EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.99% +0bp

10yr UST 4.46% 0bp

5s-10s UST 45.8 -0bp

WTI Crude 67.6 +1.2

Gold 3339 -7.8

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 980bp +22bp

BRAZIL 6 1/8 03/15/34 249bp -1bp

BRAZIL 7 1/8 05/13/54 343bp +0bp

COLOM 8 11/14/35 393bp -3bp

COLOM 8 3/8 11/07/54 468bp -2bp

ELSALV 7.65 06/15/35 432bp -13bp

MEX 6 7/8 05/13/37 255bp +0bp

MEX 7 3/8 05/13/55 318bp +1bp

CHILE 5.65 01/13/37 141bp -1bp

PANAMA 6.4 02/14/35 300bp -3bp

CSNABZ 5 7/8 04/08/32 570bp -0bp

MRFGBZ 3.95 01/29/31 275bp -0bp

PEMEX 7.69 01/23/50 605bp +4bp

CDEL 6.33 01/13/35 197bp -2bp

SUZANO 3 1/8 01/15/32 169bp +0bp

FX Level Δ DoD

USDBRL 5.54 -0.02

USDCLP 962.96 -4.81

USDMXN 18.8 +0.04

USDCOP 4021.90 +5.96

USDPEN 3.56 +0.01

CDS Level Δ DoD

Mexico 109 3

Brazil 147 (4)

Colombia 212 (4)

Chile 56 (1)

CDX EM 97.59 0.11

CDX EM IG 101.26 0.04

CDX EM HY 93.82 0.14

Main stories recap:

Comments

· The S&P 500 Stock Index hit a new all-time high in the wake of stronger than expected U.S. economic data including monthly retail sales and weekly initial jobless claims which also led to a small sell off in shorter maturity U.S. Treasuries.

· The pace of new issuance in EM slowed compared to last week with no new Asia issues, one new deal in CEEMEA and one new issue in LATAM today.

· Secondary benchmark bond spreads in Asia and CEEMEA were mixed with relatively small changes while in LATAM we saw similar behavior, though there were some outliers.

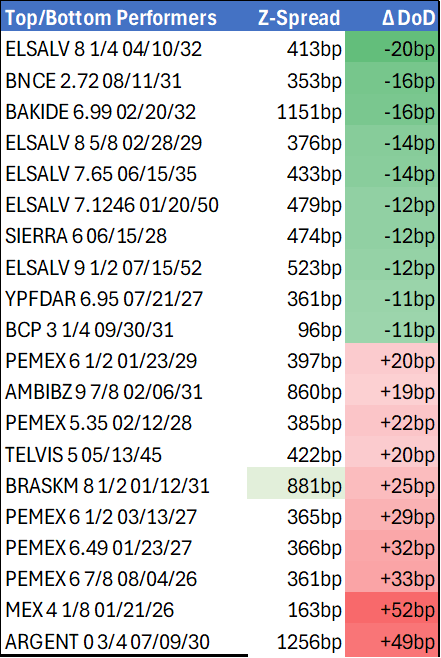

· Argentina sovereign bonds widened about 20bp while Pemex bonds moved out on average about 10bp and Braskem bond spreads widened 12bp with all three instances appearing to be persisting trends in the wake of bad news in past days.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Fresh Cycle Low

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4111 High Apr 4

- RES 2: 1.3850/1.4016 50-day EMA / High May 12 and 13

- RES 1: 1.3717 20-day EMA

- PRICE: 1.3594 @ 15:52 BST Jun 17

- SUP 1: 1.3540/3521 Low Jun 16 / 1.0% 10-dma envelope

- SUP 2: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 3: 1.3473 Low Oct 2 2024

- SUP 4: 1.3410 1.764 proj of the Feb 3 - 14 - Mar 4 price swing

The trend needle in USDCAD continues to point south and fresh cycle lows last week and again on Monday, reinforce a bearish theme. Support at 1.3686, the May 26 low and a bear trigger, has been cleared, confirming a resumption of the downtrend. This maintains the price sequence of lower lows and lower highs. Sights are on 1.3521 next, envelope-based support. Resistance at the 20-day EMA is at 1.3732.

US TSYS: Safe Haven Raises Rates in Lead-Up to FOMC Policy Annc

- Rising Middle East tensions included chances the US will join the war lent to the second half risk-off support for Treasuries Tuesday. Otherwise, markets await Wednesday's FOMC policy announcement including a Summary of Economic Projections (Dots).

- Pres Trump: "We know exactly where the so-called “Supreme Leader” is hiding. He is an easy target, but is safe there - We are not going to take him out (kill!), at least not for now. But we don’t want missiles shot at civilians, or American soldiers. Our patience is wearing thin. Thank you for your attention to this matter!"

- We expect that the June FOMC meeting communications will reflect an increasingly patient attitude since May and certainly since March’s projections.

- Cross asset update: stocks ebbed in the second half (SPX eminis -44.75 at 6045.0), West Texas crude climbed to early July 2024 highs (WTI +3.39 at 75.16), while Bbg US$ index climbed to June 11 highs (BBDXY +6.43 at 1209.02).

- Tsy Sep'25 10Y futures trades +12.5 at 110-28 vs. 111-00 high, below key resistance and its recent high of 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish and highlight a stronger reversal. This would open 111-30, a Fibonacci retracement.

- Curves flatter, 2s10s -4.250 at 43.309, 5s30s -1.837 at 90.209. 10Y yield at 4.3849% vs. 4.3770% low.

FED: Statement: Uncertainty Still Elevated (4/4)

Going paragraph by paragraph through the previous (May) statement opening paragraphs in italics:

- The opening paragraph of the Statement may as usual be marked-to-market, but the previous edition’s description of the economy largely still stands. We would be surprised if the Fed described labor market conditions as anything but “solid”, or inflation as anything but “somewhat elevated”.

- A change to either would almost certainly lean to the dovish side, with recent inflation data surprising to the downside and broad labor market indicators cooling, but it’s unlikely the FOMC would want to send such a signal this month.

- There probably hasn’t been enough evidence in the “hard” data to refer to economic activity as running at anything but a “solid” pace, though a tweak here to something like “moderate” is possible and probably not impactful. There may also be an adjustment of the language on “swings in net exports”, though this continues to be useful given the inventory/net export swings between Q1 and Q2.

- With a tentative US-China trade deal in place, it’s likely that the second paragraph will remove references to uncertainty and risks having risen, merely saying perhaps that they are/remain elevated.

- The Fed could at some point alter its assessment of the balance of risks to suggest that they are concerned that one of the dual mandate goals needs to be addressed at the potential expense of the other, but that would require much clearer evidence in the data.

- For an FOMC that is waiting to see the impact of tariffs and other policy shifts, even as it maintains its overall easing bias, a shift in forward rate guidance (“in considering the extent and timing of additional adjustments…”) looks unlikely at this juncture.

- No dissents are expected. In the Implementation Note, no changes to the administered rates are expected.