AUSSIE BONDS: Little Changed After April CPI Data

May-28 01:44

ACGBs (YM -2.0 & XM flat) are modestly richer after the release of April CPI data.

- The April headline CPI was a touch above expectations at 2.4%y/y (2.3% was forecast). The trimmed mean rose 2.8% y/y (against a 2.7% prior outcome, there is no consensus estimate for this print).

- Total construction unchanged q/q (estimate +0.5%) in Q1 versus a revised +0.9% in Q4.

- Total value of Australia’s building work for private new houses rose 1.1% to A$12.6b in the first quarter from the previous three months. (per BBG)

- Cash US tsys have modestly bear-steepened in today's Asia-Pac session, with yields flat to 2bps higher.

- Cash ACGBs are 1bps richer after the data but retain a bear-flattener, with yields flat to 2bps higher. The AU-US 10-year yield differential is -15bps.

- Swap rates are also 1bp lower after the data.

- The bills strip is -1 to -3 across contracts.

- RBA-dated OIS pricing is little changed across meetings after the data. A 25bp rate cut in July is given a 70% probability, with a cumulative 73bps of easing priced by year-end (based on an effective cash rate of 3.84%).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

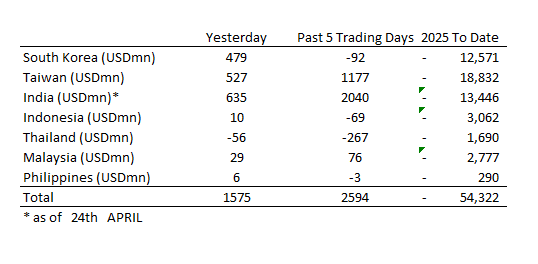

ASIA STOCKS: Strong Inflows to End Last Week

Apr-28 01:41

The ongoing theme of outflows took a breather at the end of last week as strong inflows were recorded across major markets.

- South Korea: Recorded inflows of +$479m as of Friday, bringing the 5-day total to -$92m. 2025 to date flows are -$12,571m. The 5-day average is -$18m, the 20-day average is -$424m and the 100-day average of -$151m.

- Taiwan: Had inflows of +$527m as of Friday, with total inflows of +$1,177m over the past 5 days. YTD flows are negative at -$18,832. The 5-day average is +$235m, the 20-day average of -$185m and the 100-day average of -$207m.

- India: Had inflows of +$635m as of the 24th, with total inflows of +$2,040m over the past 5 days. YTD flows are negative -$13,446m. The 5-day average is +$408m, the 20-day average of +$129m and the 100-day average of -$118m.

- Indonesia: Had inflows of +$10m as of Friday, with total outflows of -$69m over the prior five days. YTD flows are negative -$3,062m. The 5-day average is -$14m, the 20-day average -$63m and the 100-day average -$39m

- Thailand: Recorded outflows of -$56m as of Friday, outflows totaling -$267m over the past 5 days. YTD flows are negative at -$1,690m. The 5-day average is -$53m, the 20-day average of -$30m the 100-day average of -$21m.

- Malaysia: Recorded inflows of +$29m as of Friday, totaling +$76m over the past 5 days. YTD flows are negative at -$2,777m. The 5-day average is +$15m, the 20-day average of -$32m the 100-day average of -$38m.

- Philippines: Saw inflows of +$6m as of Friday, with net outflows of -$3m over the past 5 days. YTD flows are negative at -$290m. The 5-day average is -$1m, the 20-day average of -$5m the 100-day average of -$5m.

LNG: Lower Demand Allowing Inventories To Be Rebuilt

Apr-28 01:33

Natural gas is down sharply in April as heating demand declines and cooling usage is yet to rise, which is allowing storage to be refilled. European prices fell 4.8% to EUR 31.95 on Friday, around the intraday low, to be down 21.4% this month.

- Bloomberg reported that European LNG imports are higher than usual for this time of year aided by lower demand in Asia allowing further refilling. Trade deals between the US and China and other Asian countries could reverse this trend to a degree. The ability to rebuild EU gas inventories ahead of next winter has worried markets for most of 2025.

- US gas rose 2.0% on Friday to $3.16 (June contract) but was down almost 26% on the month as April is part of the shoulder season that requires little heating or cooling driving a larger-than-expected increase in inventories in the latest data. Prices have been flashing oversold on an RSI basis (Bloomberg).

- US lower-48 production rose 3.9% y/y, while demand fell 6.9% y/y on Friday. One of the major US gas producers EQT said that it plans to increase output in 2025 though, according to Bloomberg. A number of countries have offered to buy more US LNG as part of a deal to lower US tariffs they could face.

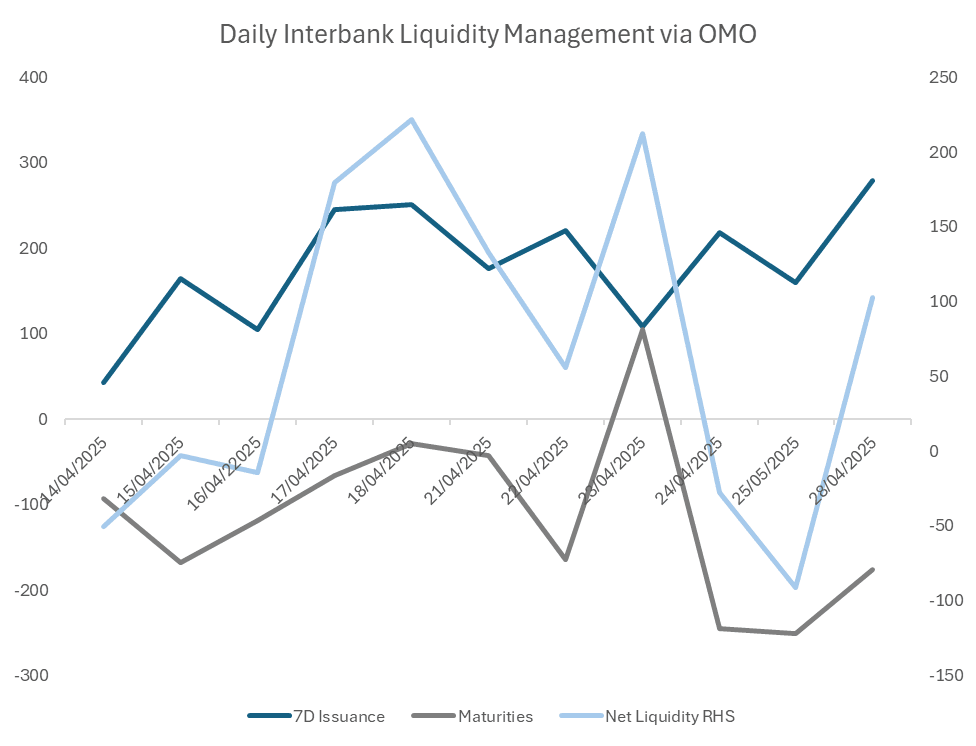

CHINA: Central Bank Injects Liquidity via OMO

Apr-28 01:30

- The PBOC issued CNY279bn of 7-day reverse repo at 1.5% during this morning’s operations.

- Today’s maturities CNY176bn

- Net liquidity injection CNY103bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.55%, from 1.71% on the 27th.

- The China overnight interbank repo rate is at 1.60%, from the prior close of 1.59%.

- The China 7-day interbank repo rate is at 1.78%, from the prior close of 1.68%.