ISRAEL: JP Morgan Say Door Likely Closed for August BoI Cut

Jul-16 10:32

- Israel’s headline CPI rose 0.3% M/m in June, translating into the annual rate rising to 3.3%. Both figures were above surveyed median estimates, tilting analysts to pare back their August easing expectations for the BOI, although further easing in Q3 is still very much on the cards.

- *JP Morgan have noted the increased inflation momentum will likely close the door for a cut at the August meeting, although a very soft July CPI report could change this perception. Yet, if they are right about the unwinding of the supply shock over the next few months, a cut in September remains probable.

- The over-year-ago inflation rate will likely fall below the 3.0% tolerance bound in the August CPI report, and if the underlying momentum remains contained and the ILS gains are not unwound, it will probably be difficult for the MPC to justify further delays in policy easing.

- *Goldman Sachs: BoI Governor Amir Yaron sounded less dovish than GS had expected, emphasising that "price stability is a condition for an orderly and growing economy" and noting that despite recent geopolitical developments, "geopolitical and economic uncertainty [...] is still at a very high level".

- With Yaron emphasising data dependence, GS continue to believe that a cut at the August MPC is possible, but they think a necessary condition is a weak July inflation print (well within the BoI's tolerance band), combined with further Shekel appreciation.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Monday Data Calendar: Empire Mfg, 20Y Bond Auction Re-Open

Jun-16 10:32

- US Data/Speaker Calendar (prior, estimate)

- 16-Jun 0830 Empire Manufacturing (-9.2, -6.3)

- 16-Jun 1130 US Tsy $76B 13W & $68B 26W bill auctions

- 16-Jun 1300 US Tsy $13B 20Y Bond auction re-open (912810UL0)

- Source: Bloomberg Finance L.P. / MNI

OUTLOOK: Price Signal Summary - USDJPY Bear Threat Remains Present

Jun-16 10:31

- In FX, a bullish EURUSD theme remains intact and the pair continues to trade closer to its recent highs. Last Thursday’s rally resulted in a breach of key resistance at 1.1573, the Apr 21 high. This strengthens the bullish theme and confirms a resumption of this year's uptrend. Sights are on 1.1696 next, a 1.618 projection of the Feb 28 - Mar 18 - 27 price swing. Initial firm support is at 1.1404, the 20-day EMA. The 50-day EMA lies at 1.1267. Short-term weakness is considered corrective.

- The trend condition in GBPUSD remains bullish and price is trading closer to its recent highs. A rising price sequence of higher highs and higher lows, together with a bull set-up in moving average studies, highlights a dominant uptrend. Sights are on 1.3681 next, the 1.500 projection of the Feb 28 - Apr 3 - 7 price swing. Support to watch lies at 1.3456, the Jun 10 low.

- USDJPY is trading in a range and remains below last week’s high. Recent weakness suggests the correction between Jun 3 - 11, is over. The trend remains bearish - moving average studies are in a clear bear-mode position, highlighting a dominant downtrend. A resumption of weakness would open 142.12, the May 27 low. Key short-term resistance is 146.28, the May 29 high. First resistance is 145.46, Jun 11 high.

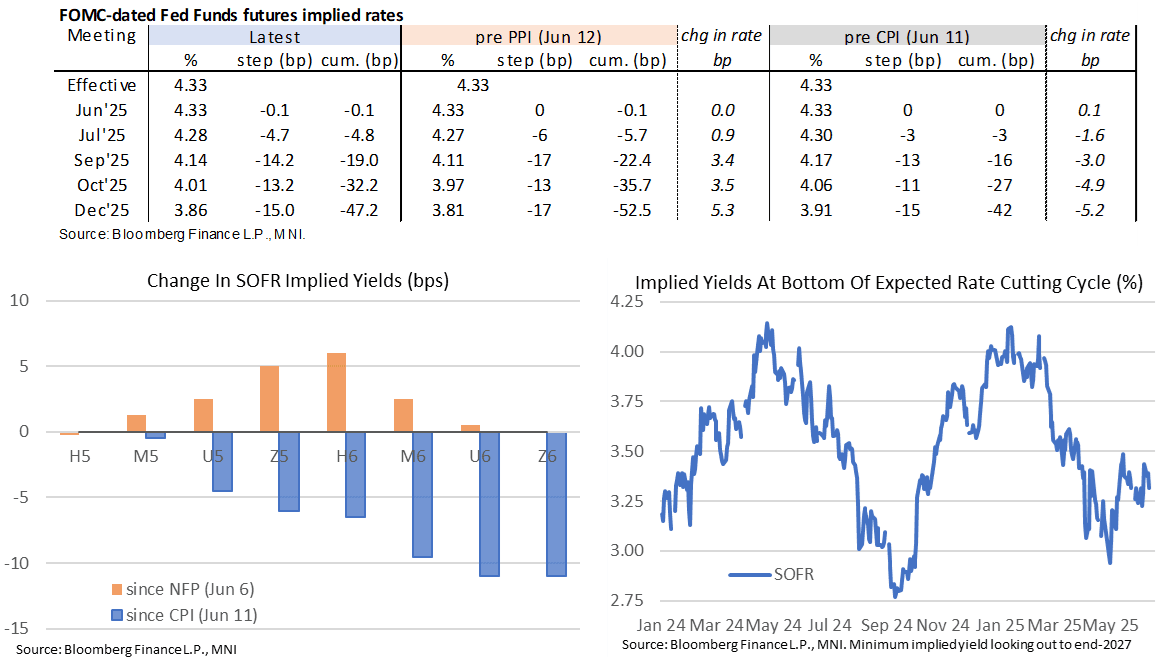

STIR: Next Fed Cut Seen In Oct With G7 and Wed FOMC Eyed

Jun-16 10:30

- Fed Funds implied rates are up to 3bp higher for 2025 meetings since Friday’s close despite modest losses for oil futures.

- The 47bp of cuts to end 2025 is off the 42bp seen before last week’s soft CPI report but remains one of the more hawkish levels in recent months.

- Cumulative cuts from 4.33% effective: 0bp for Wed, 5bp for Jul, 19bp for Sep, 32bp for Oct and 47bp for Dec.

- The SOFR implied terminal yield of 3.32% (SFRZ6, unch) points to ~100bp of cuts for what’s left of the easing cycle.

- Markets are focused on tariff and middle east discussions at G7 meetings this week before the FOMC decision on Wednesday.

- MNI Fed Preview: https://media.marketnews.com/Fed_Prev_Jun2025_ba372b9458.pdf

- The full analyst preview note will follow later today.