SWEDEN: June Flash Inflation Preview - Sellside Update

Jul-04 12:18

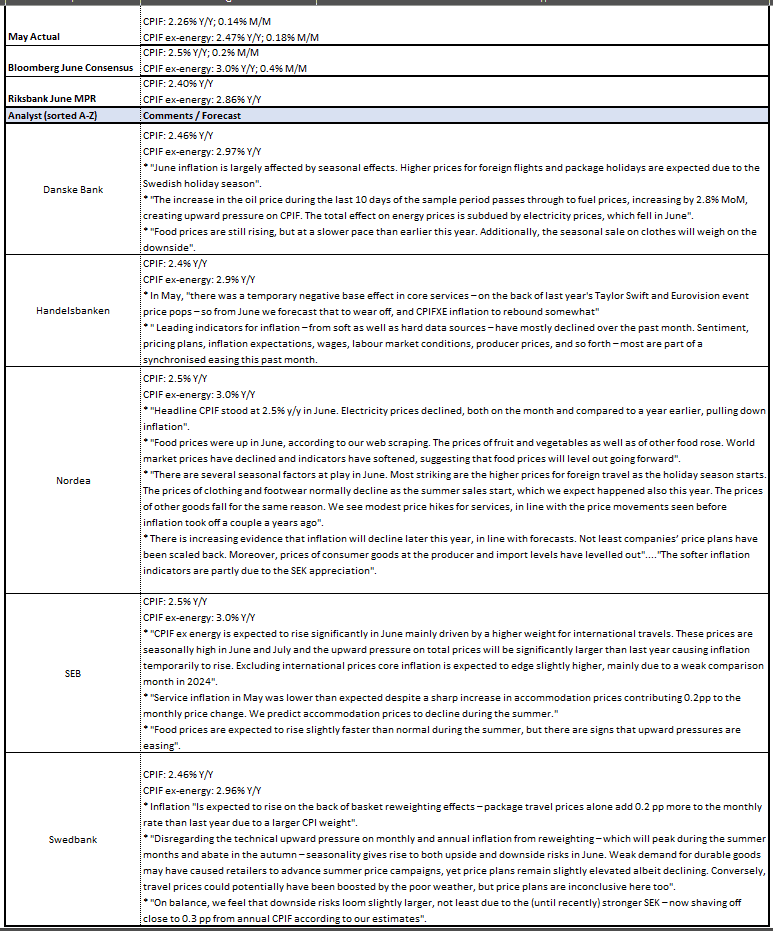

Adding Nordea to the Swedish inflation preview table - They also see CPIF ex-energy at 3.0% Y/Y.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: MNI POLITICAL RISK - GOP Leaders Downplay Schism With Musk

Jun-04 12:16

Download Full Report Here

- President Donald Trump will receive an intelligence briefing in the morning before signing ‘proclamations’ in the Oval Office. In the evening, he will attend an event on the South Lawn.

- Senate Finance Republicans will meet Trump at the White House to discuss the GOP megabill. In a series of messages on social media, Elon Musk described the bill as a “disgusting abomination.”

- Commerce Secretary Howard Lutnick and OMB Director Russell Vought are on Capitol Hill to provide Congressional testimony. Both will receive a grilling from Democrats.

- Canada and Mexico criticised Trump's proclamation raising the tariff on steel and aluminium imports from 25% to 50%, effective this morning. The proclamation includes a temporary carveout for the United Kingdom.

- EU Trade Commissioner, Maros Sefcovic, said he had a “productive" discussion with USTR Jamieson Greer.

- Markets await a call between Trump and Chinese President Xi Jinping as the trade conflict expands into a fight over supply chains.

- Social Security retirement claims are set to increase 15% this year.

- Senate Majority Leader John Thune (R-SD) appears to have learnt from the recent megabill showdown in the House by looping Trump into discussions well before a potential floor vote.

- A senior Ukrainian delegation will brief US Senators today.

- The NYT is the latest to report the Trump administration’s nuclear proposal to Tehran offered a compromise on enrichment.

- Poll of the Day: Republican satisfaction is at a “near-record high”.

Full Article: US DAILY BRIEF

STIR: Dovish ECB Could Drag Euribor-implied Terminal Back Towards 1.60%

Jun-04 12:08

With tariff-related downside growth and inflation risks still the primary concern of a dovish-leaning Governing Council, there may be scope for the Euribor-implied terminal rate to move back towards 1.60% if Lagarde keeps the door open to a July cut and the 2026 inflation/GDP projections see a larger downgrade than expected. The current terminal rate, indicated by the H6 contract, has been steady around 1.70% since May 23.

- The Euribor-implied rate curve begins to steepen back toward (and above) 2.00% from H2 2026 onwards, reflecting an impulse from higher German/EU defence spending.

- There remains uncertainty as to whether (and to what extent) an increased fiscal impulse is incorporated into the ECB’s June macroeconomic projections. It seems reasonable to assume that any effect will be seen in the 2027 forecasts, with 2025/2026 dominated by tariff-related impacts.

- From a cross-market perspective, the SFI / ER Z5 spread has consolidated above the 200bp handle, currently at 205bps. That’s down from a closing high of 209bps of May 27. With risks to the Euribor-implied terminal rate seemingly skewed to the downside, there may be scope for further widening in the spread towards initial resistance of 213.5bps (Jan 14 close).

- MNI’s full ECB preview is here.

GILT PAOF RESULTS: GBP1.176bln of the 4.375% Mar-28 Gilt sold.

Jun-04 12:03

- GBP1.188bln of the gilt had been on offer.

- This leaves GBP30.742bln of the gilt in issue.