EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.59% -3bp

10yr UST 4.04% -5bp

5s-10s UST 45.0 -2bp

WTI Crude 63.8 +1.2

Gold 3639 +12.4

Bonds (CBBT) Z-Sprd Δ DoD

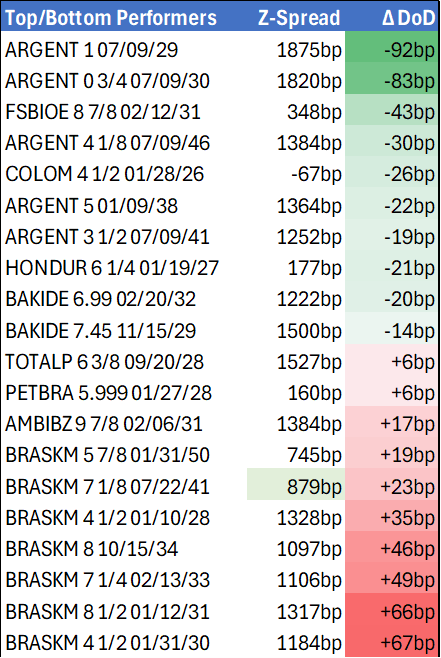

ARGENT 3 1/2 07/09/41 1252bp -17bp

BRAZIL 6 1/8 03/15/34 238bp -3bp

BRAZIL 7 1/8 05/13/54 332bp -5bp

COLOM 8 11/14/35 313bp -12bp

COLOM 8 3/8 11/07/54 381bp -16bp

ELSALV 7.65 06/15/35 410bp -13bp

MEX 6 7/8 05/13/37 238bp -7bp

MEX 7 3/8 05/13/55 296bp -4bp

CHILE 5.65 01/13/37 133bp -3bp

PANAMA 6.4 02/14/35 256bp -1bp

CSNABZ 5 7/8 04/08/32 586bp +2bp

MRFGBZ 3.95 01/29/31 253bp -4bp

PEMEX 7.69 01/23/50 457bp -12bp

CDEL 6.33 01/13/35 200bp -1bp

SUZANO 3 1/8 01/15/32 171bp -2bp

FX Level Δ DoD

USDBRL 5.41 -0.03

USDCLP 962.75 -5.15

USDMXN 18.6 -0.03

USDCOP 3925.10 +2.33

USDPEN 3.48 -0.02

CDS Level Δ DoD

Mexico 90 (5)

Brazil 134 (4)

Colombia 169 (12)

Chile 46 (2)

CDX EM 98.16 0.08

CDX EM IG 101.59 0.05

CDX EM HY 94.65 0.14

Main stories recap:

· A tame producer price index (PPI) report and a solid 10-year U.S. Treasury auction led to a bull flattener with long end yields falling 4bp ahead of tomorrow’s consumer price index (CPI) report.

· We saw heavy supply in EM with more on tap. Asia offered one new issue while CEEMEA priced four new issues.

· LATAM gave us a three tranche Colombia sovereign deal in Euros totaling EUR4.1bn and a USD200mn PerpNC7 from development bank Bladex. Three LATAM mandates are likely to be priced tomorrow, and we have fair value analysis available for all of them.

· Argentina sovereign bonds outperformed, up about a point, on supportive comments from the IMF as well as a lower than expected August inflation print.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: UBS Above Consensus For Core CPI In July

- UBS see core CPI at a seasonally adjusted 0.35% M/M in July, a little above consensus of 0.3% or MNI unrounded 0.32% and top of the unrounded analyst estimates we've seen to date.

- They see core goods inflation accelerating to 0.38% M/M after 0.2% M/M in June, but largest increases set for subsequent months with 0.6% in Aug, 0.76% in Sep and 0.73% in Oct.

- They see core services inflation accelerate from 0.25% to 0.35% M/M, led sequentially by lodging away from home and airfares.

- On latest Adobe data: “In July this year the Adobe DPI declined more than in the same month last year, but less than in July 2023 and the five years prior to the pandemic. That moderately strong, but not booming, price change has been a recent theme in the Adobe data. Nonetheless, moderately strong increases add up: Since the implementation of the China tariffs in early February the Adobe DPI has declined less than in similar 6-month periods in any year in its 12-year history except for the start of the inflation surge in”.

USDCAD TECHS: Shallow Bounce Off Lows

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3920 High May 21

- RES 1: 1.3879 High Aug 1

- PRICE: 1.3792 @ 15:33 BST Aug 11

- SUP 1: 1.3557 Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

USDCAD remains subdued, despite the shallow bounce Friday feeding through to further gains on Monday. This follows the weaker-than-expected jobs data last week. The pair remains notably lower on the week on the back of last Friday’s USD weakness. Initial firm support has been breached at the 1.3737 20-day EMA, a break below which would resume the correction off the early August high at 1.3879. On the recent run higher, price traded through the 50-day EMA at 1.3744, which aided the rally. This week’s price action, however, has cancelled that bullish threat and returned focus lower. The 100-dma becomes a key pivot point at 1.3824 last.

US TSYS: Leaning Bull Flatter Ahead Of CPI

The Treasury curve leaned bull flatter Monday ahead of Tuesday's CPI release.

- With no key data or Fed speakers on Monday's schedule, and looming CPI being the week's most impactful release, trading was relatively subdued and focused more on geopolitical developments.

- That included anticipation of the Trump-Putin meeting later this week per the Ukraine conflict, and the China tariff truce which was due to expire Tuesday (but per CNBC has been extended by 90 days as widely expected).

- In contrast to last week's reports which drew a small but notable reaction (namely firming the USD), there was little reaction to a Bloomberg report that current FOMC members Vice Chair for Supervision Bowman, Vice Chair Jefferson, and Dallas Fed's Logan are in the running to succeed current Fed Chair Powell.

- Indeed Bowman's comments over the weekend re eyeing 3 rate cuts by year-end were largely taken in stride as she's been a vocal (and dissenting) dove in recent months.

- Implied Fed funds were unchanged through year-end, still eyeing 57bp of cuts. Tsy yields traded within Friday's ranges overall, with volumes light (725k TYU5 contracts traded through 3:45ET)

- As noted, Friday sees a busier schedule including CPI - MNI's preview is here. Consensus sees core CPI inflation at 0.3% M/M and unrounded analyst estimates broadly echo this with a median 0.32% M/M. We also hear from Fed's Barkin (non-2025 voter) and Schmid (2025 voter, hawk) after CPI, with other data including the NFIB small business survey and the Federal budget statement.

- Latest levels: The 2-Yr yield is down 0.4bps at 3.758%, 5-Yr is down 0.7bps at 3.8242%, 10-Yr is down 1.2bps at 4.2713%, and 30-Yr is down 0.9bps at 4.8403%. Sep 10-Yr futures (TY) up 1.5/32 at 111-28 (L: 111-25 / H: 112-0-)