US STOCKS: Late Equity Roundup: Mildly Lower on Week

May-06 20:05

Equity indexes weaker into the close are off session lows, upper half of range SPX emini futures, ESM2 currently -30.25 points (-0.73%) at 4113.75 -- near week opener of 4146.25.

- Earnings cycle past the halfway mark, resumes Monday w/ Duke Energy (DUK), Tyson (TSN) before the open, Trex (TREX), Int Flavor/Fragrances (IFF), Cargurus (CARG) after the close.

- SPX leading/lagging sectors: Energy sector extends earlier gains (+2.91%) O&G consumables outpacing energy and equipment serving names. Utilities sector follows (+0.81%). Laggers: Materials sector holding near lows (-1.40%) w/ construction materials shares lagging; Communications sector (-1.30%).

- Meanwhile, Dow Industrials currently trades -97.15 points (-0.29%) at 32901.08, Nasdaq -173 points (-1.4%) at 12144.66.

- Dow Industrials Leaders/Laggers: United Health outperforms (UNH) +5.10 at 499.82, Chevron (CVX) +4.00 at 170.26. Laggers: Home Depot (HD) continues to sag -4.47 at 294.64, Nike (NKE) -3.62 at 115.01.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK, Late 5Y Buy

Apr-06 19:56

- +8,250 FVM2 113-12.5 (+.5), buy through 113-11.75 post-time offer at 1547:40ET, appr $400k DV01

AUDUSD TECHS: Holds Close to Cycle Highs

Apr-06 19:30

- RES 4: 0.7776 High Jun 11 2021

- RES 3: 0.7762 76.4% retracement of the Feb ‘21 - Jan ‘22 downleg

- RES 2: 0.7716 High Jun 16 2021

- RES 1: 0.7661/64 High Apr 5 / 2.0% 10-dma envelope

- PRICE: 0.7535 @ 17:23 BST Apr 6

- SUP 1: 0.7534 Low Apr 6

- SUP 2: 0.7457 Low Mar 29 and a key support

- SUP 3: 0.7441/7376 20-day EMA / Low Mar 22

- SUP 4: 0.7339 50-day EMA

AUDUSD rallied Tuesday and the break higher confirmed a resumption of its uptrend. Tuesday’s gains also confirmed a bull flag breakout and price has cleared resistance at 0.7556, the Oct 28 2021 high. The Aussie has also cleared the Jul 6 2021 high of 0.7599 and 0.7610, 61.8% of the Feb ‘21 - Jan ‘22 downleg. This opens 0.7716 next, the Jun 16 2021 high. The pair lagged slightly throughout the Wednesday session, but the onus remains higher for now. Key support has been defined at 0.7457, the Mar 29 low.

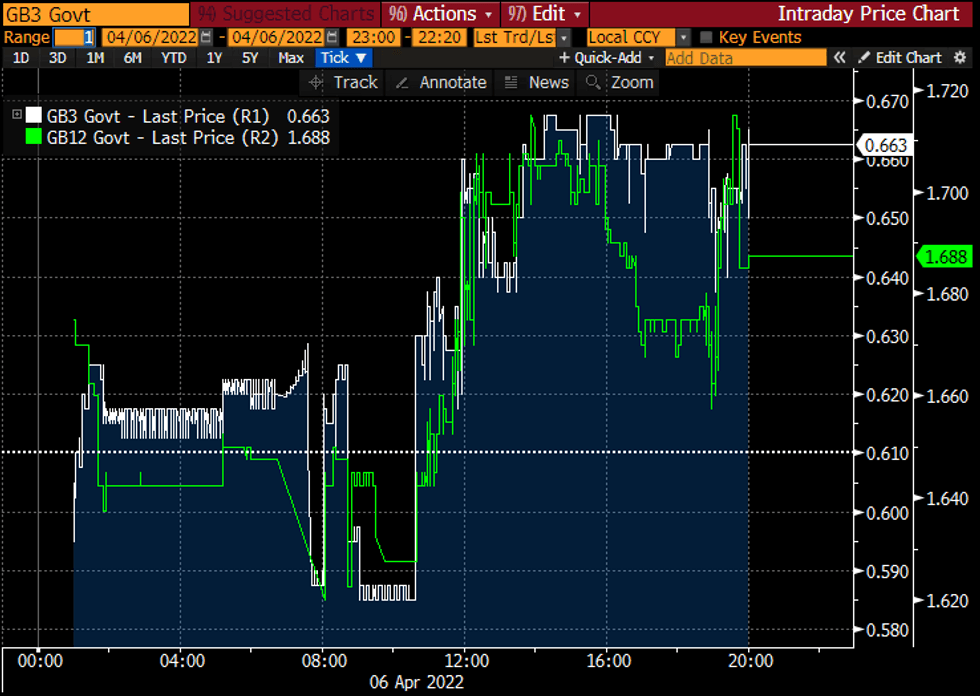

Little Reaction To Potential Inclusion In Runoff

Apr-06 19:06

- Relatively little reaction in T-bills to most participants judging it appropriate to redeem bills when Tsy coupon principal payments are below the cap -- only a few analysts had expected inclusion.

- 3M bills trade 1bp softer since the release (unchanged from 15mins before the minutes) at 0.66%, which is presumably unsurprising with a ramp-up period of three months or modestly longer for Tsys.

- 12M bills sold off 4.5bps, indicating a greater likelihood of months where the Tsy cap isn’t met, but only to earlier intraday highs and more surprisingly giving more than half of this back at 1.688%.