NORWAY: June Inflation at 0700BST/0800CET, Swedish Print Adds Upside Risks

Norwegian June inflation is due at 0700BST/0800CET. This will be the first inflation report since Norges Bank’s surprise 25bp cut on June 19. In an interview with the MNI Policy Team following the decision, Governor Wolden Bache indicated that Norges Bank opted to cut rates because it had gained confidence that the Q1 uptick in inflationary pressures was temporary. In this light, we think the base case should be that further cuts can be delivered in September and possibly December if CPI-ATE tracks in line with Norges Bank’s projections – provided economic activity momentum doesn’t accelerate unexpectedly. We continue to think that the bar to rate moves at interim decisions (August and November) is high, but NOK FX and rate markets will as usual be sensitive to large deviations from consensus.

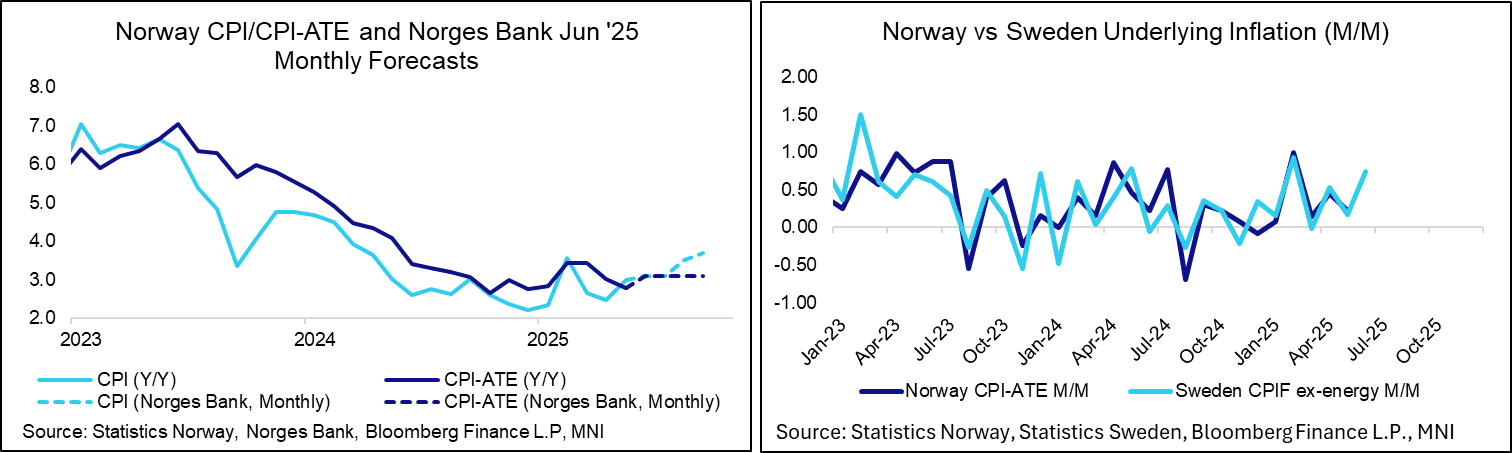

- In the June MPR, Norges Bank projected CPI-ATE inflation at 3.1% Y/Y in June through September (May: 2.77% Y/Y). For today's print, the median analyst pencils in a 3.0% Y/Y reading.

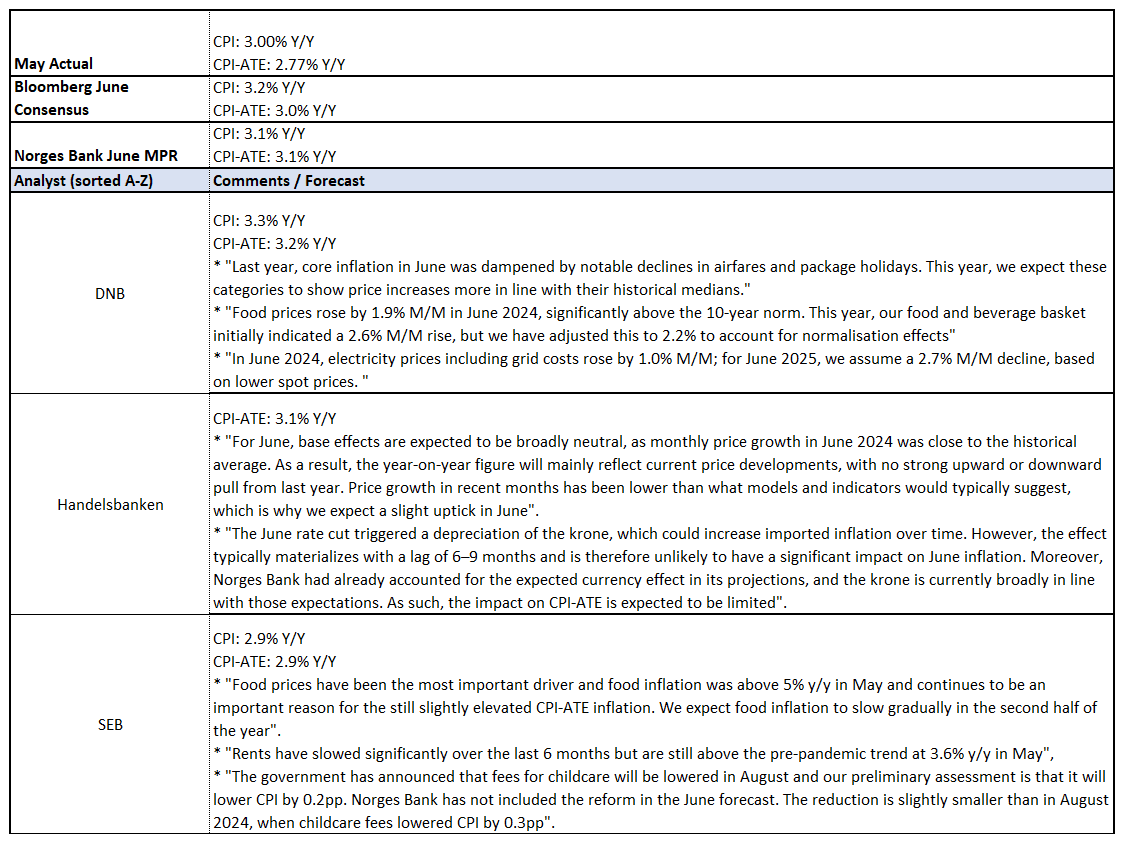

- There could be upside risks to analyst and Norges Bank projections after Monday’s Swedish flash June inflation report (3.3% Y/Y vs 2.9% cons, 2.5% prior). Since 2015, there has been a 0.56 correlation between M/M NSA Norwegian CPI-ATE inflation and Swedish CPIF ex-energy inflation. Since 2023, this correlation has risen to 0.69. The chart below also indicates a close relationship between the two inflation rates since February. Clearly, this is a crude and non-causal observation, but still worth keeping in mind.

- Swedish CPIF ex-energy was 0.74% M/M in June. If realised in Norway, this would imply an annual rate of 3.3% Y/Y – comfortably above expectations.

- Norges Bank projects headline CPI inflation at 3.1% Y/Y (vs 3.00% prior), while analysts see 3.2% Y/Y.

- See below for a selection of analyst comments:

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROZONE ISSUANCE: EGB Supply

The ESM is likely to hold a syndication while the Netherlands, Germany and Finland are all due to hold auctions today. Later this week, Germany will return for another auction while Portugal and Italy both also look to hold auctions. We pencil in estimated gross issuance for the week of E20.7bln (down from E47.3bln last week).

- The ESM has sent an RfP for an upcoming transaction. We expect a syndication today with a size of between E1-3bln. We don’t have a strong conviction surrounding the maturity that will be on offer.

- The Netherlands will kick auctions for the week off this morning with E2.0-2.5bln of the on-the-run 10-year 2.50% Jul-35 DSL ISIN (NL0015002F72) on offer.

- Germany will also come to the market this morning, looking to sell E4bln of the 2.40% Apr-30 Bobl ISIN (DE000BU25042).

- Finland will round off auctions today with up to a combined E1.5bln of the 1.50% Sep-32 RFGB (ISIN: FI4000523238) and the 0.50% Apr-43 RFGB (ISIN: FI4000517677).

CHINA STOCKS: Chinese Rare Earth Names Rally Despite Wider Equity Sell Off

We have received some questions surrounding the outperformance of Chinese equities linked to rare earths and minerals e.g. newswire headlines pointing to China Rare Earth equities rallying by 26% in Hong Kong, despite the recent sell off in the HK & Chinese equity benchmarks.

- This comes after that name added ~60% on Monday.

- We haven’t seen any fresh headline triggers for Chinese rare earths.

- The space is one of the focal areas of the ongoing Sino-U.S. trade talks, so our best guess is the move reflects speculation surrounding easier/increased exports for the sector in light of Beijing’s recent approval of some export applications for key industrial metals.

- A reminder that China’s MOFCOM noted that the country "approved a certain number of compliant applications" of rare earth-related exports over the weekend. MOFCOM went on to note that China is "willing to further enhance communication and dialogue with relevant countries on export controls to facilitate compliant trade".

EUROZONE T-BILL ISSUANCE: W/C 9 June

Spain, Belgium, France and Italy are due to sell bills this week. We expect issuance to be E21.0bln in first-round operations, down from E27.7bln last week.

- This morning, Spain will look to sell a combined E2.0-3.0bln of the 3-month Sep 5, 2025 letras and the 9-month Mar 6, 2026 letras.

- Also today, Belgium will look to issue a combined E2.2-2.6bln of TCs: An indicative E0.8bln of the 3-month Sep 11, 2025 TC and an indicative E1.6bln of the 12-month Jun 11, 2026 TC.

- This afternoon, France will look to come to the market with a combined E7.4bln of 13/14/27/49-week BTFs: E0.1-0.5bln of the 13-week Sep 10, 2025 BTF; E2.8-3.2bln of the new 14-week Sep 17, 2025 BTF; E1.4-1.8bln of the 27-week Dec 17, 2025 BTF; and E1.5-1.9bln of the 49-week May 20, 2026 BTF. The auction is held today rather than the usual Monday due to the Whit Monday public holiday.

- Finally tomorrow morning, Italy will look to sell E8.5bln of the new 12-month Jun 12, 2026 BOT.