & Co scrambling to reach deals with India, South Korea, Japan, Australia; deals said not to be imminent". Recall that Gasparino reported Monday that "Japanese negotiators are complaining that the problem with the trade negotiations with the White House, what's delaying concrete progress and a real deal, is that US keeps changing its ask in terms of exactly what it wants, said one financial CEO who speaks regularly to country officials."

- In short, while the White House's official stance is that "We're doing very well with respect to a potential trade deal with China" and "18 proposals" from various trading partners being reviewed (per WH Press Secretary Leavitt today), there is little evidence of any concrete progress on major trade deals.

- An additional item on the agenda worth noting for any insight on this and other fronts: Bessent says on X.com that he will be sharing his "thoughts on the state of the global financial system" at an IIF event at 10ET Wednesday.

US TSYS: Reality Check Slowly Emerging For Tariff Negotiations

- Treasuries look to finish mixed Tuesday, curves unwinding a large portion of Monday's steepening with bonds outperforming weaker short end rates (2s10s -6.174 at 58.027) as markets re-assess tariff-tied risks to global trader and the Trump Admin's efforts to meddle with the Federal Reserve's independent policy making.

- Europe returned from extended Easter holiday improved market depth more than trade volumes evidently (TYM5 at 1.2M near steady to Monday's levels) while the week openers risk-off tone was gradually unwound.

- Brief midday risk-on move extended after headlines that Tsy Sec Bessent (speaking at a JP Morgan event in DC - closed to public and media) sees the China tariff standoff as unsustainable and expects a de-escalation to occur. Bloom quickly came off the rose as sources clarified the gist of negotiations would be a "slog".

- Limited react to data: The Philly Fed non-mfg activity index fell further in April to -42.7 from -32.5 in Mar, -13.1 in Feb and -9.1 in Jan; Johnson Redbook Same-Store Retail month-to-date Y/Y sales up 7.0% (the week ending April 19 was +7.4% Y/Y). Same with Fed speakers, taking a back seat to headline risk.

- Cross asset: Gold retreats to 5372.0 currently after topping 5500.0 briefly overnight; Greenback rebounding BBG US$ index +5.01 at 1221.15; SPX eminis +110 at 5294.75.

AUDUSD TECHS: Clears Key Resistance

- RES 4: 0.6550 61.8% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6528 High Nov 29 ‘24

- RES 2: 0.6471 High Dec 9 ‘24

- RES 1: 0.6439 High Apr 22

- PRICE: 0.6392 @ 16:20 BST Apr 22

- SUP 1: 0.6370/6291 Low Apr 21 / 20-day EMA

- SUP 2: 0.6181 Low Apr 11

- SUP 3: 0.6116 Low Apr 10

- SUP 4: 0.5915 Low Apr 9 and key support

AUDUSD traded higher again overnight Tuesday and the pair is building on the latest gains . A key resistance at 0.6409, the Dec 9 ‘24 high, has been cleared. This reinforces bullish conditions and signals scope for a continuation higher near-term. Sights are on 0.6471 next, the Dec 9 2024 high. Initial key support to monitor is 0.6291, the 20-day EMA. A clear break of this EMA would be a concern for bulls.