EQUITIES: Looking at next Week's Option Expiry

Looking at next Week's Equity Option Expiry, on the 15th August, at present in Notional term:

US:

- SPX: $1.23T.

- NDX: $52.42bn.

- Amazon: $17.48bn.

- Apple: $16.75bn.

EU:

- SX5E: €148.31bn.

- SX7E: €3.15bn.

- DAX: €22.13bn.

- UKX: £9.56bn.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Early SOFR/Treasury Option Roundup: Fading the Bounce

SOFR & Treasury option flows (overnight to current) appear to be taking advantage of the rebound in underlying futures to buy puts/put spreads (Dec SOFR put tree looking at year end Fed on hold), unwind calls with a few exceptions. Projected rate cut pricing largely steady vs late Tuesday (*) levels: Jul'25 steady at -1.2bp, Sep'25 steady at -17.3bp, Oct'25 steady at -31.7bp, Dec'25 at -49.3bp (-48.6bp).

- SOFR Options:

- +5,000 SFRZ5 95.62/95.68/95.81 broken put trees, 1.5

- -2,000 SFRH6 96.37/96.87 call spds, 15.0 ref 96.40/0.26%

- +2,500 SFRU5 95.62/95.75 put spds, 3.0

- -15,000 0QU5 97.12/98.12 call spds, 5.25 ref 96.745

- +6,000 SFRU5 95.75/96.00/96.25 call trees, 9.0 ref 95.865

- +4,000 SFRZ5 95.87/96.62 call over risk reversals, 1.0 vs. 96.15/0.40%

- +1,000 SFRZ5 96.25 straddles, 38.5

- over +20,000 SFRQ5 95.68/95.75 put spd, 1.25 (more on a 2x3 ratio)

- +2,000 SFRQ5/SFRU5 95.75 put spd, 2.0

- 3,000 SFRU5 95.62/95.75 put spd, 3.0

- Treasury Options:

- 10,000 TYQ5 110.5/111.5 put spds 33 vs. 111-00/0.34%

- -5,000 TYU5 111 calls, 46 vs 110-24/0.44%

- +2,250 TYU5 110/110.5/111/111.5 call condor, 7 vs 110-30/0.05%

- 3,950 TYQ5 111.75/112.25 call spds ref 110-28

- -5,000 wk2 TY 111 put, 15

- +5,000 wk2 TY 111 straddle, 26 vs 110-28.5 to -29/0.20%

EQUITIES: US Cash Opening calls

US Cash Opening calls: We'll be opening higher, but will be short of the record highs:

- Calls: SPX: 6,253.5 (+0.4%); DJIA: 44,452 (+0.5%/+211pts); NDX: 22,795.8 (+0.4%).

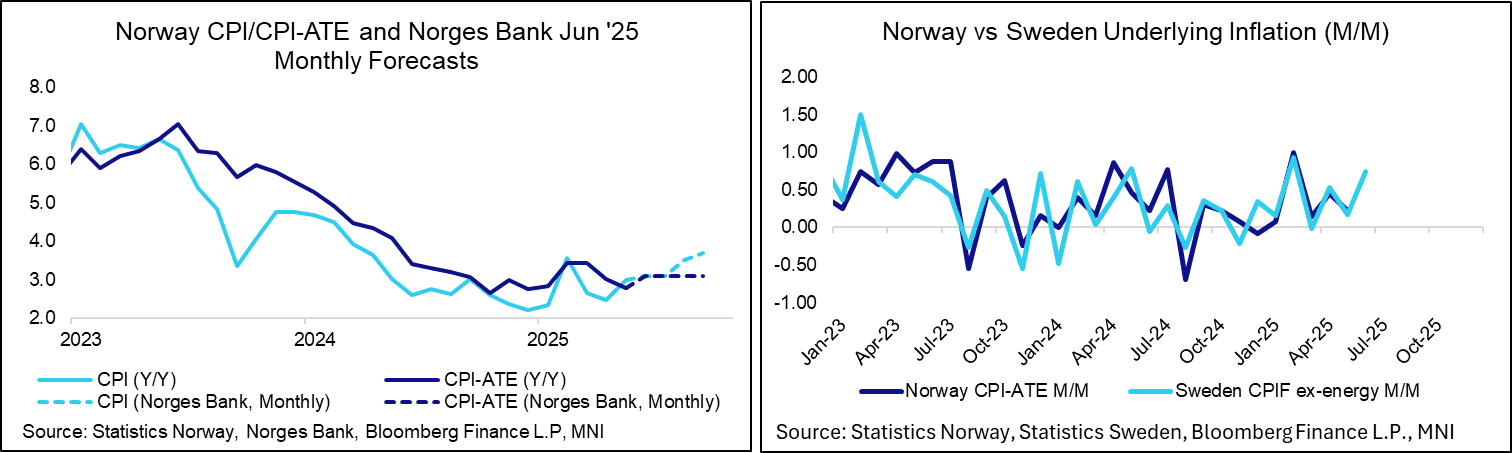

NORWAY: June Inflation Tomorrow, Swedish Print Adds Upside Risks

Norwegian June inflation is due tomorrow at 0700BST/0800CET. This will be the first inflation report since Norges Bank’s surprise 25bp cut on June 19. In an interview with the MNI Policy Team following the decision, Governor Wolden Bache indicated that Norges Bank opted to cut rates because it had gained confidence that the Q1 uptick in inflationary pressures was temporary. In this light, we think the base case should be that further cuts can be delivered in September and possibly December if CPI-ATE tracks in line with Norges Bank’s projections – provided economic activity momentum doesn’t accelerate unexpectedly. We continue to think that the bar to rate moves at interim decisions (August and November) is high, but NOK FX and rate markets will as usual be sensitive to large deviations from consensus.

- In the June MPR, Norges Bank projected CPI-ATE inflation at 3.1% Y/Y in June through September (May: 2.77% Y/Y). For tomorrow’s print, the median analyst pencils in a 3.0% Y/Y reading.

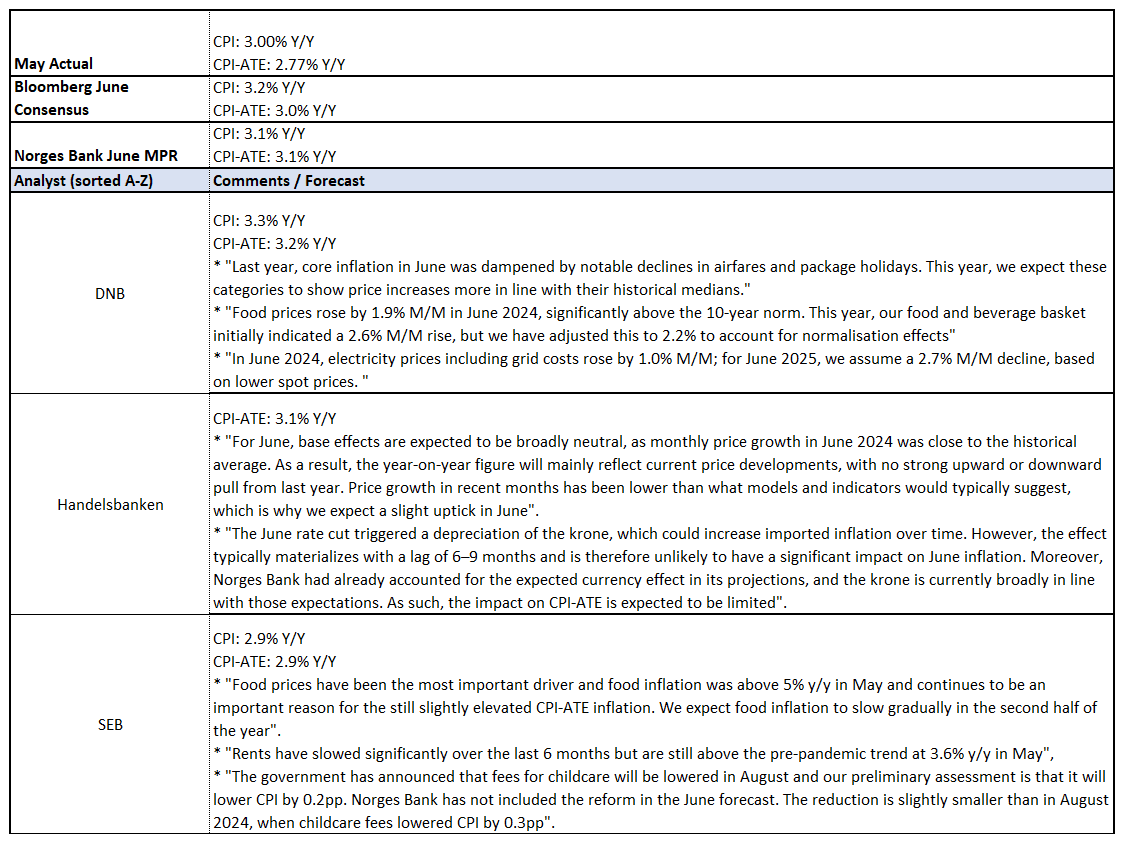

- There could be upside risks to analyst and Norges Bank projections after Monday’s Swedish flash June inflation report (3.3% Y/Y vs 2.9% cons, 2.5% prior). Since 2015, there has been a 0.56 correlation between M/M NSA Norwegian CPI-ATE inflation and Swedish CPIF ex-energy inflation. Since 2023, this correlation has risen to 0.69. The chart below also indicates a close relationship between the two inflation rates since February. Clearly, this is a crude and non-causal observation, but still worth keeping in mind.

- Swedish CPIF ex-energy was 0.74% M/M in June. If realised in Norway, this would imply an annual rate of 3.3% Y/Y – comfortably above expectations.

- Norges Bank projects headline CPI inflation at 3.1% Y/Y (vs 3.00% prior), while analysts see 3.2% Y/Y.

- See below for a selection of analyst comments: