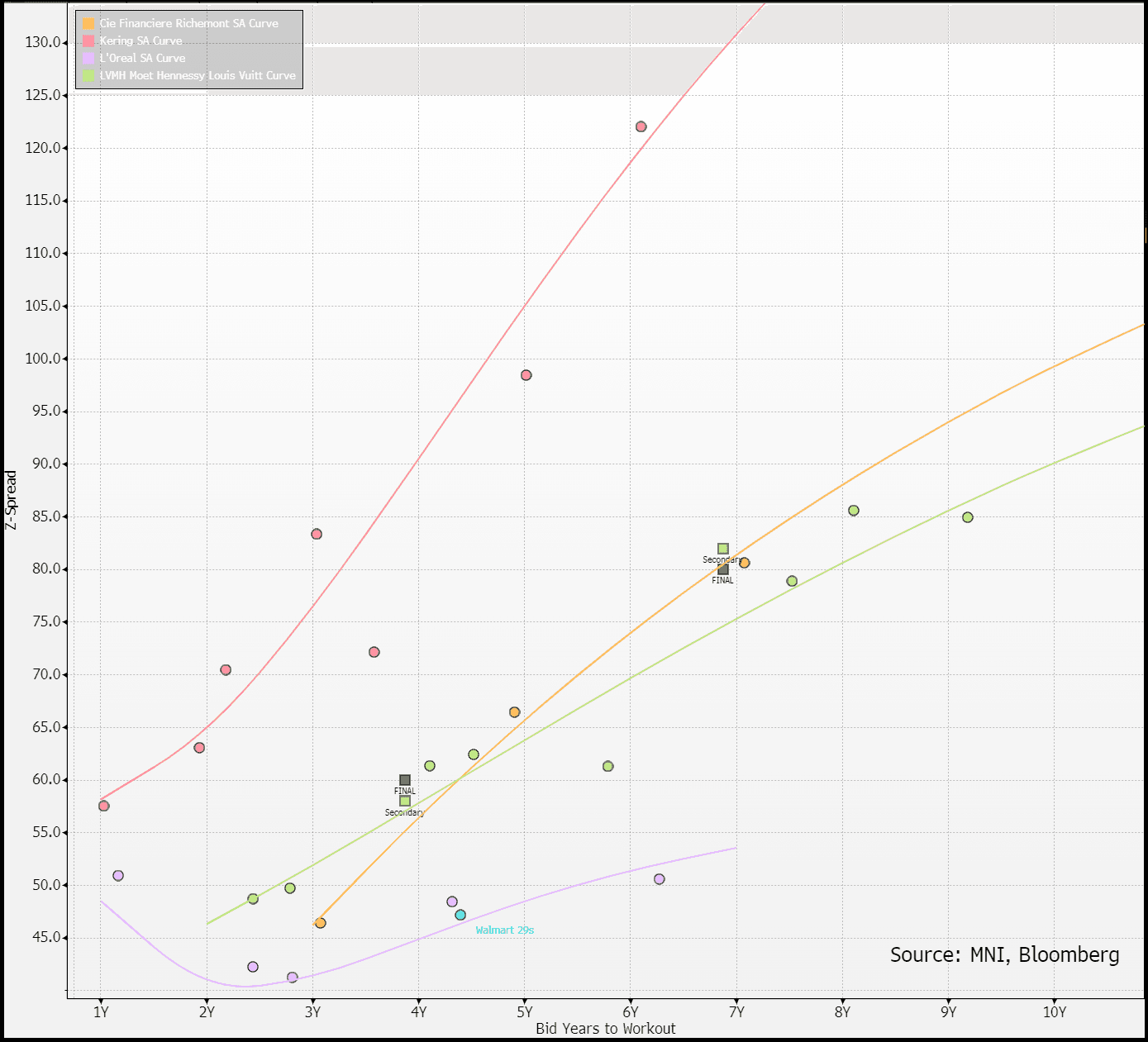

EU CONSUMER CYCLICALS: LVMH | Effective Tap

(MCFP; Aa3/AA-)

The 7y is upsized from €800m to €900m, all other terms unchanged.

Long-end secondary we still see needing to reprice wider.

It is the widest AA consumer curve and we see this warranted on a 'Arnault discount'.

€1.1b 3.9Y: 8bp NIC, books 2.2x

€0.9b 6.9Y: 8bp NIC, books 1.6x (1.8x originally)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EFSF ISSUANCE: Syndication: 5-year May-30: Final terms

- Size: E5bln

- Final Spread set earlier: MS+30bps (guidance was MS+32bps area)

- Books closed in excess of E19.5bln pre-rec (ex JLM interest)

- Maturity: 07-May-2030

- Settlement: 07-Apr-2025 (T+5)

- Coupon: Long first to 07-May-2026

- Bookrunners: CITI/CACIB(DM/B&D)/SG

- ISIN: EU000A2SCAT6

- Timing: Allocations to follow

EUROPEAN INFLATION: MNI Projects 2.2% Y/Y German National CPI, Core 2.6%

From state-level index data that equates to 89.1% weighting of the national February flash German CPI print (due at 13:00 GMT / 14:00 CET), MNI estimates that national CPI (non-HICP print) rose by 0.3-0.4% M/M (Feb 0.4%) and rose 2.2-2.3% Y/Y (Feb 2.3%). See the tables below for full calculations.

- Analyst consensus stands at 2.2% Y/Y and 0.3-0.4% M/M, so the release appears to come in inline.

- Current tracking of core CPI (ex-energy and food, based on 50% of the national index) implies around 2.6% Y/Y (2.7% in Feb) and 0.6% M/M (0.3% Feb).

- We will provide a follow-up bullet looking at underlying drivers in due course.

- Note: These estimates are in relation to the national CPI print, not the HICP print which feeds into the Eurozone HICP print that the ECB targets. The magnitude of surprises to consensus can sometimes be different due to the different methodologies and weights used in national CPI vs HICP - but the direction of the surprise is normally the same.

| Y/Y | March (Reported) | February (Reported) | Difference |

| North Rhine Westphalia | 1.9 | 1.9 | 0.0 |

| Hesse | 2.4 | 2.3 | 0.1 |

| Bavaria | 2.3 | 2.4 | -0.1 |

| Brandenburg | 2.3 | 2.3 | 0.0 |

| Baden Wuert. | 2.2 | 2.5 | -0.3 |

| Berlin | 1.9 | 2.0 | -0.1 |

| Saxony | 2.5 | 2.3 | 0.2 |

| Rhineland-Palatinate | 2.0 | 2.4 | -0.4 |

| Lower Saxony | 2.4 | 2.5 | -0.1 |

| Saarland | 2.0 | 2.4 | -0.4 |

| Saxony-Anhalt | 2.9 | 3.0 | -0.1 |

| Weighted average: | 2.22% | for | 89.1% |

| M/M | March (Reported) | February (Reported) | Difference |

| North Rhine Westphalia | 0.3 | 0.4 | -0.1 |

| Hesse | 0.4 | 0.3 | 0.1 |

| Bavaria | 0.3 | 0.4 | -0.1 |

| Brandenburg | 0.4 | 0.6 | -0.2 |

| Baden Wuert. | 0.2 | 0.5 | -0.3 |

| Berlin | 0.6 | 0.4 | 0.2 |

| Saxony | 0.6 | 0.3 | 0.3 |

| Rhineland-Palatinate | 0.2 | 0.2 | 0.0 |

| Lower Saxony | 0.3 | 0.4 | -0.1 |

| Saarland | 0.2 | 0.3 | -0.1 |

| Saxony-Anhalt | 0.7 | 0.5 | 0.2 |

| Weighted average: | 0.36% | for | 89.1% |

US TSYS: 10s Stabilise Around 4.20%, March Yield Lows Unchallenged

10-Year Tsy yields stabilise around 4.20%, ~10bp off the March low (4.104%) and a couple of bp off session lows.

- TY futures back to 111-17+ vs. session highs of 111-22+. Resistance at the March 20 high (111-17+) pierced, with bulls now looking to force a break above the March 11 high (111-25) as they aim to build further on last week’s gains. The medium-term trend condition is the contract is bullish.

- U.S. reaction to the risk-off price action seen in Asia & the London morning now eyed.