LATIN AMERICA: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.96% -3bp

10yr UST 4.38% -1bp

5s-10s UST 41.6 +2bp

WTI Crude 74.9 -0.2

Gold 3365 -5.6

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 927bp +2bp

BRAZIL 6 1/8 03/15/34 260bp -0bp

BRAZIL 7 1/8 05/13/54 361bp +2bp

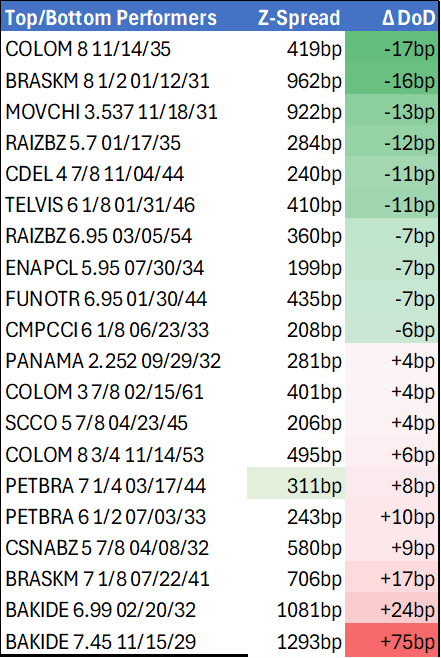

COLOM 8 11/14/35 419bp -17bp

COLOM 8 3/8 11/07/54 496bp -3bp

ELSALV 7.65 06/15/35 446bp +2bp

MEX 6 7/8 05/13/37 259bp +3bp

MEX 7 3/8 05/13/55 321bp +2bp

CHILE 5.65 01/13/37 149bp -1bp

PANAMA 6.4 02/14/35 308bp +3bp

CSNABZ 5 7/8 04/08/32 580bp +9bp

MRFGBZ 3.95 01/29/31 278bp +3bp

PEMEX 7.69 01/23/50 639bp -0bp

CDEL 6.33 01/13/35 209bp -2bp

SUZANO 3 1/8 01/15/32 185bp -5bp

FX Level Δ DoD

USDBRL 5.52 +0.03

USDCLP 942.88 +2.48

USDMXN 19.2 +0.13

USDCOP 4095.45 +10.53

USDPEN 3.60 +0.01

CDS Level Δ DoD

Mexico 108 (1)

Brazil 157 (2)

Colombia 226 (0)

Chile 56 (0)

CDX EM 96.99 0.02

CDX EM IG 101.01 (0.02)

CDX EM HY 92.98 (0.01)

Main stories recap:

Comments

· Mixed close in equity indexes with verdict of whether U.S. will enter the Iran-Israel fray still hovering while tariff tensions still seem heightened as Japan cancelled a high-level meeting in reaction to U.S. demands on defense spending.

· U.S. Treasuries rallied a few bp in the front end with mixed signals coming from a few Fed governors about the next policy move. The Philly Fed business outlook was reported weaker than consensus.

· EM was quiet on the primary market front while in the EM Asia and CEEMEA secondary markets benchmark bond spreads showed a widening bias.

· LATAM secondary market spreads generally widened 2-3bp. Colombia sovereign bonds outperformed, possibly due to Fitch deciding not downgrade ratings in the near term.

· Raizen bonds tightened 7-12bp, bouncing back from a brief sell-off in past days after Fitch moved ratings to negative outlook recently, but people still expected asset sale announcements in the coming weeks.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Moving Average Studies Highlight A Downtrend

- RES 4: 1.4296 High Apr 7

- RES 3: 1.4200 Round number resistance

- RES 2: 1.4111 High Apr 4

- RES 1: 1.4016/17 High May 12 / 13 / 50-day EMA

- PRICE: 1.3827 @ 16:28 BST May 21

- SUP 1: 1.3814/3751 Low May 8 / 6 and the bear trigger

- SUP 2: 1.3744 76.4% retracement of Sep 25 ‘24 - Feb 3 bull run

- SUP 3: 1.3696 Low Oct 10 ‘24

- SUP 4: 1.3643 Low Oct 9 ‘24

The trend condition in USDCAD remains bearish and recent gains appear corrective. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the trend would open 1.3744, a Fibonacci retracement. Key resistance to watch is 1.4017, the 50-day EMA. A clear break of this hurdle would signal a stronger reversal and open 1.4111, the Apr 4 high.

US TSYS: Massive Deficit Estimates Tied to Tax/Spending Bill Weighing on Bonds

- Treasuries look to finish near late Wednesday session lows, curves bear steepening: 2s10s +6.792 at 58.019 - highest level since May 1. Heavier volumes tied to Jun/Sep Tsy futures rolls, 5s well over 1M.

- No economic data, headline or outright flow to site for the move other than trepidation over Pres Trump's tax & spending bill estimated to increase the deficit appr $3.3 trillion over 10 years. Lawmakers continued to debate the bill and passage remained uncertain despite Pre Trump personally haranguing GOP holdouts.

- Treasury futures extend session lows after the $16B 20Y Bond auction (912810UL0) tailed, drawing a high yield of 5.047% vs 5.035% When-Issued yield at the cutoff; 2.46x bid-to-cover vs. 2.63x prior. Bonds yield climbed to 5.0955% intraday high - last seen late October 2023. 10Y yield up to 4.5825% (+.0956).

- The Jun'25 10Y futures contract slipped to 109-13.5 low (-25) briefly -- through initial technical support at 109-18.5 (May 15 low) before bouncing to 109-19 - strengthening a bearish theme and exposing key support at 109-08, Apr 24 low and a bear trigger.

- Cross asset update: Gold up 33.4 at 3323.42, stocks weaker with rise in bond yield (SPX emini -95.0 to 5864.75), Crude retreating (WTI -0.62 at 61.41).

- Look ahead to Thursday's data: Weekly Claims at 0830ET, Flash PMIs at 0945ET, Exist Home Sales at 1000ET and KC Fed Mfg Activity at 1100ET.

LOOK AHEAD: Thursday Data Calendar: Weekly Claims, Flash PMIs, Exist Home Sales

- US Data/Speaker Calendar (prior, estimate)

- 22-May 0800 Richmond Fed Barkin fireside chat (no text, Q&A)

- 22-May 0830 Initial Jobless Claims (229k, 230k)

- 22-May 0830 Continuing Claims (1.881M, 1.883M)

- 22-May 0830 Chicago Fed Nat Activity Index (-.03, -0.25)

- 22-May 0945 S&P Global US Manufacturing PMI (50.2, 49.9)

- 22-May 0945 S&P Global US Services PMI (50.8, 51.0)

- 22-May 0945 S&P Global US Composite PMI (50.6, 50.3)

- 22-May 1000 Existing Home Sales (4.02M, 4.10M), MoM (-5.9%, 2.0%)

- 22-May 1100 Kansas City Fed Manf. Activity (-4, -5)

- 22-May 1130 US Tsy $85B 4W & $75B 8W bill auctions

- 22-May 1300 US Tsy $18B 10Y TIPS auction

- 22-May 1400 NY Fed Williams keynote remarks NY Fed event (text, Q&A)