CZK: Koruna Softens Along CE3 Peers, Snr ANO Off'l Vows To Abandon Austerity

EUR/CZK has crept higher to last trade +0.026 at 24.487, with bulls looking for a move towards the 50-DMA, which kicks in at 24.632. On the downside, losses through Aug 11 low of 24.389 would bring Nov 29, 2023 low of 24.203 into play.

- ANO deputy leader Karel Havlíček pledged that his party would reverse the incumbent coalition's austerity measures if it is voted into government in the upcoming parliamentary election. He told Bloomberg that Czechia should abandon 'fiscal self-flagellation' and boost investment to 'kick-start economic growth', but also signalled that an ANO administration would not breach the 3%/GDP deficit cap.

- The Czech Banking Association (CBA) revised Czechia's 2025 GDP forecast to +2.1% Y/Y from its May estimate of +1.7%, citing an improvement in exports and a weaker-than-expected impact of US tariffs. It also adjusted the 2025 inflation outlook higher to +2.5% Y/Y from +2.2%. According to the new forecast, the CNB's policy rate will remain at 3.50% this year before dropping to 3.25% in 1Q26.

- CZGBs are mostly a tad firmer at typing; the PX Index is little changed on the session.

- Czechia's data docket is virtually empty during the remainder of this week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

COMMODITIES: Bearish Tone in WTI Futures Intact, Recent Recovery Corrective

A bearish tone in WTI futures remains intact and the recovery since Jun 24 is considered corrective. The sharp reversal from the Jun 23 high continues to highlight scope for an extension lower. Support to watch is the 50-day EMA, at $65.68. The average has been pierced, a clear break of it would expose $58.87, the May 30 low. Initial resistance to monitor is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. A bull cycle in Gold that started Jun 30, remains intact and the yellow metal is holding on to its recent gains - for now. Note that medium-term trend conditions are bullish - moving average studies are in a bull-mode position highlighting a dominant uptrend. An extension would expose $3395.1, the Jun 23 high, and $3451.3, the Jun 16 high. The bear trigger is $3248.7, the Jun 30 low. First support to watch is 3282.8, the Jul 9 low.

- WTI Crude down $0.27 or -0.4% at $67.07

- Natural Gas down $0.18 or -5.05% at $3.386

- Gold spot up $15.83 or +0.47% at $3365.75

- Copper up $4.05 or +0.72% at $564.5

- Silver up $0.29 or +0.77% at $38.4591

- Platinum up $24.94 or +1.74% at $1454.21

EQUITIES: Bull Cycle in Eurostoxx 50 Futures Remains in Play

A bull cycle in Eurostoxx 50 futures remains in play and recent weakness appears corrective. Support to watch is 5281.00, the low on Jul 1 and 4. A clear break of this price point would strengthen a bearish threat. Recent gains have exposed key resistance and the bull trigger at 5486.00, the May 20 high. It has been pierced, a clear breach of it would resume the medium-term bull cycle that began Apr 7 and open the 5500.00 handle. S&P E-Minis traded high last week resulting in a fresh cycle high. The climb confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6381.50, a Fibonacci projection. Key support is at the 50-day EMA, at 6101.83. Support at the 20-day EMA is at 6246.73.

- In China the SHANGHAI closed higher by 25.308 pts or +0.72% at 3559.791 and the HANG SENG ended 168.48 pts higher or +0.68% at 24994.14.

- Across Europe, Germany's DAX trades lower by 4.52 pts or -0.02% at 24285.7, FTSE 100 higher by 1.85 pts or +0.02% at 8994.09, CAC 40 down 17.67 pts or -0.23% at 7805.81 and Euro Stoxx 50 down 18.81 pts or -0.35% at 5340.59.

- Dow Jones mini up 112 pts or +0.25% at 44652, S&P 500 mini up 15.5 pts or +0.24% at 6350.25, NASDAQ mini up 59.25 pts or +0.26% at 23283.25.

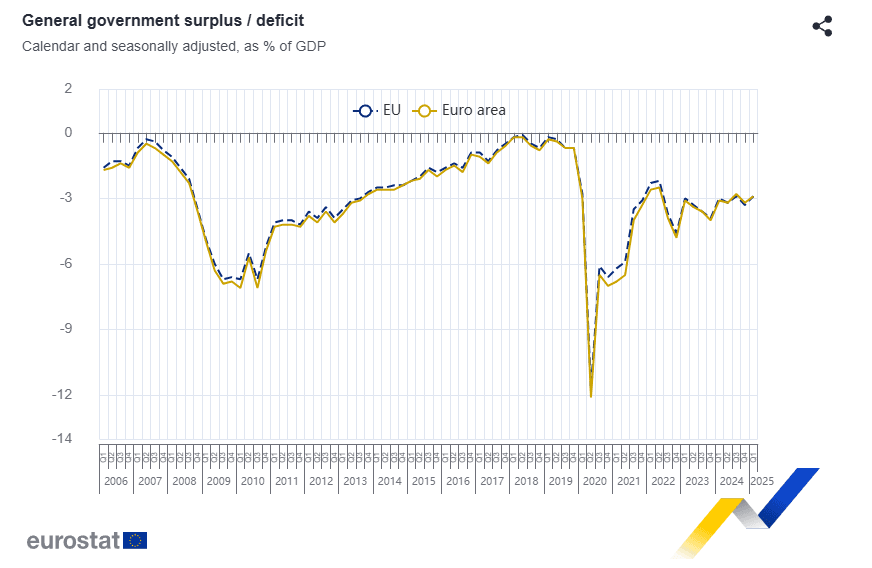

EUROPEAN FISCAL: EZ Debt/GDP Inches Up In Q1; Germany The Key Fiscal Theme Ahead

The Eurozone debt to GDP ratio inched up to 88.0% in Q1, up from 87.4% in Q4 2024 and 87.8% in Q1 2024. Compared with a year ago, the debt/GDP ratio has fallen most in Greece (-9.3pp to 152.5%), Cyprus and Ireland (-6.1pp to 34.9% - though, a reminder that Irish national accounts are best viewed through the lens of modified GDP, which strips out globalisation effects). The largest increases in debt/GDP were seen in Finland (+5.1pp to 83.7%), Austria (+4.1pp to 84.9%) and France (+3.6pp to 114.1%).

- The seasonally adjusted deficit to GDP ratio was 2.9% in Q1, down from 3.2% in Q4 2024 but up from 2.8% in Q3.

- A ramp-up in German (especially defence) spending is the key European fiscal theme in the coming years. Analysts were on balance surprised to the upside by the 2025-2029 fiscal plan announcement in terms of money spent, but some continue to point to some downside risks to the announced investment figures, and see the need for structural reforms in Germany.

- The seasonally adjusted German deficit inched down to 2.3% GDP in Q1 (vs 2.4% prior), but will likely start rising from the second half of this year onwards as the spending uptick kicks in.

- Although some high debt countries (e.g. France and Italy) are attempting to consolidate primary balances to reduce debt burdens, increased interest expenses (due to Covid-induced spending and higher interest rates) continue to push total debt/GDP in the opposite direction.