EM LATAM CREDIT: Kallpa Generacion: New Issue Guidance

Sep-04 16:19

(KALLPA; Baa3/NR/BBB-)

“GUIDANCE: Kallpa Generacion SA $Benchmark 10Y +145a (+/-5)” – Bbg

IPTs 10Y: T+170bp Area

FV 10Y: T+135bp Area

• Please see our earlier fair value post for more information:

https://mni.marketnews.com/482m9Y1

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: Large March'26 SOFR Midcurve Call Package Buy

Aug-05 16:18

- +20,000 0QH6 97.25/97.50 call spd w/

- +20,000 0QH6 97.25/97.50/97.62 AND

- +20,000 97.25/97.50/97.75 call flys, paying 13.5-13.75 total on package

FOREX: USD Index May be Building a Base

Aug-05 16:15

- The USD Index remained rangebound Tuesday, however the inability of markets to press the USD lower still after Friday's NFP print may suggest the price is building a base. ISM services data came in mixed, with headline activity softer-than-expected against a higher-than-expected prices paid subcomponent, and proved USD negative upon release, but the pullback was mild.

- The JPY was the poorest performing currency against all others in G10, aiding EUR/JPY to recovery back toward Y171. This keeps markets clear of the uptrending 50-dma support at 169.04, ahead of which the outlook remains bullish, and targets 171.85 - the 50% retracement for the fade off the cycle high at 173.97.

- Meanwhile, Trump spoke on his possible Fed picks to replace Kugler following her resignation over the weekend. The President declared he had a shortlist of 4, which includes both Kevin Warsh and Kevin Hassett, and while the President said he may use this Fed pick as a precursor to selecting the next Fed chair, he remained vague about the timing of such an announcement.

- GBP fared better, rising against most others in G10 as markets look ahead to Thursday's BoE rate decision. The MPC are expected to cut rates by 25bps, and anything other than this would mark a sizeable surprise against expectations. It's the vote split among the MPC that should prove more consequential - and should provide a strong signal for the Bank's easing plans through the second half of this year. Despite today's modest recovery, a bearish theme in GBPUSD remains intact for now - despite Friday’s rally. Last week’s sell-off resulted in a breach of the bear trigger at 1.3365, the Jul 16 low. The break confirms a resumption of the downleg that started Jul 1 and highlights a clear breach of the trendline drawn from the Jan 13 low.

- German factory orders, Italian industrial production and the Canadian services PMI data are the data highlights Wednesday. Fed's Cook, Collins and Daly are also set to make appearances.

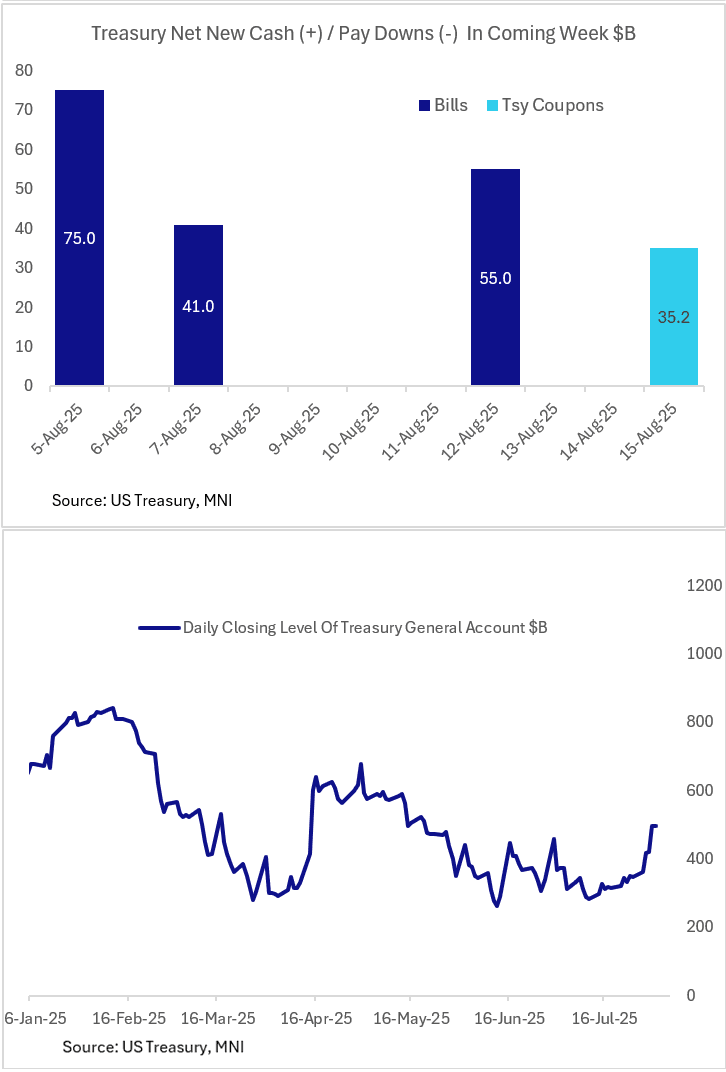

US TSYS/SUPPLY: Bill Supply Ramp-Up Continues, Reserves Could Be Pressured

Aug-05 16:06

Treasury will sell a record $100B in 4-week bills on Thursday, with a $5B increase that was not entirely unexpected in the context of the rebuild of the Treasury General Account.

- 4-month bill sizes will remain $65B (auctioned Weds Aug 6) while 8-week bills remain at $85B (auctioned Thu Aug 7 alongside 4-week). All settle on Aug 12 for a total $55B net cash raised.

- Treasury noted last month it would ramp up bill supply, and "specifically, the 4-, 6-, and 8-week bills", which it has done. Since the first week of July, when the debt limit was lifted by $5B, sizes of 4-week auctions are up from $55B, 6-week auctions have gone from $50B to $85B, while 8-week are up from $45B.

- Bill upsizing is likely coming to an end shortly - Jul 30's Treasury refunding policy statement noted "Treasury anticipates further marginal increases in short-dated Treasury bill auction sizes in the coming days and then maintaining sizes at or near those levels through the end of September."

- Including today's settlements through to mid-month, Treasury is set to raise a net $206B in new cash. Between mid-July and mid-August Treasury will have raised over $810B in new cash between bills and coupons; the last net cash paydown was in the first half of July (corresponding to the raising of the debt limit in early July).

- At just shy of $500B, the TGA is targeted to rise to $850B by end-September.

- We continue to note that reserves could pull back meaningfully by mid-September's tax date on the cash rebuild. The latest quarterly refunding saw the Treasury's advisory committee note: "Some members highlighted the potential that a rapid increase in bill issuance in conjunction with lower levels for RRP and uncertainty around levels of ample reserves could create funding stress as we head into the Treasury’s 2025 fiscal year end."